Why do emerging markets represent a compelling opportunity now?

Despite an increasingly uncertain policy environment, the US economic backdrop was supportive of equity returns in 2025. American trade policy and the Federal Reserve's interest rate cuts contributed to dollar weakness, prompting investors to reassess their US equity exposure and to reappraise international opportunities.

The logic to reassess opportunities is further supported by emerging markets enjoying the tailwinds of easing inflation, stronger balance sheets, and favourable central bank policies. Debt burdens have also been eased amid this dollar weakness, contributing to a more favourable macroprudential outlook and driving positive investor sentiment.

Combined with very attractive starting valuations, emerging markets were one of the prime beneficiaries of this shift in asset allocation last year, with money flowing back into emerging markets, especially into large-cap EM benchmark stocks.

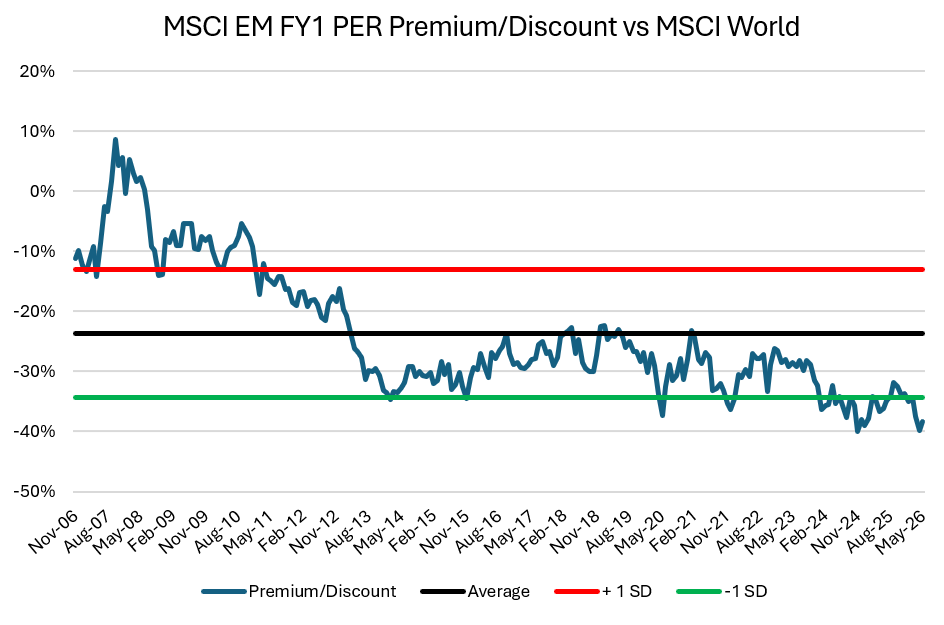

We expect the relatively benign developed-market backdrop to continue in 2026, while EM economies remain resilient. If we continue to see this interest in EM allocations (which remain at low levels), our expectation is that the rally should ultimately broaden across the market-cap spectrum. While we recognise the strong recent momentum, EM stocks remain undervalued, trading at a steep discount to developed markets, offering an attractive entry point.

Why is this the time to invest in China?

Much of the argument for emerging markets centres on China, the largest and most influential EM economy. As we discussed in our analysis of its long-term future, China has been building its economic and political capacities for decades. The country offers global markets an alternative set of trade opportunities to the US, itself a pivotal opportunity for other emerging markets.

Concurrently, China has been incentivised to move up the value chain, raising labour productivity to alleviate the constraints of an ageing population and reduce reliance on other countries. The fruits of these endeavours are evident across different avenues, all pointing to a strong investment case for the region as a whole.

Semiconductor independence

Amid US sanctions on semiconductor technology, China is rumoured to have built its first extreme ultraviolet lithography (EUV) machine, a breakthrough in its semiconductor independence. This presents a real possibility that cutting-edge chips will soon begin production in China, limiting the US’s strategic semiconductor chokepoint and strengthening Chinese supply chains in high tech (including security capabilities).

The sector is set to benefit from further government funding, with Beijing having launched Big Fund III, the largest state-backed semiconductor funding programme ever, surpassing the $39 billion in subsidies set aside under the US Chips Act (2022). The fund will be active from 2024 to 2039, and will invest across the whole semiconductor supply chain.

These developments exemplify how close cooperation between state and industry in China, through centralised research and development (R&D) and targeted funding, continues to produce gains in productivity and technological independence despite global uncertainties.

Dependence on Chinese exports

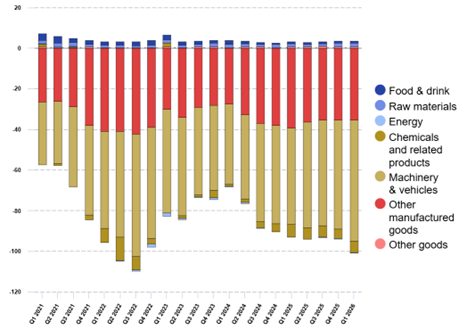

As demonstrated by the opening of international markets for Chinese high-tech products, we are already observing the increased dependence on Chinese goods by foreign markets. This can be clearly seen in the EU. The Sino-EU trade balance has, over the past 20 years, been heavily skewed towards China, with Chinese exports reaching €145 billion in Q1 2026, causing an EU trade in goods deficit of €98 billion. The vast majority of this imbalance is dominated by machinery and other manufactured goods.

EU-China trade balance by product group

Source: Eurostat, as of May 2026

China’s export of rare earths is another strength, placing it at the heart of tech production and making it one of its strongest bargaining chips in trade conflicts. Given the aforementioned difficulty in developing local rare-earth supply chains, it will be a long time before China loses this edge.

Furthermore, China continues to pursue deeper structural economic relationships globally with the Belt and Road Initiative (BRI), which should further cement these international dependencies. One of the most prescient recent examples of this is China’s focus on transforming its often-neglected western regions of Xinjiang and Tibet into key energy and trade corridors. The Yarlung Tsangpo River hydro project in Tibet alone (begun in 2025) is predicted to produce three times as much energy as the largest hydropower plant currently in operation. This is being supplemented by electricity transmission and transport infrastructure projects throughout the region, positioning Western China as a key energy exporting hub.

Is China’s economy strong or weak in 2026?

The US-centric narrative is that China is a country mired with problems. The fallout of a weakened property sector, the challenges in youth employment in the labour market, and the overcapacity that has built up in many industries are all expected to weigh on profitability and returns. However, we think there is support for the more China-centric view. The mostly stable policy environment has yielded vast improvements in China’s productive capabilities, and the full impact is starting to become apparent.

The real estate sector has levelled out

Real estate has undoubtedly been a drag on the economy, having been in a slump for several years, with the old real estate model of ‘high debt, high leverage, high turnover’ causing many property developers to default. However, Chinese policy support to the tune of 300 billion yuan ($42.3 billion) has helped to stabilise the ailing property sector. Furthermore, we have now reached a stage where the contribution from China’s new pillar industries outweighs the drag from real estate. With valuations still very low, we don’t think this has necessarily been fully reflected in the market.

Sector overcapacity is being managed

Key industries in China have been engaged in hyper-competitive, circular battles for market share, leading to price wars, oversupply and thinning margins, a phenomenon called ‘involution’. This issue has been acknowledged by China through its ‘anti-involution drive, in which China has attempted to curb self-defeating price wars and export local oversupply to global markets, where low price points have made Chinese goods, such as EVs, highly competitive. China’s growing export capabilities, driven by projects such as the BRI, are key to directing excess capacity internationally.

As an emerging leader in technological innovation, underpinned by its unique combination of state-funded R&D, mass production capacity, and integrated supply chains, we believe that China is increasingly aligned to meet the demands of the rapidly evolving global economy in next-generation industries.

Read here to understand how we at Guinness invest in China and the wider EM region to benefit from its raw potential while mitigating the risks associated with the region.

Risk: The Guinness Emerging Markets Equity Income Fund is an equity fund. Investors should be willing and able to assume the risks of equity investing. The value of an investment and the income from it can fall as well as rise as a result of market and currency movement; you may not get back the amount originally invested. The Funds are actively managed with the MSCI Emerging Markets Index used as a comparator benchmark only.

Disclaimer: This insight may provide information about Fund portfolios, including recent activity and performance and may contains facts relating to equity markets and our own interpretation. Any investment decision should take account of the subjectivity of the comments contained in this insight. This insight is provided for information only and all the information contained in it is believed to be reliable but may be inaccurate or incomplete; any opinions stated are honestly held at the time of writing but are not guaranteed. The contents of this insight should not therefore be relied upon. It should not be taken as a recommendation to make an investment in the Funds or to buy or sell individual securities, nor does it constitute an offer for sale.