China's long term future

The sustained investment made by China over the past ten years in new pillar industries is starting to bear fruit. China’s growing technological prowess is allowing it to establish leadership positions in strategically valuable sectors and become increasingly self-sufficient.

This is part of China’s wider two-pronged strategy, as discussed in our insight into Apple’s relationship with China.

- Reduce reliance on other countries.

- Increase reliance of other countries on China.

How weaponised interdependence has catalysed Chinese innovation

Much of China’s investment and subsequent innovation has been spurred by weaponised interdependence, the process by which nation-states can exert leverage within supply chains to coerce others.

In 2025, the most prominent example of this is the semiconductor industry, which stands at the centre of a huge share of today’s technological advancement and the products that are driving GDP growth. Advanced semiconductors are produced amid a highly globalised and yet highly specialised series of supply-chain chokepoints. From Dutch extreme ultraviolet (EUV) lithography machines (made by ASML) to Taiwanese fabs, each link is critical and many are entrenched.

China’s production is principally in lagging-edge chips, a consequence of US sanctions that restrict China’s access to key semiconductor technologies that have been in effect since 2019. While US restrictions have impacted the local industry in the short term, they have catalysed new policies from Beijing to support the chip industry.

This flurry of investment and innovation is perhaps best epitomised by the announcement of DeepSeek, a watershed moment that has drawn attention to the progress of China’s AI sector. DeepSeek has driven efficiency improvements in AI chips, helping reduce computational demands for model training and interference, thus allowing weaker chips to run AI. This has challenged the position of leading American chip designers, such as Nvidia, by essentially developing around the need for their products.

China’s rare-earth leverage

America’s ability to squeeze chokepoints is not unilateral. China holds almost half the global reserves of rare-earth minerals and accounts for around 71% of mining, 87% of processing and 91% of refining. The materials are essential for creating magnets, key to the defence, automotive, green energy, and semiconductor industries across the world. China produces around 90% of these magnets.

China’s rare-earth hegemony stems not from scarcity, but from entrenched and structured supply chains and infrastructure that could take decades for developed countries to replicate. In response to the US ‘liberation day’ tariffs, China has introduced export controls on rare-earth elements. While developed markets attempt to develop rare-earth self-sufficiency, decoupling will be a lengthy and costly process which may not ultimately succeed.

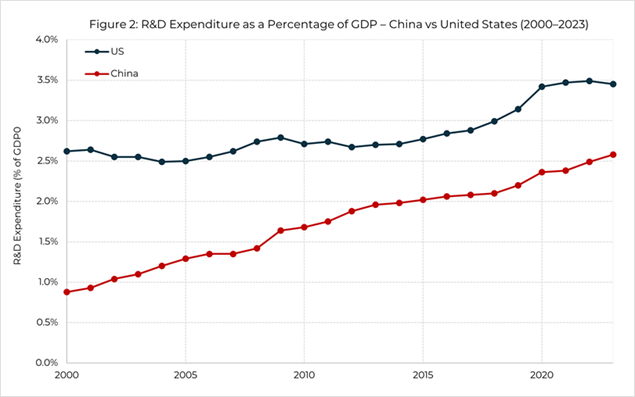

China is investing in the right sectors

China now leads the US in early-stage research across areas such as green energy (EVs, batteries, solar), 5G telecom, rare-earth mining, and quantum communication, among others. It has achieved this by leveraging links between the state, private sector, and research institutions to commercialise early-stage research and development (R&D). In fostering these industries at early stages through subsidies rather than more aggressive strategies such as tariffs, China has also mitigated internal price distortions that could have further suppressed domestic consumption.

Source: Guinness Global Investors; OECD Main Science and Technology Indicators

China’s technological rise has enabled it to provide new goods at competitive prices and secure supply chains, without jeopardising its goal of self-sufficiency. By holding these levers of production power and controlling the rare-earth supply chain, China has been able to circumvent the worst attempts by the US to stymie its progress. In doing so, China not only challenges the US but the global order itself by carving out its own diplomatic and political trajectory.

Changing export destinations

China has been laying the groundwork to capture EM consumption for many years through the Belt and Road Initiative (BRI), started in 2013. The initiative aims to leverage Chinese investment and expertise to revitalise the ancient Silk Roads that connected Europe and Asia. It does this through investments and funding in major infrastructure projects, such as railroads, ports, and pipelines.

When the BRI was first introduced, many viewed it mainly as a way for China to export excess construction capacity internationally by financing foreign infrastructure development. However, it also plays into China’s aim to foster interdependence among partnering countries with the Chinese economy. Today, Chinese exports to countries participating in the BRI have more than doubled since its inception, accounting for around 53.6% of total exports.

A flagship example of the BRI is the China-Pakistan Economic Corridor (CPEC), which was launched in 2015. The CPEC aims to connect the ports of Gwadar and Karachi to China’s interior, specifically the Xinjiang region, by road, rail and energy transport.

By continuing to cultivate closer diplomatic relationships and connected infrastructure through the BRI, as its manufacturing sector has advanced rapidly, China can continue to open new markets to receive its growing outputs, diversifying traditional export destinations away from the US.

What does this mean for investors?

China’s success in advanced manufacturing and securing export markets for its products has two key implications for investors. First, China’s move up the manufacturing value chain has created ever-increasing numbers of high-quality companies for investors to choose from – companies with real competitive advantages and the cash flows that demonstrate an ability to harness them – rather than those reliant on subsidy or weaponised interdependence. Secondly, the production of higher-value goods has brought higher wages and greater personal wealth, leading to a consumer economy served by ever more high-quality companies of its own. Assertive government policy may have created the conditions in which such companies can thrive, but their persistent and real returns on capital demonstrate that they can now stand for themselves. For investors, this creates an ever-broader opportunity set.

While China is a central pillar of trade within emerging markets, intra-EM trade is growing considerably across the region as a whole. Learn more about this deepening of intra-regional trade relations and its implications here.

Risk: The Guinness Emerging Markets Equity Income Fund is an equity fund. Investors should be willing and able to assume the risks of equity investing. The value of an investment and the income from it can fall as well as rise as a result of market and currency movement; you may not get back the amount originally invested. The Funds are actively managed with the MSCI Emerging Markets Index used as a comparator benchmark only.

Disclaimer: This insight may provide information about Fund portfolios, including recent activity and performance and may contains facts relating to equity markets and our own interpretation. Any investment decision should take account of the subjectivity of the comments contained in this insight. This insight is provided for information only and all the information contained in it is believed to be reliable but may be inaccurate or incomplete; any opinions stated are honestly held at the time of writing but are not guaranteed. The contents of this insight should not therefore be relied upon. It should not be taken as a recommendation to make an investment in the Funds or to buy or sell individual securities, nor does it constitute an offer for sale.