The long-term opportunity for wind energy

2025 wind sector in review

Global installations reached record levels

In recent years, the global wind market has overcome elevated interest rates, supply chain disruptions and regional challenges to record levels of installations. In 2025, the global wind industry is expected to have added 143 gigawatts (GW) of installations, an all-time high and a 17% increase from 2024’s previous record installations. For comparison, the United Kingdom's total installed capacity, both onshore and offshore, is around 30 GW. Global growth was led by a reacceleration of onshore wind installations, with an anticipated record 130 GW of capacity added, representing 18% annual growth from the previous year.

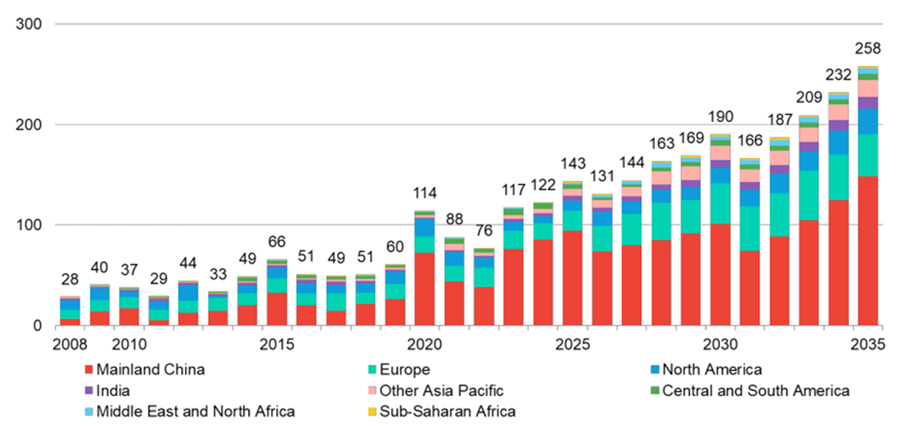

Global wind: annual installations GW

Source: BNEF, February 2025

Onshore wind

As it has been for a decade, mainland China was the largest onshore market in 2025, installing about 85 GW of capacity. India also continues to see strong growth and is likely to surpass 5 GW of new installed capacity in a single year for the first time.

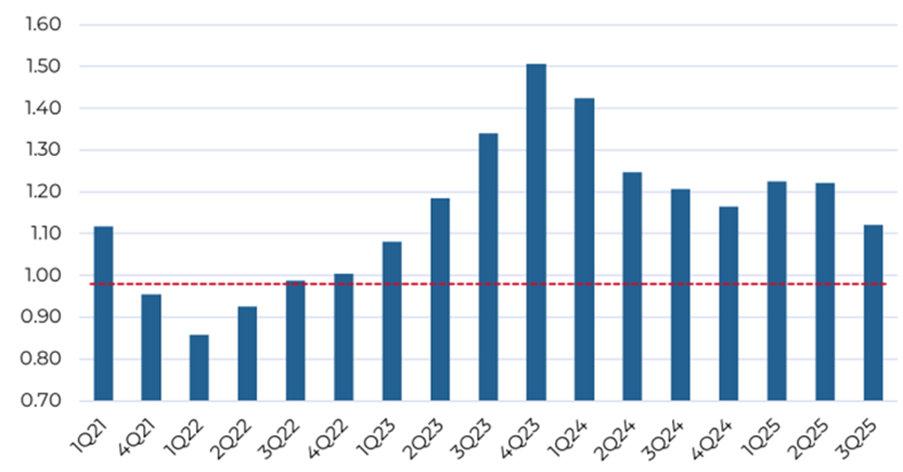

2025 was also a record year for Europe, the Middle East, and Africa, with 17 GW of capacity added, driven by a rebound in key markets such as Germany, Sweden, and France. Consistent book-to-bill ratios above 1x in Europe, which indicate a growing order backlog, suggest a strong demand outlook over the coming years.

In the Americas, onshore installations are expected to have grown 11% year-over-year in 2025, with a rebound in the US offsetting weakness in Latin America.

Encouragingly, growth looks to be increasingly demand-driven rather than subsidy-driven, with corporate power purchase agreements (PPAs), data centre expansion and electrification producing structural support across Europe, the US and parts of Asia Pacific.

Trailing 12-month Book to Bill for European Wind Turbine OEMs

Source: Guinness Global Investors, Bloomberg, February 2026

Offshore wind

Offshore wind installations continued to expand in 2025, anchored by strong activity in Europe and sustained large-scale deployment in China. The sector has faced headwinds in recent years, with higher interest rates, cost inflation and supply chain disruptions putting pressure on project returns and profitability. However, with some of these obstacles begin to ease, new offshore capacity is likely to have exceeded 13 GW in 2025.

As with onshore wind, China was the largest market for offshore wind in 2025, with additions of 9.6 GW, supported by domestic supply chains and supportive financing policies.

Elsewhere, the US offshore wind industry has come under pressure from the Trump administration, and the outlook for the sector appears more challenging in the short term.

Developments in the wind market and the outlook for 2026

2025 marked a year of record installations and increasingly diversified growth. In 2026, recent policy developments have helped to provide clarity on the outlook for wind installations, particularly in China and Europe.

China has upgraded its national wind installation targets

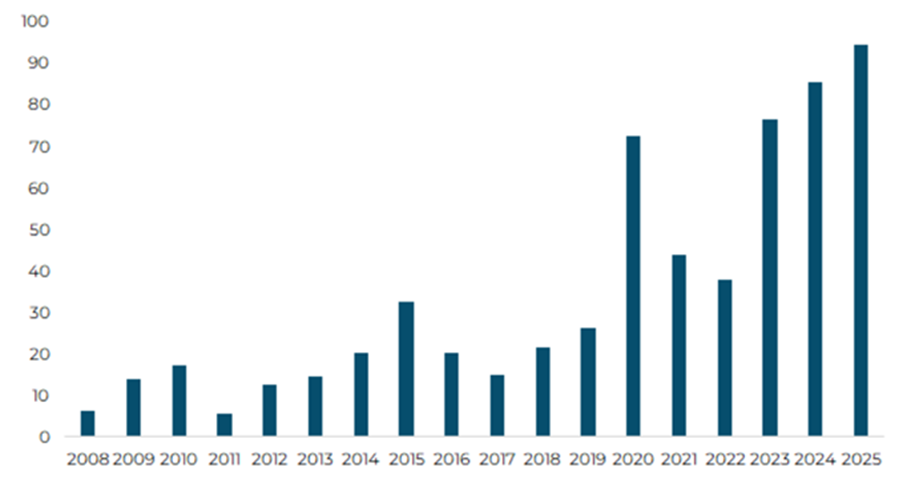

Since the signing of the first Beijing Declaration on Wind Energy in 2020, global wind industry growth has been driven primarily by the large-scale build-out of capacity in mainland China. By 2024, China accounted for around 50% of the world’s total installed wind capacity. This dominance has continued in the near term, with China expected to have contributed approximately 66% of global wind installations in 2025.

While China’s share of global installations remains substantial, the country has moved from a system of feed-in tariffs, where renewable energy producers were guaranteed a fixed price for the electricity they generated, to a more market-based system.

Under this new approach, renewable energy must compete directly with fossil fuels in the open power market. Although this will likely introduce short-term challenges and lower expectations for installations in the coming years, we are encouraged to see that Beijing has updated its capacity targets in its Declaration on Wind Energy 2.0.

The updated declaration states that China will aim to install no less than 120 GW of new capacity every year between 2026 and 2030, including 15 GW of offshore capacity. This would ensure that China’s cumulative wind power capacity reaches 2,000 GW by 2035, and puts them on track to achieve Beijing’s longer-term target of installing 5,000 GW of wind capacity by 2060.

China wind installations 2008-2025 (GW)

Source: BNEF, February 2026

The UK announced a record offshore wind auction

Although the UK is the world’s second-largest offshore wind market, it has faced challenges in recent years. Higher costs and rising interest rates led to a decline in capacity awarded in the 2023 auction round, where developers bid for the right to build new power projects with the aim to meet government capacity targets.

Against this backdrop, it was encouraging to see the UK government’s latest Contracts for Difference (CfD) auction award over 8.4 GW of offshore wind capacity, comprising 8.2 GW of bottom-fixed projects and two floating offshore wind projects totalling approximately 0.2 GW. The auction set a new record for offshore volumes and materially exceeded market expectations of 4–5 GW.

Increased financial support for near-term wind goals

The strong auction outcome in October was supported by a doubling of the annual budget for UK offshore wind CfDs from £0.9bn to £1.8bn.

The increased financial support enabled the government to raise strike prices to around £90/MWh. A strike price is the guaranteed price per megawatt-hour that a generator receives for the electricity it produces under a CfD. If the market price is below this level, the government pays the difference, while if it is above, the generator pays the difference back.

The £90/MWh level was sufficient to make projects financially viable despite recent inflationary pressures and higher interest rates, while remaining below the threshold Aurora Energy Research believes would raise UK electricity prices. The improved funding also enabled contracts to be offered for 20-year terms, compared with 15 years in earlier auction rounds.

Encouragingly, around 1.7 GW of awarded capacity is expected to come online in 2028–29, implying near-term construction activity and earlier-than-expected turbine ordering.

On the back of these results, the UK is on track to have approximately 36 GW of offshore wind capacity operational within the next four years, broadly aligning with its 2030 targets and reinforcing its position as the world’s second-largest offshore wind market.

Europe signed a multinational target to develop offshore wind

In January, a collection of ten European countries signed the Hamburg Declaration, committing to the development of 100 GW of cross-border offshore wind capacity in the North Sea by 2050. The agreement builds on the earlier Esbjerg and Ostend declarations and sits within a broader ambition to reach 300 GW of offshore wind capacity over the same period.

Cross border collaboration in Europe

The Hamburg Declaration is notable for its emphasis on cross-border collaboration, shifting away from a model where offshore wind is planned and delivered on a country-by-country basis. Under the agreement, the proposed capacity is intended to deliver power across borders, with the aim of improving security of supply and reducing overall system costs.

Once fully deployed, the projects are estimated to provide sufficient electricity to power nearly 150 million households. For European wind developers, the Declaration signals a sustained and coordinated pipeline of large-scale projects, providing visibility that should support investment into the sector.

In the US, political uncertainty is hurting the sector

Despite policy pressures, rising power demand should support US industry growth.

Since coming into office, the Trump administration has taken steps that have increased policy uncertainty for the US wind industry. While amendments to President Biden’s Inflation Reduction Act (IRA) were ultimately less restrictive than feared, the One Big Beautiful Bill Act (OBBBA) accelerated the phase-out of utility-scale wind Investment and Production Tax Credits, raising the cost of developing new projects.

Wind tax credits will remain until 2027

Subsequent clarifications, however, materially improved the outlook by extending the eligibility windows for remaining tax credits, and wind-related manufacturing tax credits were confirmed to remain in place through 2027.

Issues with US offshore wind

In offshore wind, the administration has adopted a more interventionist stance, issuing stop-work orders on five major projects despite construction already being underway. While these actions introduced near-term disruption, projects have been able to proceed following successful legal challenges, with the US still expected to add around 5.8 GW of offshore wind capacity between 2025 and 2029.

Wind power still has strong potential in the US

Despite these policy challenges, we continue to see a supportive backdrop for wind in the US for the medium to long term, underpinned by structurally rising electricity demand. Utilities and policymakers are facing sustained growth in power consumption driven by AI data centres, which we discuss in further detail here, as well as the reshoring of manufacturing, and the broader electrification of transport, buildings and industry. Meeting this demand requires new generation capacity to be deployed at speed and at scale, where wind remains well-positioned on both cost and delivery timelines.

In this context, the outlook for onshore wind remains positive. Installations are estimated to have increased by around 25% in 2025 to approximately 7 GW, with growth expected to average close to 9% per annum over the next decade as US power demand inflects structurally higher. Given its competitive economics and its ability to be deployed quickly, we continue to believe onshore wind will play a central role in the evolution of the US electricity mix.

Outlook for 2026

Looking ahead to 2026, the outlook for global wind demand will depend upon how China adjusts to its new market-based power regime. As mentioned earlier, the country has replaced fixed feed-in tariffs with liberalised market trading, potentially introducing short-term headwinds for developers.

However, with Beijing announcing new targets of no less than 120 GW of capacity additions per year, we are confident that China will continue to expand its domestic industry as its electricity demand continues to grow.

Outside of China, the global wind market is increasingly diversifying, with strong contributions from India, Europe and parts of Southeast Asia expected in 2026. The offshore market is set for a step up in 2026, with project completions due across a range of markets such as the UK, Vietnam and France.

Wind generation is becoming cheaper

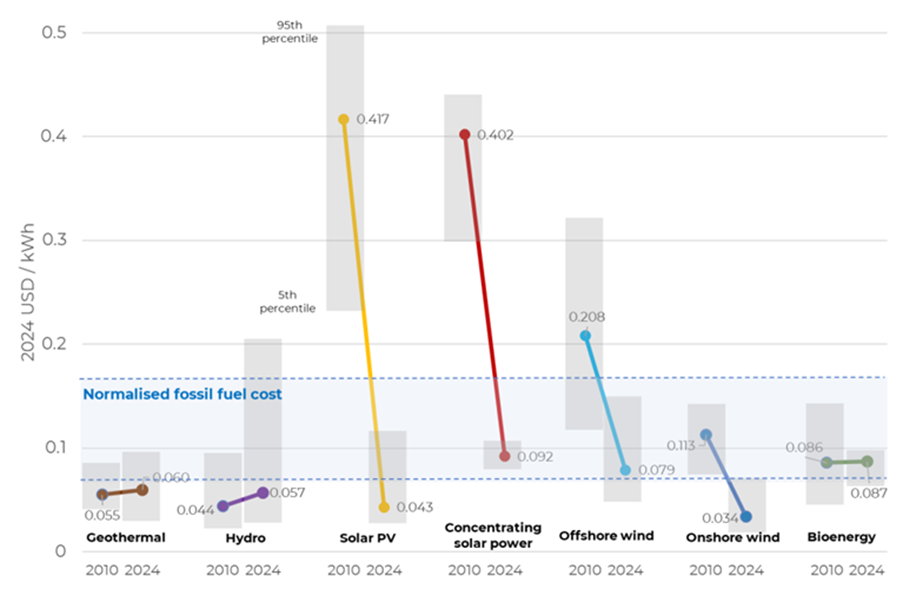

We continue to believe that wind will increase its share of the global electricity mix, underpinned by favourable economics and improvements in technology. Research from the International Renewable Energy Agency (IRENA) in 2025 demonstrates that both onshore and offshore wind generation are among the cheapest forms of new electricity in most situations.

The estimated Levelized Cost of Electricity (LCOE) ranges between $0.03-0.08/kWh. New wind generation from projects that were commissioned in 2024 is now competitive with the cheapest fossil fuel generation, which also produces power at $0.08/kWh.

Pleasingly, LCOEs for wind have remained broadly flat versus 2024 data, as the impact of higher interest rates and the 2022/23 inflation cycle were offset by greater economies of scale. Conversely, with inflation in gas turbine prices, we would expect estimates for the cheapest new fossil fuel generation to trend upwards in the coming years.

Global LCOE of newly commissioned utility-scale renewable power generation technologies (2010-2024)

Source: IRENA; Guinness Global Investors, August 2025, percentile ranges from 2024 or 2023 if data is not available

As such, we expect longer-term wind installations to grow at 6-7% per year through 2030, with the smaller offshore market to grow at a higher rate of around 20%.

What is the long-term outlook for the global wind industry?

The wind industry will continue to grow at pace and capture a growing share of rising electricity demand.

We believe wind generation is well positioned to capture a growing share of rising global electricity demand, supported by continued improvements in technology and economies of scale that enhance its relative economics. With long-term targets updated in both China and Europe, the industry benefits from improved visibility, while in the US we see structurally higher power demand providing support for growth despite ongoing political headwinds.

The Guinness Sustainable Energy Fund aims to invest in companies involved in the generation, storage, and efficiency of sustainable energy sources, including but not limited to wind. Learn more about the fund and its investment philosophy here.

Disclaimer: This insight may provide information about Fund portfolios, including recent activity and performance and may contain facts relating to equity markets and our own interpretation. Any investment decision should take account of the subjectivity of the comments contained in this insight. This insight is provided for information only and all the information contained in it is believed to be reliable but may be inaccurate or incomplete; any opinions stated are honestly held at the time of writing but are not guaranteed. The contents of this insight should not therefore be relied upon. It should not be taken as a recommendation to make an investment in the Funds or to buy or sell individual securities, nor does it constitute an offer for sale.

Risk: The Guinness Sustainable Energy Fund, WS Guinness Sustainable Energy Fund & Guinness Sustainable Energy UCITS ETF are equity funds. Investors should be willing and able to assume the risks of equity investing. The value of an investment and the income from it can fall as well as rise as a result of market and currency movement; you may not get back the amount originally invested. The Funds are actively managed with the MSCI World Index used as a comparator benchmark only.