Sustainable Energy - June Commentary

Portfolio Manager, Specialist Team

Portfolio Manager, Specialist Team

This is a marketing communication. Please refer to the prospectus, supplement and KID/KIID for the Funds before making any final investment decisions. The value of this investment can fall as well as rise as a result of market and currency fluctuations. You may not get back the amount you invested.

Past performance does not predict future returns.

The IEA (International Energy Agency) recently released its annual World Energy Investment report, which highlights continued growth in global energy spending and an ongoing shift towards renewables and electrification. Recent disruption to energy markets has reinforced the importance of energy security, prompting greater investment in domestic generation, electricity networks, electrification and efficiency. While the geopolitical backdrop remains uncertain, the report's conclusions are broadly consistent with our longer-term outlook for the energy transition characterised by increasing renewable penetration, rising electricity demand and continued improvements in energy efficiency.

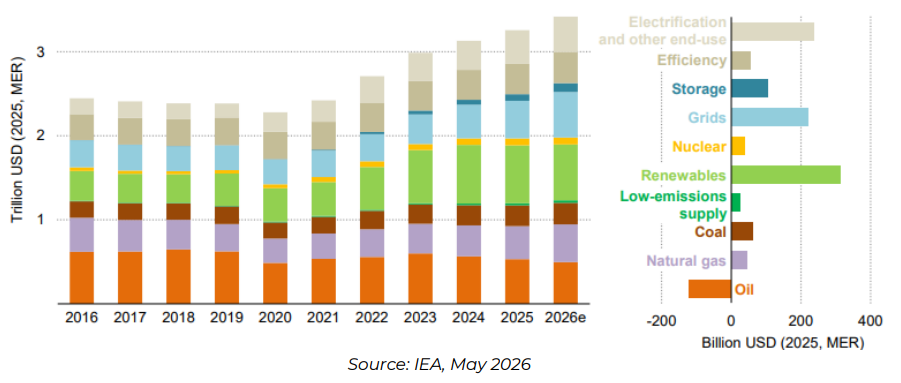

Global energy investment continues to rise

The IEA expects investment into the energy sector to grow 5% year-on-year in 2026, reaching $3.4 trillion. This would mark the sixth consecutive year of growth following a period that saw investment fall 3% per year between 2015-2020. The majority of this investment, around $2.2 trillion, is expected to go towards the energy transition, funding renewables, storage, low-emission fuels, and efficiency and electrification. Despite the ongoing conflict in the Middle East, the IEA still expects meaningful investment into conventional energy, with the oil, natural gas, and coal industries expected to spend a further $1.2 trillion.

Annual global energy investment, 2016-2026e; Change in investment 2016-2026e

Source: IEA, May 2026

Electrification is driving global energy investment

The IEA's report highlights the growing importance of electricity within the global energy system. Electricity-related investment now accounts for almost 60% of total energy spending and is expected to approach $2 trillion in 2026 across generation, grids and storage, and end-use technologies. Electricity demand growth is accelerating, particularly in advanced economies due to the growth in electric vehicles, heat pumps, cooling technologies, industry and recently from data centres. However, the composition of that investment is changing. Increasingly, capital is being directed towards the infrastructure required to support a more electrified energy system. We now consider some of the key themes emerging from the report.

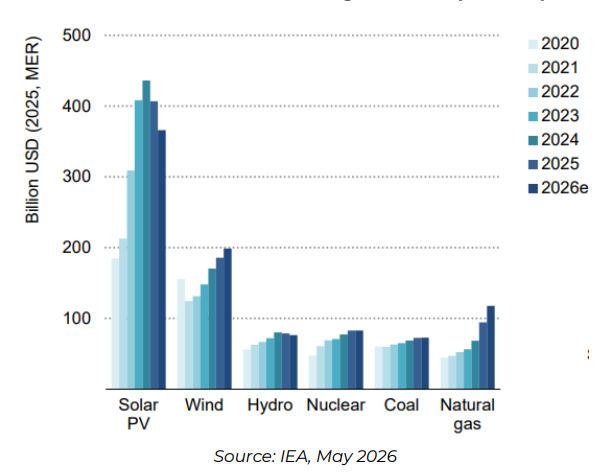

Renewables continue to dominate power generation investment

Renewable energy remains at the centre of global power sector investment, accounting for around 70% of generation spending according to the IEA. Annual investment now stands at approximately $665 billion, with solar attracting around $365 billion and wind a further $200 billion. While investment growth has moderated somewhat since 2024, this appears to reflect lower technology costs, particularly in solar, alongside policy changes in major markets such as China and the US. Natural gas is expected to see the largest step up in spending in 2026, reflecting rising power demand and increasingly tight power markets.

- Solar: Investment remains the largest within the power sector at around $365 billion per year. While overall spending has slowed since 2024, the IEA attributes this largely to falling costs rather than weaker demand, suggesting deployment should continue to grow strongly.

- Wind: Investment continues to grow and likely reaches around $200 billion in 2026. Growth is tempered due to permitting, policy and project execution challenges in some markets.

- Hydro: Investment is expected to remain around $75 billion per year, broadly in line with recent years, providing a stable source of low-emission generation and system flexibility.

- Nuclear: Investment is expected to remain flat in 2026 at around $80bn, having grown steadily in recent years. China will likely continue to drive near-term growth, with approvals still running at around 10 reactors per year. Looking further ahead, increasing policy support across the US, Europe and the UK should broaden the growth base and support a constructive long-term outlook for the global nuclear industry.

Global Investment into new generation ($ billion)

Source: IEA, May 2026

Looking forward, the IEA expects renewables to be a key beneficiary of the conflict in the Middle East. For many fuel-importing countries, domestically generated electricity offers a means of reducing exposure to volatile fossil fuel markets while improving the resilience of the energy system. The report highlights signs that this process is already underway:

- The Philippines, which declared a national energy emergency in March, imported three times more Chinese solar panels in the first quarter of 2026 than during the same period a year earlier.

- Across Africa, 15 countries reported solar imports of more than $400 million in the first quarter of 2026, compared with $650 million for the whole of 2025.

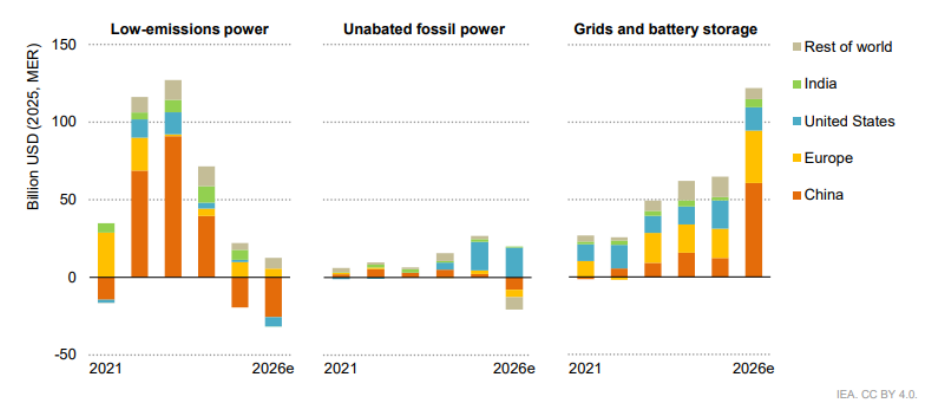

Power sector investment is shifting towards grids and battery storage

As renewable penetration continues to increase, investment is broadening from generation towards the infrastructure needed to support a more electrified economy. Electricity networks and battery storage are becoming increasingly important in maintaining system reliability and integrating new renewable capacity.

A reason for the acceleration in spending is that grid investment has lagged generation in recent years, resulting in growing constraints across electricity networks, with the IEA estimating that almost 600 GW of renewable projects in late-stage development are currently awaiting grid connection. In response, governments are increasingly prioritising network investment and introducing measures designed to accelerate grid expansion and improve connection times.

- In the UK, Ofgem has approved $13.6 billion to reinforce the electricity transmission network, improve reliability, and expand capacity for electrification.

- The European Commission has introduced a ‘European Grids Package’, allocating $565 million to network expansion.

- In China, State Grid has approved a $100 billion investment programme for 2026.

- India plans to invest $91 billion in transmission infrastructure by 2035-36 to address acute network bottlenecks.

In combination with rising grid spending, investment in battery energy storage systems (BESS) is expected to grow 30% in 2026, reaching almost $80 billion. BESS have an increasingly important role to play with growing renewable penetration given their ability to store energy during periods of surplus solar photovoltaic and wind production and release it during peak demand.

Ultimately, the IEA expects global grid investment to approach $550 billion in 2026, while spending on battery storage is set to exceed $100 billion.

Annual year-on-year investment growth for the power sector by category, 2021-2026e

Source: IEA, May 2026

Energy security considerations will accelerate efficiency investments and electrification

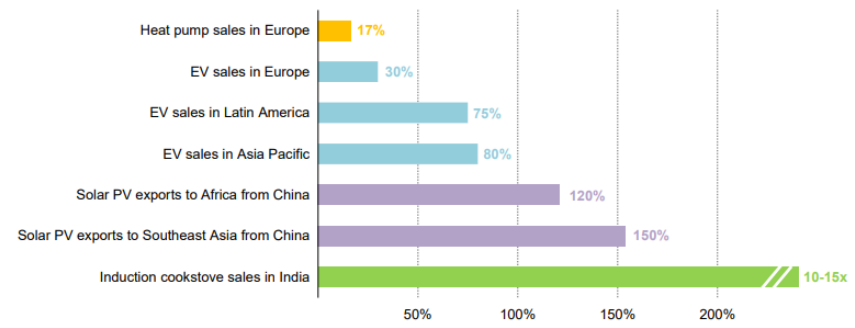

With energy security returning to the top of the policy agenda, the IEA expects investment in energy efficiency to continue rising. Efficiency spending on buildings, transport and in industry has already proved relatively resilient, reaching around $366 billion in 2025 and reflecting the importance of energy costs to households and businesses even outside periods of crisis. In the context of recent supply disruption, the case for efficiency becomes stronger still given its ability to structurally reduce energy consumption and fossil fuel import dependency.

While it remains too early to determine the full impact of recent events on efficiency investment, there is already evidence that higher energy prices are influencing consumer and business behaviour. The IEA notes that heat pump sales in Europe increased by 17% in the first quarter of 2026, while EV sales across Europe, Latin America and Asia Pacific rose by between 30% and 80%. Similarly, solar deployment has accelerated in parts of Africa and Southeast Asia, with exports from China up between 120% - 150%.

Growth in spending Q1 2025 – Q1 2026

Source: IEA, May 2026

Longer-term implications

The IEA’s findings point to an energy transition that is progressing at speed, with investment increasingly flowing towards the parts of the system required to support electrification and rising power demand. This is consistent with our longer-term view of the energy transition: driven less by policy and more by structural demand growth, improving economics and the need for secure, reliable power, with investment focused on grids, generation and storage to enable a more electrified global energy system.

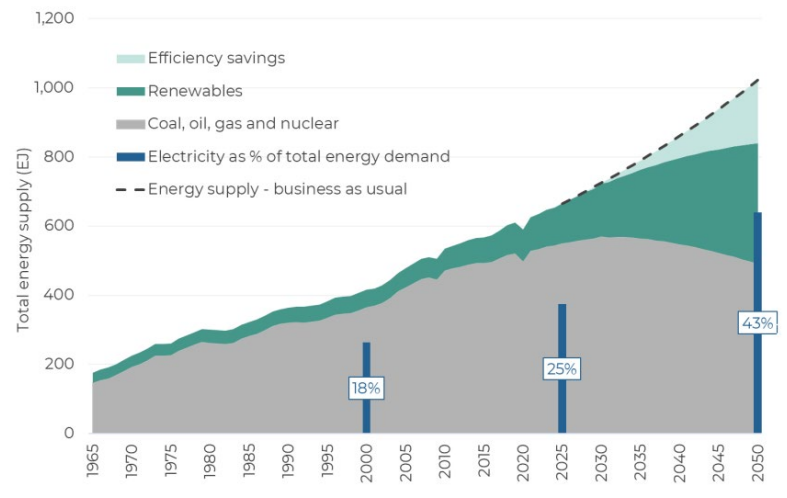

Global Energy Supply, 1965-2050e

Source: Guinness Global Investors, June 2026

Conclusion

The IEA's latest report reinforces a number of themes that have been shaping the energy transition for many years. Investment in renewables continues to grow, supporting an increasingly low-carbon electricity system, while investment is now broadening into the grids, storage and infrastructure needed to support rising levels of electrification. The conflict in the Middle East has brought energy security back to the forefront of policymaking and is likely to accelerate several trends already evident across the global energy system. In our view, the report reinforces our long-held view of the transition, characterised by rising renewable penetration, improving energy efficiency and increasing electrification across transport, buildings and industry.

For our full report, including analysis of fund returns in May, click below.

The value of this investment can fall as well as rise as a result of market and currency fluctuations. You may not get back the amount you invested.

The information provided on this page is for informational purposes only. While we believe it to be reliable, it may be inaccurate or incomplete. Any opinions stated are honestly held at the time of publication, but are not guaranteed and should therefore not be relied upon. This content should not be relied upon as financial advice or a recommendation to invest in the Funds or to buy or sell individual securities, nor does it constitute an offer for sale. Full details on Ongoing Charges Figures (OCFs) for all share classes are available here.

The Guinness Sustainable Energy Funds invest in companies involved in the generation, storage, efficiency and consumption of sustainable energy sources (such as solar, wind, hydro, geothermal, biofuels and biomass). We believe that over the next twenty years the sustainable energy sector will benefit from the combined effects of strong demand growth, improving economics and both public and private support and that this will provide attractive equity investment opportunities. The Funds are actively managed and use the MSCI World Index as a comparator benchmark only.

For the avoidance of doubt, if you decide to invest, you will be buying units/shares in the Fund and will not be investing directly in the underlying assets of the Fund

Guinness Sustainable Energy Fund

Documentation

The documentation needed to make an investment, including the Prospectus, the Key Investor Information Document (KIID), Key Information Document (KID) and the Application Form, is available in English from www.guinnessgi.com or free of charge from the Manager: Waystone Management Company (IE) Limited, 2nd Floor 35 Shelbourne Road, Ballsbridge, Dublin DO4 A4E0, Ireland; or the Promoter and Investment Manager: Guinness Asset Management Ltd, 18 Smith Square, London SW1P 3HZ.

Waystone IE is a company incorporated under the laws of Ireland having its registered office at 35 Shelbourne Rd, Ballsbridge, Dublin, D04 A4E0 Ireland, which is authorised by the Central Bank of Ireland, has appointed Guinness Asset Management Ltd as Investment Manager to this fund, and as Manager has the right to terminate the arrangements made for the marketing of funds in accordance with the UCITS Directive.

Investor Rights

A summary of investor rights in English, including collective redress mechanisms, is available here: https://www.waystone.com/waystone-policies/

Residency

In countries where the Funds are not registered for sale or in any other circumstances where their distribution is not authorised or is unlawful, the Funds should not be distributed to resident Retail Clients. NOTE: THIS INVESTMENT IS NOT FOR SALE TO U.S. PERSONS.

Structure & Regulation

The Funds are sub-funds of Guinness Asset Management Funds PLC, an open-ended umbrella-type investment company, incorporated in Ireland and authorised and supervised by the Central Bank of Ireland, which operates under EU legislation. The Funds have been approved by the Financial Conduct Authority for sale in the UK. If you are in any doubt about the suitability of investing in these Funds, please consult your investment or other professional adviser.

Switzerland

This is an advertising document. The prospectus and KID for Switzerland, the articles of association, and the annual and semi-annual reports can be obtained free of charge from the representative in Switzerland, Reyl & Cie SA, Ru du Rhône 4, 1204 Geneva. The paying agent is Banque Cantonale de Genève, 17 Quai de l'Ile, 1204 Geneva.

WS Guinness Sustainable Energy Fund

Documentation

The documentation needed to make an investment, including the Prospectus, the Key Investor Information Document (KIID) and the Application Form, is available in English from www.waystone.com/our-funds/waystone-fund-services-uk-limited/ or free of charge from Waystone Management (UK) Limited, PO Box 389, Darlington DL1 9UF.

General enquiries: 0345 922 0044

E-Mail: wtas-investorservices@waystone.com

Waystone Management (UK) Limited is authorised and regulated by the Financial Conduct Authority.

Residency

In countries where the Fund is not registered for sale or in any other circumstances where its distribution is not authorised or is unlawful, the Fund should not be distributed to resident Retail Clients.

Structure & regulation

The Fund is a sub-fund of WS Guinness Investment Funds, an investment company with variable capital incorporated with limited liability and registered by the Financial Conduct Authority.

This Fund is registered for distribution to the public in the UK but not in any other jurisdiction. In other countries or in circumstances where its distribution is not authorised or is unlawful, the Fund should not be distributed to resident Retail Clients.

Guinness Sustainable Energy UCITS ETF

Documentation

The documentation needed to make an investment, including the Prospectus, the Key Investor Information Document (KIID), Key Information Document (KID) and the Application Form, is available in English from www.guinnessgi.com, www.hanetf.com or free of charge from the Administrator: J.P Morgan Administration Services (Ireland) Limited, 200 Capital Dock, 79 Sir John Rogerson’s Quay, Dublin 2 DO2 F985; or the Investment Manager: Guinness Asset Management Ltd, 18 Smith Square, London SW1P 3HZ.

Residency

In countries where the Fund is not registered for sale or in any other circumstances where its distribution is not authorised or is unlawful, the Fund should not be distributed to resident Retail Clients. NOTE: THIS INVESTMENT IS NOT FOR SALE TO U.S. PERSONS.

Structure & regulation

The Fund is a sub-fund of HANetf ICAV, an Irish collective asset management vehicle umbrella fund with segregated liability between sub-funds which is registered in Ireland by the Central Bank of and authorised under the UCITS Regulations.