Iran conflict and three scenarios of the impact on the energy sector

This insight looks at the recent escalation of military conflict between the United States, Israel, and Iran, and its potential impact on global energy markets. With Iran a meaningful oil producer and the Strait of Hormuz a critical transit point for roughly one-fifth of global crude and liquefied natural gas (LNG), the duration and scale of any disruption could have material impacts on global energy markets. We outline three scenarios with differing levels of escalation and the potential implications for oil and gas prices and energy equities.

The three scenarios considered, with escalating impact to the energy sector, are as follows:

Scenario one: the conflict is short-lived, with limited disruption to physical oil supplies and parties return to a negotiated outcome.

Scenario two: the conflict is protracted, with physical shipments of oil and natural gas impacted but not stopped entirely, despite Iranian efforts.

Scenario three: the conflict is protracted and becomes a wider war as other countries get involved. Iran is successful in shutting off a higher proportion of oil & gas supply through the Strait of Hormuz for a prolonged period.

As a reminder, Iran currently produces around 3.5 million barrels per day (3.5% of world oil supply) of which around 1.7m b/day is exported, predominantly to China. Iran holds the world’s fourth-largest oil reserves and second-largest gas reserves. There have been several years of Iranian export volatility, driven by western sanctions against the country’s nuclear programme.

What is the current situation?

Before reviewing the scenarios, the following is a summary of events at the time of writing:

The United States and Israel have commenced military strikes on Iran with the stated aim of regime change in Iran.

Ayatollah Ali Khamenei, Iran’s supreme leader, has been killed along with several key military and political leaders.

Iran has announced its intention to shut the Strait of Hormuz and a number of oil tankers have been attacked. Tanker flow has slowed sharply, with around two hundred tankers dropping anchor close to the Strait.

A number of oil majors and trading houses have suspended tanker sailings through the Strait of Hormuz for several days.

OPEC has announced 0.2m b/day of quota increase for April 2026 loadings.

Scenario one

The conflict is short-lived, with limited disruption to physical oil supplies and parties return to a negotiated outcome.

This is the least disruptive scenario which sees the conflict conclude quickly.

For oil supply in this scenario, there is limited disruption through the Strait of Hormuz, a 21-mile-wide stretch of water separating Iran from the UAE and Oman.

The strait is a vital corridor that represents a critical chokepoint in global energy logistics as it facilitates the transit of approximately 20m b/day of crude oil, condensate, and oil products—equivalent to around 20% of global oil supply and 30% of seaborne oil trade. It also facilitates the transit of 20% of global liquefied natural gas (LNG) production.

Red Sea & Strait of Hormuz shipping routes showing prior Houthi attacks

Source : Al Jazeera

With conflict over, the global oil market likely returns to the prior forecasted oversupply in 1Q 2026. Spot oil prices likely recede to the mid $60s and the forward curve remains flat, reflecting a very modest risk premium for the unsteady equilibrium in the region and the market balance.

Similarly, the supply of LNG is not materially impacted and European and Asian gas pricing starts to reflect fundamental supply and demand factors. Energy equities act rationally and fall on the conclusion of the war but maintain a risk premium.

Scenario two

The conflict is protracted, with physical shipments of oil and natural gas impacted but not stopped entirely, despite Iranian efforts.

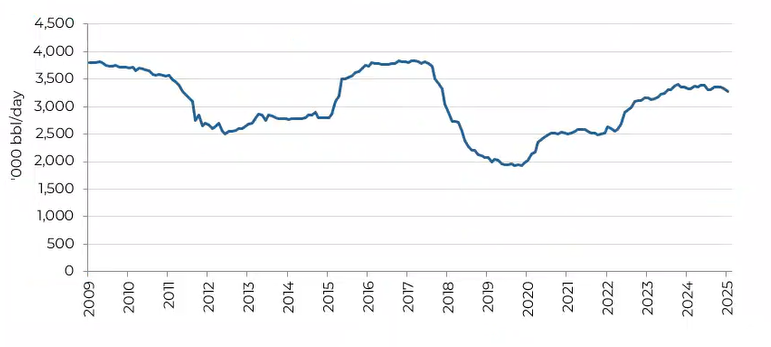

Trump’s comments on Sunday 1st March suggest that the main phase of the conflict could last for around four weeks. Beyond that, the lack of an obvious ‘end game’ increases the risk of a power vacuum and raises the spectre of lower Iranian oil production and oil exports (currently at around 3.5m b/day and 1.7m b/day respectively) as political chaos could impact production facilities (as seen historically in Iraq and Libya).

Iranian oil production (000s b/day)

Source: Bloomberg, 28th February 2026

Potential effect on global oil

In this scenario, Iranian efforts to shut the Strait of Hormuz are partially successful in that some tanker traffic chooses to not pass through the Strait owing to the risk of attack.

To circumvent the Strait, Saudi likely re-routes some of its oil exports through to the Red Sea and the UAE re-routes some volumes via onshore pipelines to the Gulf of Oman (there is thought to be around 3-4m b/day of total spare pipeline capacity here).

Nevertheless, the global oil and LNG markets suffer supply constraint. Houthi rebels and other Iranian militias disrupt shipping in the Red Sea around the Bab al-Mandeb Strait causing the re-routing of large volumes of seaborne oil and LNG around the Cape of Good Hope at the southern tip of Africa. Consuming countries rely on ample strategic storage for their short-term oil supplies, which will be politically acceptable in the near term but not a solution if the disruption persists.

Oil prices in this scenario likely rise to a $80-100/bl range, also pulling the forward curve for oil higher. Beyond inventory consumption, there are limited short-term supply responses available to make up such a shortfall. Whilst OPEC could increase quotas and promise to satisfy the market, most of its spare capacity would likely also be caught up in the Strait of Hormuz disruption.

Potential effect on natural gas

In terms of natural gas, around 75-80 million tonnes per annum of LNG (around 20% of global LNG supply, predominantly from Qatar) transits the Strait of Hormuz, with Asia as its primary destination. A supply disruption here could be arguably more impactful than for crude oil since there is no other option for these LNG volumes to bypass the Strait (leaving them effectively locked out of the market) and because natural gas inventories in Europe (the marginal consumer of global LNG) are currently at particularly low levels.

In Europe, despite winter coming to an end, there is a significant need to start the summer inventory refill process. Europe would need to compete for global LNG volumes (as it did in the aftermath of the Russian invasion of Ukraine) meaning that prices could be biassed sharply higher, potentially exceeding $20/mcf (thousand cubic feet). Asian consumers, especially China, would likely curtail LNG demand at these prices and switch demand towards cheaper domestically produced coal for power generation.

Energy equities in a protracted conflict

Taking the bottom end of our $80-100/bl price range for this scenario: if energy equities reflected $80/bl as a long-term Brent oil price, we see around 30% equity price appreciation, relative to pre-conflict valuations.

Scenario three

The conflict is protracted and becomes a wider war as other countries get involved. Iran is successful in shutting off a higher proportion of oil & gas supply through the Strait of Hormuz for a prolonged period.

In this scenario, Iran and its allies thwart US and Israeli efforts to force regime change and a broader conflict ensues, both militarily and economically. Equity risk premia likely increase and equity markets suffer as more countries become embroiled in the conflict, which drags on.

Implications of a wider war for oil

The effect on the oil markets would be an amplified version of scenario two, with spot oil prices rising to $100/bl and above, leading ultimately to demand destruction. Forward oil prices rise in sympathy.

Global oil refining margins likely suffer as a weakening global economy limits global oil product demand.

Implications of a wider war for natural gas

European and Asian gas prices likely act in a similar manner. The most recent analogy for European gas would be the Russian invasion of Ukraine, when gas prices spiked to around $40/mcf ($240 per barrel of oil equivalent) to balance the market: i.e. stifle demand and incentivise significant other supply. The loss of all LNG volumes through the Strait would be equivalent to around two thirds of Russian pipeline gas volumes to Europe pre-invasion in 2021.

Implications of a wider war for energy equities

In this scenario, energy equities would likely be a safer haven in weaker global equity markets. For reference, if energy equities priced in $100/bl as a long-term oil price, with equity risk premia unchanged, we see it implying around 90% equity upside.

What does this mean for energy equities?

The big questions concern the duration of the conflict and the extent to which oil and gas supply disruption in the Strait of Hormuz persists. At 3.5m b/day, Iran is a material oil producer, and at 20m b/day, the Strait of Hormuz is by a distance the most important oil shipping lane in the world. Against these risks, we must weigh the fact that the global oil market was oversupplied in 2025 and that inventories are at comfortable levels.

Stepping back, the common thread in all three scenarios is that energy markets are likely to embed a more persistent geopolitical risk premium in oil and gas prices than was evident prior to the outbreak of current hostilities.

Even in scenario one, where the conflict proves short-lived, that premium fades but does not disappear as the event itself proves the vulnerability of the Strait of Hormuz as a single chokepoint in both crude and LNG transit. In scenarios two and three, that premium becomes more structural as a partial or prolonged conflict solidifies supply constraints and changes overall demand in the market.

In all three scenarios, the higher geopolitical risk premium points to higher oil & gas prices, all else equal. But while the sector has rallied, it continues to discount relatively conservative long-term commodity price assumptions.

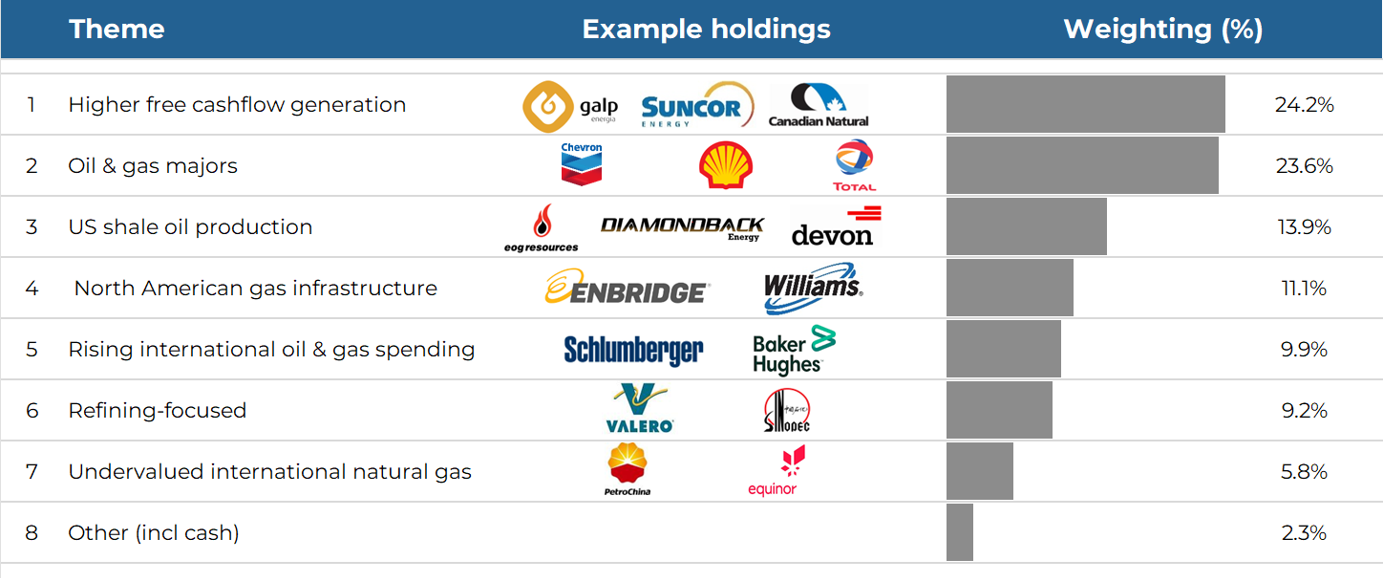

The Guinness Global Energy Fund is entirely invested in oil and gas companies and is positioned to benefit directly from strength in oil and gas markets. Today’s portfolio is diversified across energy majors, mid-cap integrateds, exploration and production, services, refiners and midstream companies in North America, Europe and Asia.

Source: Guinness Global Investors. Data as of 28.02.2026

Discover how we invest in these themes

Disclaimer: This insight may provide information about Fund portfolios, including recent activity and performance and may contains facts relating to equity markets and our own interpretation. Any investment decision should take account of the subjectivity of the comments contained in this insight. This insight is provided for information only and all the information contained in it is believed to be reliable but may be inaccurate or incomplete; any opinions stated are honestly held at the time of writing but are not guaranteed. The contents of this insight should not therefore be relied upon. It should not be taken as a recommendation to make an investment in the Funds or to buy or sell individual securities, nor does it constitute an offer for sale.

Risk: The Guinness Global Energy Fund and WS Guinness Global Energy Fund are equity funds. Investors should be willing and able to assume the risks of equity investing. The value of an investment and the income from it can fall as well as rise as a result of market and currency movement; you may not get back the amount originally invested. The Funds are actively managed with the MSCI World Energy Index used as a comparator benchmark only.

The commentary, which can be accessed via the article links above, contains important information about the Funds and further details on the risk factors are included in the Funds’ documentation, available here