Gilts and energy shocks: an unhappy relationship

Before tensions over Iran exploded into open conflict, the market had become increasingly comfortable with the broader global disinflation story. Gilts had rallied hard into the end of February on expectations of further Bank of England interest rate cuts, helped further by lower US Treasury yields. This made them vulnerable to a sharp reversal as war in the Middle East caused oil and gas prices to surge.

What happened

The energy shock has forced investors to rethink the inflation outlook, hitting gilts hard. At the worst of the move, UK 2-year yields rose from 3.52% at month-end to 4.17%, while 10-year yields rose from 4.23% to an intraday peak just under 4.80% on 9th March, before settling at 4.69% at the close on 11th March. Around 50 basis points of interest rate cuts that were priced at the end of February were effectively stripped out during the sell-off.

Why were gilts especially vulnerable?

The UK remains especially sensitive to higher energy prices. Sharp moves in oil and gas, therefore, tend to feed quickly into UK inflation concerns and the expected Bank of England path, whatever the origin of the shock. With inflation still above target at 3% year-on-year (based on the Consumer Prices Index) the market reacted aggressively to the risk that higher energy prices could interrupt what had started to look like a more reliable disinflation trend.

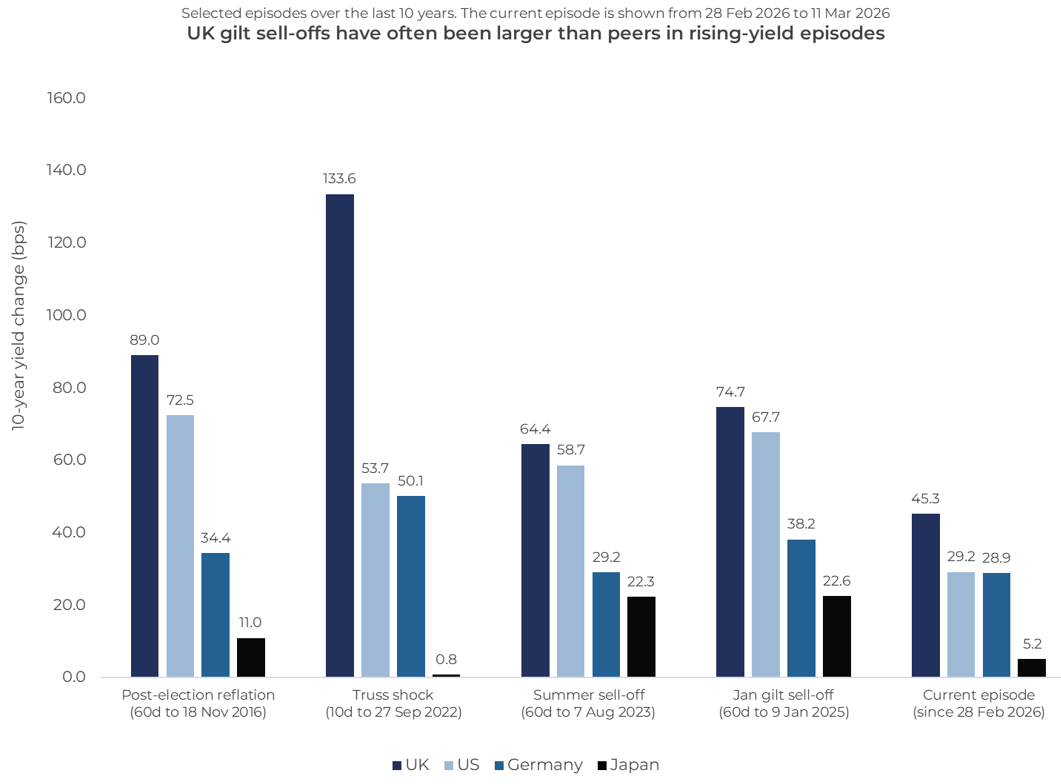

It is also worth noting what this sell-off was not. In the last such episode in January 2025, the pressure came from broader global bond weakness, sticky inflation concerns and investor worries about the implications of higher yields for the UK’s fiscal position. This time the catalyst was different, and importantly, other major bond markets including the US, Germany and Japan were much less sensitive. As the chart below shows, in the five selected rising-yield episodes over the past decade, UK 10-year yields moved further than peers, even when the original issue was not specifically UK-focused.

Source: Bloomberg, Guinness calculations, as of 11th March 2026

The UK-centric Truss shock in September 2022 was the most extreme, with gilts selling off by 134 basis points against just 54 basis points for US Treasuries. But even in episodes where the original trigger was global, such as the post-election reflation of 2016, or the summer sell-off of 2023, gilts still moved more. The current episode, at 45 basis points versus 29 for the US and Germany, is significant but not yet in the same league as those earlier dislocations. That context matters: it suggests the move is serious and consistent with historical patterns but does not yet represent an extreme or disorderly outcome.

The wider implications

Gilts matter beyond the sovereign market itself. They form the risk-free base for GBP-denominated corporate bonds, so a sharp move higher in gilt yields pushes up financing costs more broadly across sterling credit markets. More generally, when underlying government yields rise sharply, even very high-quality corporate bonds can suffer meaningful price declines through duration alone. Alphabet’s 100-year bond, for example, was down around 7% in price terms at one point from month-end levels.

In rate markets, sharp moves are often amplified by positioning and technical levels, not just fundamentals, and that appeared to be the case here. The size of the sell-off and the subsequent rally both show that markets are still trading headlines rather than a settled macro conclusion.

What does this mean for investors?

At current levels, gilt yields are becoming more attractive, even if the oil price and inflation backdrop are still settling. It is notable that when 10-year gilt yields approached 5% in January 2025, buyers did start to emerge, including very large real-money investors who saw value in shorter-dated gilts at those levels.

The front end and belly of the curve look most interesting after this repricing. A prolonged energy shock would also raise downside risks to growth and could ultimately become recessionary, which in time would argue for lower yields. Higher yields improve the starting point for investors, and around key technical levels, the market can quickly shift from forced selling to value-based buying. If yields were to move materially further out of line with UK economic data or other developed bond markets, and if energy prices begin to stabilise, my bias would be to start leaning back into gilts.

Disclaimer: This insight may provide information about Fund portfolios, including recent activity and performance and may contain facts relating to bond markets and our own interpretation. Any investment decision should take account of the subjectivity of the comments contained in this insight. This insight is provided for information only and all the information contained in it is believed to be reliable but may be inaccurate or incomplete; any opinions stated are honestly held at the time of writing but are not guaranteed. The contents of this insight should not therefore be relied upon. It should not be taken as a recommendation to make an investment in the Funds or to buy or sell individual securities, nor does it constitute an offer for sale.