The power of real assets in an unstable market environment

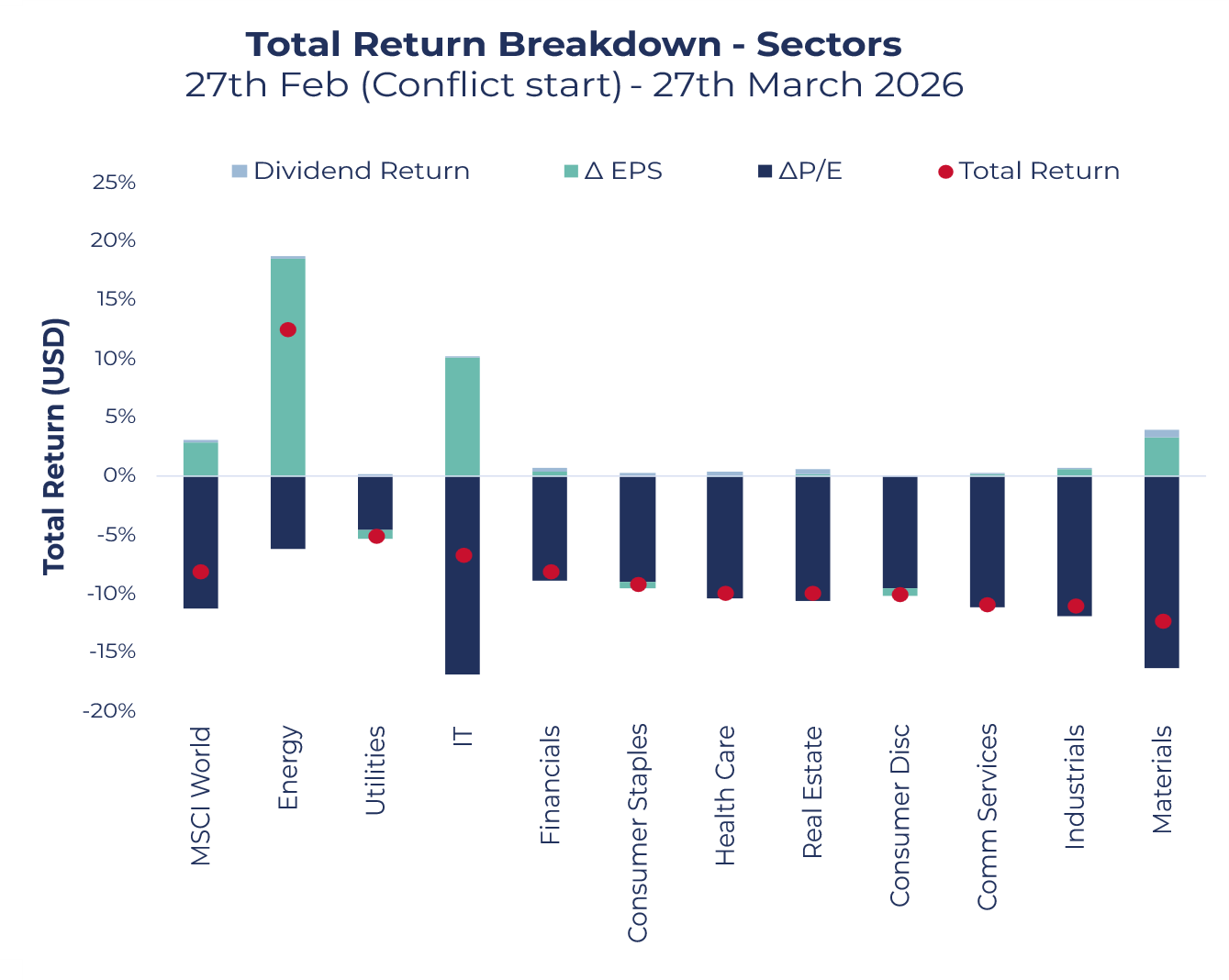

Energy equities have seen positive performance since the conflict

Among equity sectors, Energy has led performance and remains the only one in positive territory for total returns in 2026. Utilities have been the next best performer, with the sector’s classic defensive characteristics providing investors with some shelter from the economic uncertainty rippling through global markets.

Source: MSCI, Bloomberg, Guinness Global Investors, March 2026

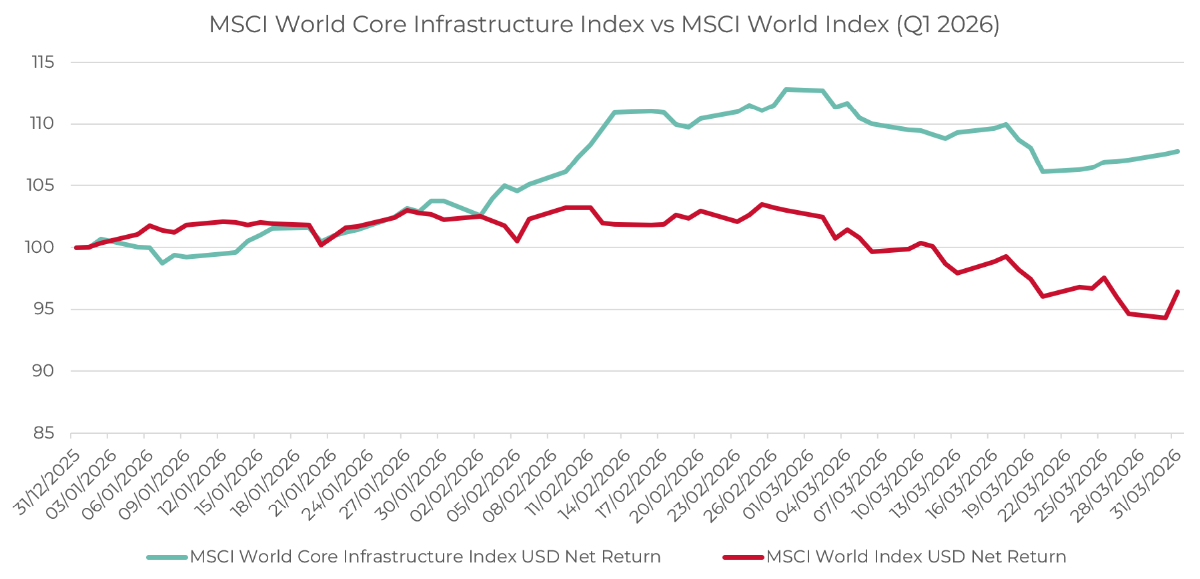

Infrastructure has outperformed equity markets overall this year

Meanwhile, indexes dominated by utilities and energy infrastructure such as the MSCI World Core Infrastructure Index have materially outperformed the MSCI World Index.

The chart below shows returns for these two indexes for Q1 2026, rebased to 100, with the MSCI World Infrastructure Index delivering both positive absolute performance and strong relative outperformance.

Source: Bloomberg, Guinness Global Investors, March 2026

Part of the explanation for the outperformance of real asset-focused sectors rests on the emergence of the so-called HALO trade: Heavy Assets and Low Obsolescence. This investment strategy focuses on companies with significant tangible assets, long-term economic importance, and resistance to AI-linked disruption. Examples include energy networks, water treatment, and waste collection. This move was underway before the outbreak of war, but it essentially signals the market beginning to recognise the value of asset-heavy businesses, which are potentially less exposed to AI disruption and displacement.

The outbreak of war has also shone a light on the importance of many HALO businesses, particularly in utilities, which have regulated business models, high barriers to entry, and support vital economic activity.

What can we expect from the real assets sector?

The war in the Middle East has created three related drivers for the real assets sector as its consequences unfold. These are an energy shock, the resulting inflationary pressure, and in turn, changes to the path of interest rates.

1. The energy shock’s implications for the sector

The implications of the emerging energy shock differ across real asset sectors and regions, particularly between the US and Europe. In terms of sectors, the principal area impacted is utilities and power producers.

Impact on the US utilities

US utilities are broadly less exposed to fossil fuel supply constraints given domestic supply capabilities. Supply constraints in the Middle East could, in reality, be positive for US gas exports to Europe, thereby supporting the energy infrastructure companies that move gas across North America to export terminals.

Impact on Europe utilities

European utilities have greater direct exposure to developments in energy and power markets, particularly amid the spike in gas prices. In the short term, depending on the levels of short-term hedging, this should create upside opportunities for generators which can capture higher spot prices.

On the defensive side, networks-focused regulated utilities should see limited disruption to their financial outlook. In the long term, the current war further highlights Europe’s vulnerability to disruptions in fossil fuel supply. This could, and arguably should, reinforce and accelerate policy support for the continued development and roll-out of renewable energy, storage and the associated infrastructure.

Energy security, system resilience, and a continued transition away from fossil-fuel dependence are likely to be among the primary focus areas for European governments following the current crisis.

2. Inflationary pressures

The spectre of rising inflation already looms over Europe and the global economy, depending, of course, upon how long we see disrupted and elevated energy prices. Real asset-owning companies are generally well positioned to help protect against inflationary pressure given their contracted indexation (a mechanism in long-term contracts that automatically adjusts prices based on an index, such as the Consumer Price Index) and provision of essential services, which can often enable inflation costs to be passed through.

While the current geopolitical turmoil and energy disruption are different to those resulting from Russia’s invasion of Ukraine and the emergence from Covid, the sector's performance during that sharp inflation spike is nonetheless an interesting comparator. The biggest rise in inflation came in 2022, and over that year, the MSCI World Core Infrastructure Index meaningfully outperformed the MSCI World Index, as shown in the re-based chart below:

Source: Bloomberg, Guinness Global Investors, March 2026

If we see inflation begin to rise significantly again, the sector could offer relative safety amid wider equity markets, as it has done so far in 2026.

3. Interest rates

Just as the energy shock affects inflation, it must also affect interest rates. Before the war, expectations in developing markets were of continued cuts through the rest of 2026. These expectations have now been tempered by the prospect of inflationary pressure.

The real asset sector is highly sensitive to interest rate movements, which can act as headwind depending on the speed and severity of any upward move. It is thus an important consideration when assessing the sector. However, across the real asset-owning companies, we do observe improving fundamentals in terms of earnings growth and higher-quality balance sheets that should help to mitigate adverse valuation impacts, if indeed we did see a new rate tightening cycle in response to inflation. Equally, slowing economic growth could pull monetary policy pressure in the other direction.

While such an environment could become stagflationary and therefore generally a headwind for markets, infrastructure and real estate companies are well positioned to perform well relative to the broader market given the essential nature of the services they provide and the inflation-linked nature of their cashflows.

Why real assets continue to deliver

Whilst each conflict and energy shock is different, history shows that real asset-owning equities can deliver defensive performance in the face of uncertainty, supported by long-term investment trends and often backed up by regulation and government support. The story so far for the sector in 2026 is in line with this thesis.

The Guinness Global Real Assets Fund continues to be focused on high-quality infrastructure and real estate companies diversified across regions and business models. The Fund’s focus on listed equities provides investors with highly liquid exposure to a sector typically considered illiquid. Learn more about the Fund and its investment philosophy here.

Risk: The Guinness Global Real Assets Fund is an equity fund. Investors should be willing and able to assume the risks of equity investing. The value of an investment and the income from it can fall as well as rise as a result of market and currency movement, and you may not get back the amount originally invested. For full information on the risks, please refer to the Prospectus, Supplement, and KID/KIID for the Fund, which will be available in English at Fund launch on our website (guinnessgi.com/literature).

The Fund is actively managed with the MSCI World Core Infrastructure Index used as a comparator benchmark only. The Global Real Assets Fund invests primarily in Global companies which pay dividends.

Disclaimer: This insight may provide information about Fund portfolios, including recent activity and performance and may contains facts relating to equity markets and our own interpretation. Any investment decision should take account of the subjectivity of the comments contained in this insight. This insight is provided for information only and all the information contained in it is believed to be reliable but may be inaccurate or incomplete; any opinions stated are honestly held at the time of writing but are not guaranteed. The contents of this insight should not therefore be relied upon. It should not be taken as a recommendation to make an investment in the Funds or to buy or sell individual securities, nor does it constitute an offer for sale.