Greater China - February Commentary

Director, Chief Investment Officer, Portfolio Manager

Portfolio Manager, Asian & Emerging Markets

This is a marketing communication. Please refer to the prospectus, supplement and KID/KIID for the Funds before making any final investment decisions. The value of this investment can fall as well as rise as a result of market and currency fluctuations. You may not get back the amount you invested.

Past performance does not predict future returns.

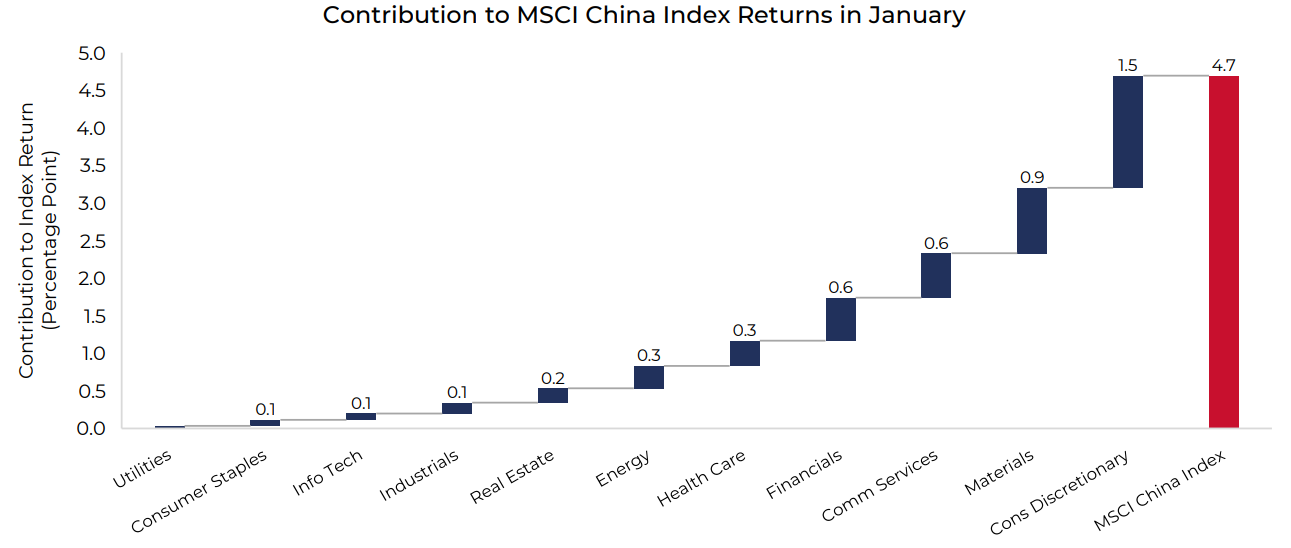

Chinese equities were strong in January as Consumer Discretionary stocks outperformed (led by Alibaba, which introduced new features) and Communication Services stocks rose on the prospect of rising AI demand. Materials stocks benefited from the rise in metal prices including gold.

Source: Data from 31/12/25 to 31/01/26, returns in USD, source: Bloomberg, Guinness Global Investors calculations

Source: Data from 31/12/25 to 31/01/26, returns in USD, source: Bloomberg, Guinness Global Investors calculations

In this commentary we analyse the drivers of Fund returns over the month. We consider the macro picture at the start of 2026 as countries continue to improve relations with China, driven by US policymaking becoming more unpredictable.

Finally, in light of the Fund's overweight to Industrials, we highlight how our holdings are set to benefit from the AI infrastructure build-out and the associated increase in demand for power.

The value of this investment can fall as well as rise as a result of market and currency fluctuations. You may not get back the amount you invested.

The information provided on this page is for informational purposes only. While we believe it to be reliable, it may be inaccurate or incomplete. Any opinions stated are honestly held at the time of publication, but are not guaranteed and should therefore not be relied upon. This content should not be relied upon as financial advice or a recommendation to invest in the Funds or to buy or sell individual securities, nor does it constitute an offer for sale. Full details on Ongoing Charges Figures (OCFs) for all share classes are available here.

The Guinness Greater China Fund is designed to provide investors with exposure to economic expansion and demographic trends in China and Taiwan. The Fund is managed for capital growth and invests in profitable companies generating persistently high return on capital over the business cycle. The Fund is actively managed with the MSCI Golden Dragon used as a comparator benchmark only.

For the avoidance of doubt, if you decide to invest, you will be buying units/shares in the Fund and will not be investing directly in the underlying assets of the Fund

Documentation

The documentation needed to make an investment, including the Prospectus, the Key Information Document (KID) / Key Investor Information Document (KIID) and the Application Form, is available from the website www.guinnessgi.com , or free of charge from:

the Manager: Waystone Management Company (IE) Limited 2nd Floor 35 Shelbourne Road, Ballsbridge, Dublin DO4 A4E0; or, the Promoter and Investment Manager: Guinness Asset Management Ltd, 18 Smith Square, London SW1P 3HZ.

Waystone IE is a company incorporated under the laws of Ireland having its registered office at 35 Shelbourne Rd, Ballsbridge, Dublin, D04 A4E0 Ireland, which is authorised by the Central Bank of Ireland, has appointed Guinness Asset Management Ltd as Investment Manager to this fund, and as Manager has the right to terminate the arrangements made for the marketing of funds in accordance with the UCITS Directive.

Investor Rights

A summary of investor rights in English, including collective redress mechanisms, is available here: https://www.waystone.com/waystone-policies/

Residency

In countries where the Funds are not registered for sale or in any other circumstances where their distribution is not authorised or is unlawful, the Funds should not be distributed to resident Retail Clients. NOTE: THIS INVESTMENT IS NOT FOR SALE TO U.S. PERSONS.

Structure & Regulation

The Fund is a sub-fund of Guinness Asset Management Funds PLC, an open-ended umbrella-type investment company, incorporated in Ireland and authorised and supervised by the Central Bank of Ireland, which operates under EU legislation. The Funds have been approved by the Financial Conduct Authority for sale in the UK. If you are in any doubt about the suitability of investing in these Funds, please consult your investment or other professional adviser.

Switzerland

This is an advertising document. The prospectus and KID for Switzerland, the articles of association, and the annual and semi-annual reports can be obtained free of charge from the representative in Switzerland: Reyl & Cie SA, Ru du Rhône 4, 1204 Geneva. The paying agent is Banque Cantonale de Genève, 17 Quai de l'Ile, 1204 Geneva.

Singapore

The Fund is not authorised or recognised by the Monetary Authority of Singapore (“MAS”) and shares are not allowed to be offered to the retail public. The Fund is registered with the MAS as a Restricted Foreign Scheme. Shares of the Fund may only be offered to institutional and accredited investors (as defined in the Securities and Futures Act (Cap.289)) (‘SFA’) and this material is limited to the investors in those categories.