Demographic changes are driving investment opportunities in emerging markets

Demographic change, especially across Asia and Africa, is well known as a powerful driver of long-term economic shifts in emerging markets. As these trends work through, they change the structure of the economies concerned and create new opportunities for investors. Central among these is the consumer economy, which is growing throughout emerging markets due to growing working-age populations, rising incomes, and an increasingly urbanised population.

India, for example, is on track to become the fastest-growing major global economy, with the UN forecasting 6.6% growth in 2026 compared to 2.7% worldwide. It has benefited from a young, large population and a consumption revival. These structural changes are providing opportunities for India that should continue to bear fruit in the long term.

Emerging markets’ growing middle class

A useful prism from which to consider income levels is the level 1-4 framework developed by Swedish academic Hans Rosling, in which a person’s income can be categorised into four levels:

- Level one: less than $2 a day, bringing a life of extreme poverty. Only basic needs (food, water, shelter) can be covered on this income.

- Level two: between $2-8 a day. Nearly half the global population lives on this level of income.

- Level three: between $8-32 a day.

- Level four: $32 a day and above, the level of income enjoyed by the richest billion people.

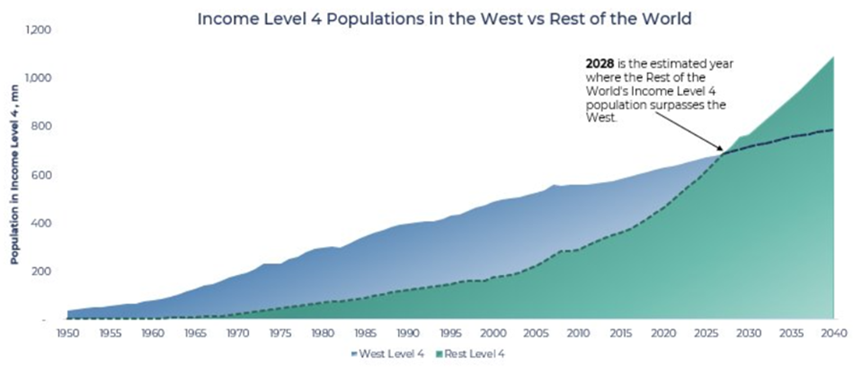

The number of people earning a ‘level four’ income outside the West is rising rapidly. In 1970, the West accounted for 89% of the level four population. By 2024, it was home to only 51.4%. It is projected that by 2028, more people in this category will be outside the West than within it, with an expected growth in the number of level four incomes in the rest of the world from 700 million in 2028 to 1.1 billion by 2040 and around 2 billion by 2050.

Population at Level 4 Income – In the West vs the Rest of the World

Source: Gapminder, United Nations, Department of Economic and Social Affairs, Population Division (2024), Guinness calculations 2025

Multinational consumer goods companies, recognising this growing opportunity, have begun to invest to gain market share in the healthcare and personal care sectors of these regions. These sectors typically become affordable relatively quickly, specifically once level two incomes are reached.

In higher income brackets such as level three and four, the rise in disposable income allows increased purchases of electronics, household appliances, leisure equipment, sportswear, and other fashion or luxury items. This opens up markets for further foreign direct investment (FDI) by multinationals from a range of different sectors as they compete to capture this new consumer demand.

Onshore production benefits from the increased disposable income

Asia

Asia, having gained the ‘keys to the factory’ as manufacturing relocated to its shores over the past generation, will directly benefit from the growth in demand within these categories in the coming generation. As leading suppliers to the consumer market outside of the developed world, Chinese companies such as Haier and Anta Sports will continue to benefit from these demographic changes, in part by catering to multiple income levels.

Haier is well placed to tackle rising demand in emerging markets for domestic appliances, with production bases in multiple countries and a portfolio of international brands. Anta has moved into the luxury sportwear market through brand acquisitions, allowing its business to grow on both domestic and international fronts.

Brazil

In Brazil, the growing middle class has permitted the ownership of cars and homes, and increased access to healthcare. One beneficiary we have identified from this is Porto Seguro, the Brazilian insurance firm, which has enjoyed stable growth from this macro-environment by providing home, automobile and health insurance. Similarly, Hypera Pharma, a leading Brazilian pharmaceutical company, has strong market positions in various categories and is likely to benefit from these structural shifts.

Powered by this combination of rising population and rising incomes, the world is reaching an inflexion point. Investors seeking to understand who the beneficiaries of this growth in consumption will need to shift their attention from the West and towards ‘the rest’.

While demographic shifts, the deepening of intra-EM trade relations, and the growth of Chinese self-sufficiency and innovation are compelling long-term structural tailwinds, investors also have to consider the timing of their entry. Find out emerging markets present an opportunity today in the next article in our ‘Why Invest in Emerging Markets’ series here.

Risk: The Guinness Emerging Markets Equity Income Fund is an equity fund. Investors should be willing and able to assume the risks of equity investing. The value of an investment and the income from it can fall as well as rise as a result of market and currency movement; you may not get back the amount originally invested. The Funds are actively managed with the MSCI Emerging Markets Index used as a comparator benchmark only.

Disclaimer: This insight may provide information about Fund portfolios, including recent activity and performance and may contains facts relating to equity markets and our own interpretation. Any investment decision should take account of the subjectivity of the comments contained in this insight. This insight is provided for information only and all the information contained in it is believed to be reliable but may be inaccurate or incomplete; any opinions stated are honestly held at the time of writing but are not guaranteed. The contents of this insight should not therefore be relied upon. It should not be taken as a recommendation to make an investment in the Funds or to buy or sell individual securities, nor does it constitute an offer for sale.