Opportunities in Semiconductors

Whilst 2023 saw a downturn in semiconductor demand, semiconductor stocks outperformed the broader market.

Following three years of very strong growth amid the covid pandemic, the semiconductor industry faced a downturn during 2023 – the seventh since 1990. Global sales fell approximately 10-12% as customers worked through inventories built up during widespread supply chain disruption following the pandemic, and a weakened macro-outlook dampened demand. Memory chips (semiconductors used for internal storage within a computer) performed particularly badly, with weak consumer demand and excess channel inventory on the whole causing prices for DRAM (Dynamic Random Access Memory) and NAND memory chips (which make up the majority of the segment) to fall by over 50% in the first half of the year (according to Gartner). Non-memory chips fared far better during the downturn, facing an overall decline of c.3% during the year. While they felt similar headwinds such as weakened demand and excess channel inventory, pricing held up – in fact, excluding memory, pricing per unit was up double digits. In addition, the demand for non-memory chips for artificial intelligence purposes offset most of the declines elsewhere.

Counterintuitively, the semiconductor market was the best performing industry (by Global Industry Classification Standard (GICS)) during 2023; the MSCI World Semiconductor Index rose 90% over the year vs the MSCI World’s 24%. While this was in part driven by the strength of one Magnificent Seven stock in particular, Nvidia (+238% USD), broad-based gains were seen across the market, with the average semiconductor stock within the Philadelphia Semiconductor Index up 45%.

The Fund’s overweight position to the industry is a function of our bottom-up process.

Whilst we are certainly bullish on the long-term outlook of the semiconductor industry and note its exposure to many secular growth themes, our overweight position is a result of our investment process – focusing on bottom-up stock selection rather than attempting to make top-down macro calls. Our bottom-up approach has four key tenets: Growth, Quality, Valuation and Conviction.

- Growth drives long-term returns. We focus on companies with exposure to long-term secular growth themes, that are expected to grow faster than the market over time, and which may offer more predictable, sustainable growth.

- Quality protects against downside risks. We focus on high and consistent return on capital, balance sheet strength, and sustainable competitive advantages. Valuation is important; we aim to avoid overpaying for (uncertain) future growth.

- Conviction is reflected in our high active share, 30-stock, equal-target-weight portfolio, long-term, low-turnover approach.

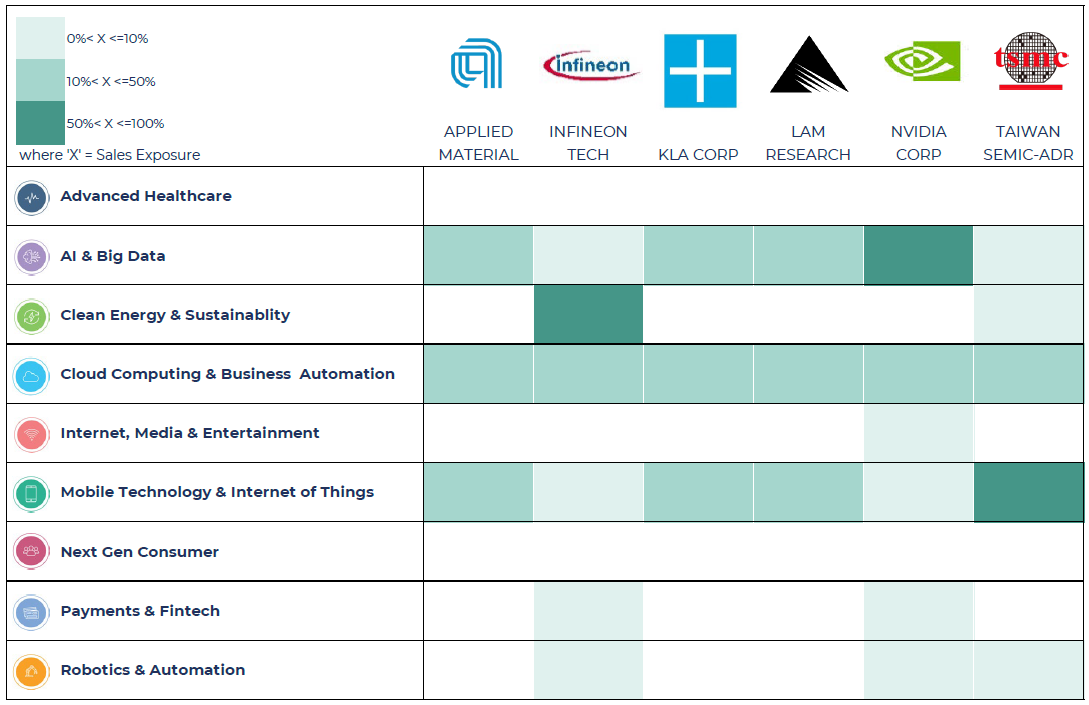

Our six holdings in the semiconductor industry are exposed to many of the growth themes we have identified whilst also exhibiting the characteristics we seek in terms of growth, quality, and valuation.

Source: Guinness Global Investors estimates from company reports and literature. February 2024

Semiconductor companies are an important driver of global innovation, and thus, need to be innovative themselves

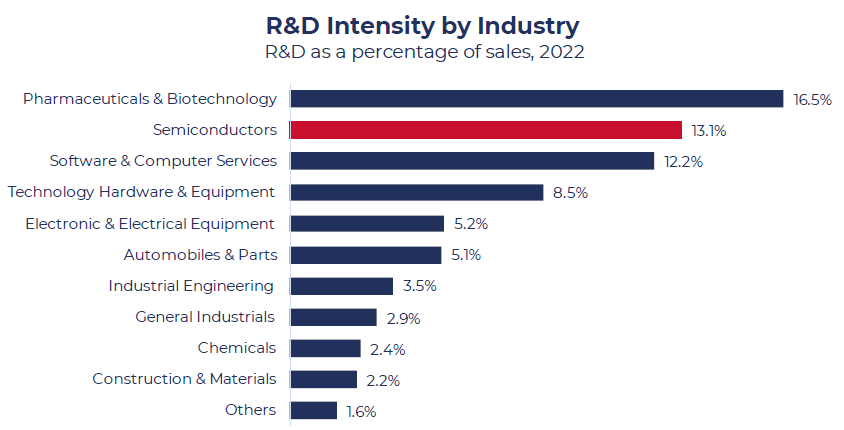

Semiconductors act as one of the fundamental building blocks for technological advancement. Companies across end markets are continually demanding increasingly complex, high-performing and efficient chips, across an expanding number of applications and different system requirements – all to drive innovation within their own products. For semiconductors to meet these increasing demands, they need to innovate themselves. At the ‘leading edge’, innovation is focused on shrinking the size of the ‘node’, and thus increasing the number of transistors per chip. Over several decades, progress in this area has seemingly followed Moore’s Law: that the number of transistors on a chip will double every two years, leading to an exponential increase in computational power and efficiency. TSMC has been at the forefront of this progress and is able to produce chips at the 3 nanometre ‘node’, with a 2nm node offering 30% more efficiency expected by 2025. Even at the ‘trailing edge’ – older, more mature semiconductor technologies – innovation is still important. Here, rather than pushing the limits of what is possible and where size may not be as important (such as in power chips), innovation is focused on improving the reliability and efficiency of chips, potentially through material science. Infineon is an example in this space, using a different architecture named ‘trench’ technology which has superior performance in power semiconductors, as well as investing in the innovative use of materials such as silicon carbide. To facilitate this innovation, the semiconductor industry is one the most intense in research and development (as a proportion of sales), second only to Pharma in 2022.

Source: EU Industrial R&D Investment Scoreboard; IC Insights; Guinness Global Investors

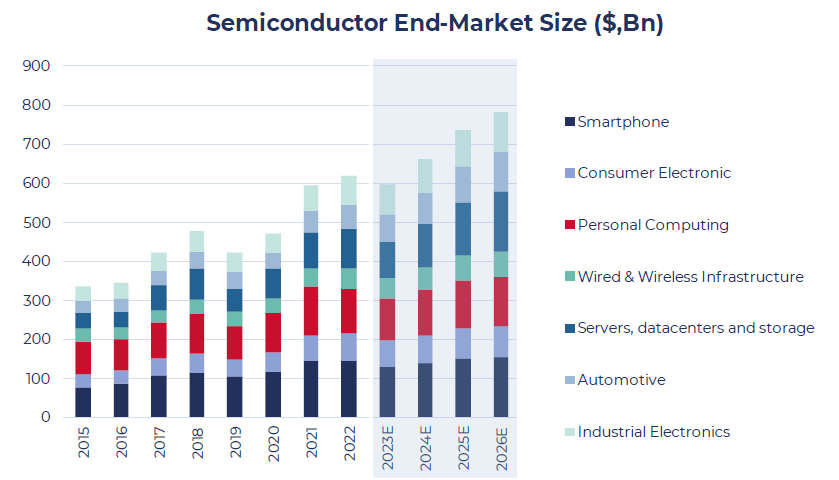

While this is clearly a significant cost for semiconductor companies, a high investment allocation to R&D not only creates high barriers to new entrants, but allows the industry to continue growing, not only by providing improved, more complex and powerful semiconductors, but facilitating the development of new technologies in different categories and industries – as seen with the progress made in generative artificial intelligence across sectors over the course of 2023. Consequently, the semiconductor market has grown rapidly over the past decade. The chart below shows data and estimates taken from a presentation by semiconductor equipment manufacturer ASML at the beginning of 2023, highlighting not only the significant historical growth (9.1% annually between 2015-2023) across a broad range of end markets, but the significant growth expectations for the future. Although these estimates did not reflect the c.10% decline seen in 2023 (the actual end market size ended at c.$530bn, according to Gartner), they are also unlikely to reflect the longer-term consequence of progress made with respect to generative AI during the year. Assuming the market can reach $1trillion by 2030-2032 (as multiple sources suggest e.g. IDC, Gartner and McKinsey), this would deliver c.7-10% annual growth (2023-2030) – broadly in line with the historical trend.

Source: ASML Investor Day November 2022, Annual Report 2022 (released February 2023)

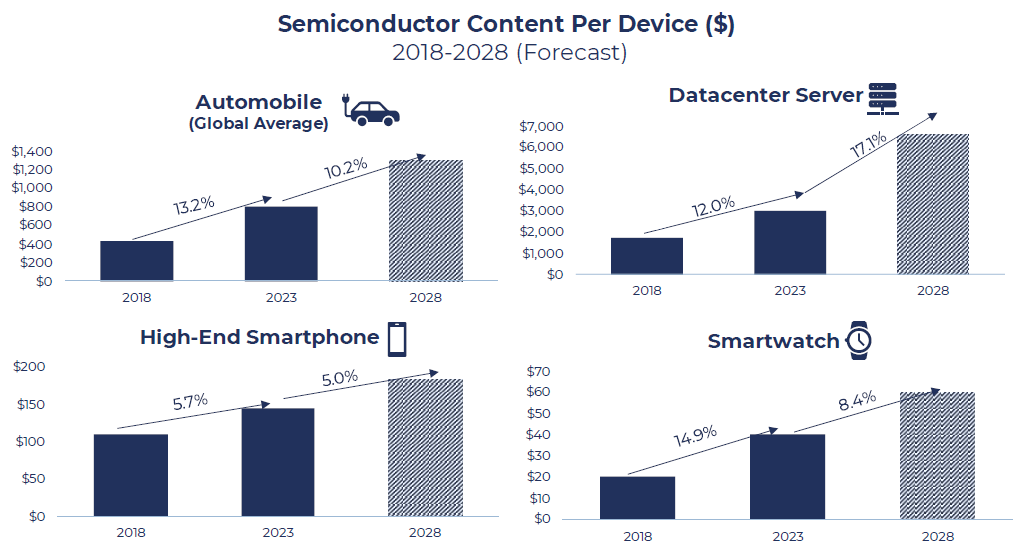

- Automotive: Growth in the auto semiconductor end-market (14% annually through to 2030, according to Bernstein) is expected to far outpace the broader sector, with long-term trends such as digitalisation, electrification and autonomous driving increasing the complexity and content of semiconductors within vehicles. Semiconductor content per vehicle averaged around $600-700 in 2021, and has nearly doubled from $320 in 2014. It is expected to reach $2000 by 2030. Semi content roughly doubles from an internal combustion engine vehicle to a battery or plug-in hybrid electric vehicle, and the expectation that EVs (full or hybrid) will make up more than 50% of car production by 2027, a significant tailwind to demand. In addition, the increasing complexity and prevalence of infotainment systems will also drive semiconductor content within vehicles.

- Datacentre is expected to be the second fastest growth sector over the remainder of the decade (+13% annually, Bernstein). We have seen rapidly increasing demand for cloud computing capacity across industries, not only due to more businesses and industries migrating on-premise infrastructure over to the cloud, but the rise of ‘Big Data’ and more data-centric analytics boosting demand for more efficient servers, and thus more complex, efficient and powerful processors. Furthermore, advances in artificial intelligence, particularly following developments in generative AI during 2023, require specialised hardware that has the ability to handle complex and energy-intensive computations, with datacentres providing the necessary infrastructure for both the training and running of AI systems.

The increasing demands and complexity of the underlying products within these two industries are resulting in greater ‘semiconductor content per device/unit’ (measured as the dollar amount). However, this phenomenon isn’t just present within Automotive and Datacentre, but across many other use cases, as seen by the below estimates from Soitec.

Source: Guinness Global Investors, Soitec Capital Markets Day 2023

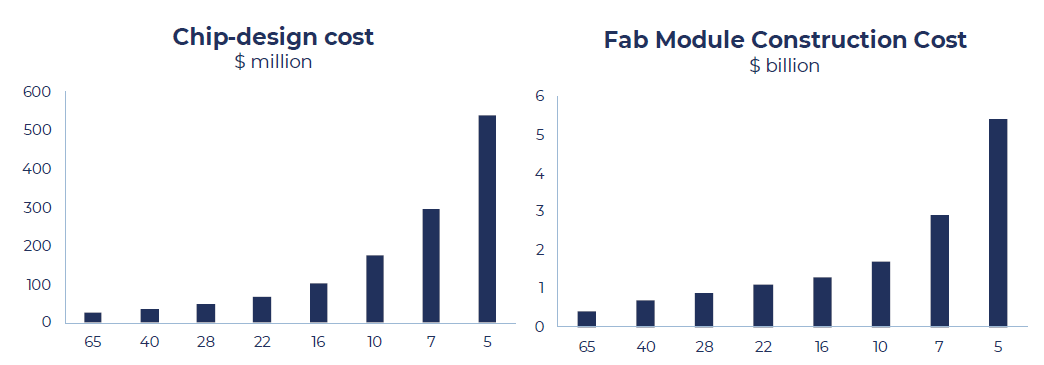

Facilitating the development of faster, more efficient and powerful chips at the leading edge is not cheap.

We have already seen that the semiconductor industry is one of the most R&D-intensive industries, and part of the reason is the costs associated with fitting more transistors onto a given area. Advancing to smaller technologies becomes more and more complex, meaning that at each ‘node’ (the minimum distance between transistors on a chip) the cost increase is significant. The ‘chip-design’ cost can be seen below, showing an exponential rise in the development costs of each node. Whilst no data is available yet, the 3nm node is expected to be c.$1bn. The more significant cost, however, is the cost of the fabrication module (semiconductor factory), which is expected to be c.$5-6bn at the 5nm node. The cost of TSMC’s 3nm proposed fabrication plant is estimated to be $20bn, highlighting a significant acceleration in the costs required to progress the technology further.

Source: McKinsey, IB, Guinness Global Investors, August 2020

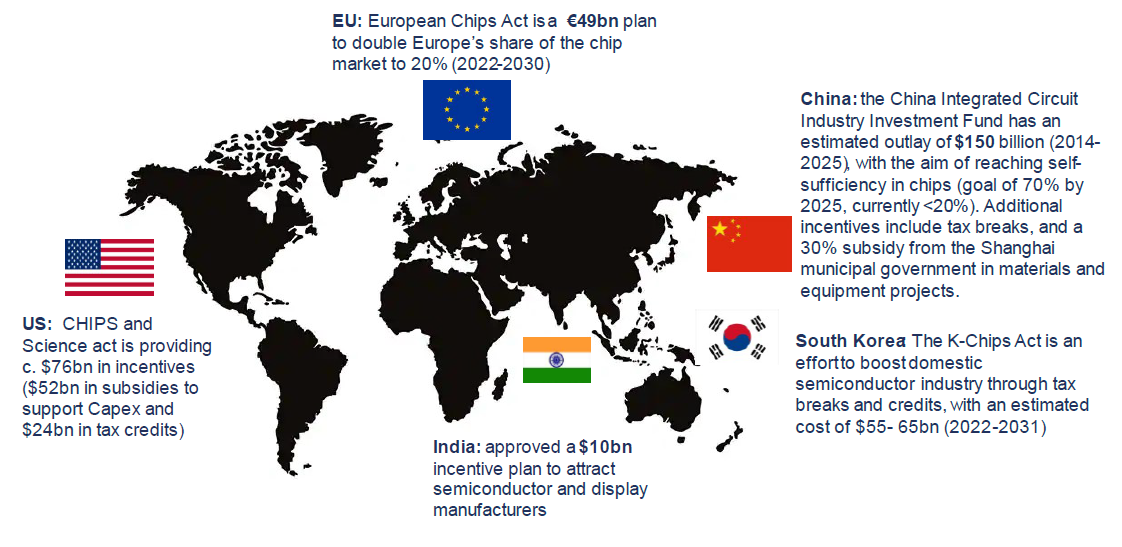

Geopolitical tensions have driven governments to offer significant subsidies to accelerate the onshoring of chipmaking facilities.

The covid-19 pandemic exposed vulnerabilities in the semiconductor supply chain, with varying lockdown measures across regions driving severe shortages in many areas of the chip markets. The global nature of the supply chain can be illustrated by this excerpt from Chris Miller’s 2022 book Chip War:

“A typical chip might be designed with blueprints from the Japanese-owned, UK-based company called Arm, by a team of engineers in California and Israel, using design software from the United States. When a design is complete, it’s sent to a facility in Taiwan, which buys ultrapure silicon wafers and specialised gases from Japan. The design is carved into silicon using [precision] tools produced primarily by five companies, one Dutch, one Japanese, and three Californian. […] The chip is then packaged and tested, often in Southeast Asia, before being sent to China for assembly.”

The supply chain disruption exacerbated existing underlying tensions and concerns over national security and supply chain stability. Strained relations between the US and Chinese governments have resulted in sanctions and restrictions over exports between the two countries since 2017, with the US ultimately aiming to limit China’s ability to acquire and manufacture chips at advanced nodes and thus slowing efforts to gain a meaningful foothold in industry and become self-sufficient. The US’s vulnerability is clear. Whilst accounting for 25% of global semiconductor demand, the US possesses just 12% of global manufacturing capacity. Other regions have also weighed in to obtain their own slice of the rapidly growing and critical industry, with the EU, Japan, Korea and India all offering additional subsidies to incentivise chipmakers to build on their shores.

Source: Guinness Global Investors, RBC Wealth Management, February 2024

One concern with government subsidies is that they typically lead to the misallocation of capital. We do not expect this to be the case for the semiconductor industry since the subsidies are coming at a time when companies need to ramp up capacity in order to service the long-term underlying growth trends. Either way, semiconductor equipment manufacturers such as Lam Research and KLA Corp stand to benefit from these long-term capex cycles.

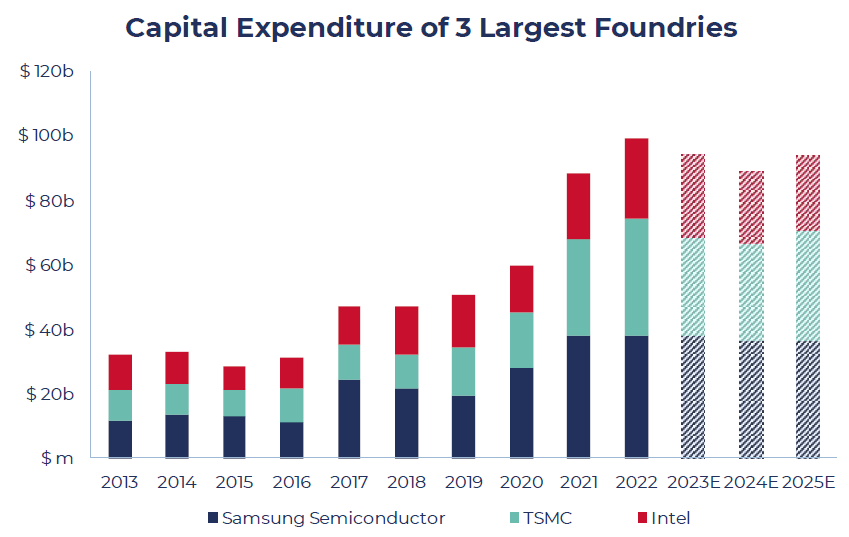

Foundries have responded with significant ramp-ups in capex.

At the end of 2023, there were around 50 new semiconductor fabrication plants (or ‘fabs’) being built globally (Z2Data), and an additional 23 expansions to existing sites. 40% of builds are in the US, with the value of US-based semiconductor projects that are either announced or under consideration coming to over $200bn through to 2030 (McKinsey, ZData). Around 16 fabs are being built that will focus on 10nm nodes or smaller. Intel committed $100bn to capex on chip plants between 2022- 2032, Samsung $150bn in its foundry unit until 2030, and while TSMC slightly cut capex expectations to 2024, expectations remain above $30bn annually. Although 2023 and 2024 are expected to see slight year-on-year declines among the largest chipmakers with respect to capex, this comes amid a slight semiconductor downturn and a high interest rate environment. Looking forward, in a stronger demand environment where interest rates are falling, we expect this spend to be at least stable, with the top three contributing at least $80bn annually over 2023-2025. Even beyond the big three foundries, we have also seen integrated device manufacturers such as Infineon ($5.5bn over the next five years towards its Malaysian Kulim plant) and Texas Instruments ($5bn annually to 2026) continuing to commit large-scale capex despite a weakening demand environment.

Source: Guinness Global Investors, Bloomberg, company reports. Data for 2023 onwards are estimates.

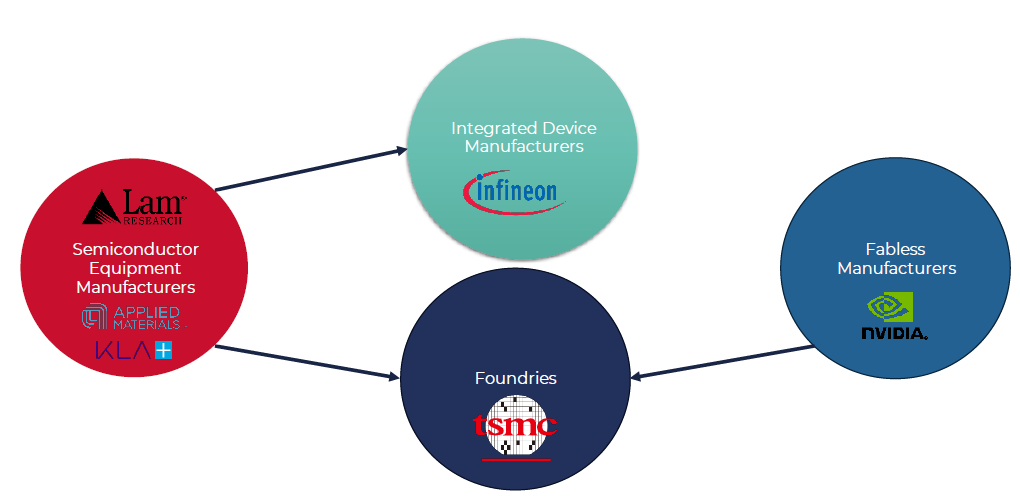

Against this backdrop, we see significant opportunity across the value chain. A simplified diagram of the Semiconductor value chain is shown below, along with Fund holdings within the sector. As a brief reminder, Semiconductor Equipment Manufacturers design, produce and sell equipment used in the fabrication of semiconductor devices, often specialising in areas such as photolithography, deposition and etching, or focusing on particular types of chips. They sell their equipment to foundries, who specialise in the physical manufacture of semiconductors. ‘Fabless manufacturers’ are the designers of the chip, who outsource to foundries. An Integrated Device Manufacturer is essentially a fabless manufacturer and a foundry combined – they manufacture their own chips. Within the Guinness Global Innovators portfolio, we hold a diversified set of semiconductor companies across regions and across the semiconductor value chain.

Source: Guinness Global Investors

We can look at these companies through the lens of some of the strategy’s key tenets.

| Position in Value Chain | Company | Growth Thesis |

|---|---|---|

| Fabless Manufacturers |  | Nvidia is positioned at the centre of exploding demand seen for artificial intelligence, possessing over 95% market share of the GPUs (graphical processing units) required for generative AI systems, establishing the firm as the dominant chipmaker for AI model training. Whilst the risk to market share is certainly to the downside, this can be more than offset by the rapid growth and demand within the industry, and we expect the firm’s strong IP and technological edge to offer a strong economic moat in this instance. And whilst AI may now be the core growth driver for the firm, Nvidia is also exposed to a number of other long-term secular growth trends, including other areas of datacentre (high performance computing and edge computing/IoT), as well as the automotive industry (advanced driver assistance systems (ADAS) in particular). The firm is a natural beneficiary for the long-term secular trends discussed above. |

| Foundries |  | Like Nvidia, TSMC is a natural beneficiary of the strongly increasing demand for semiconductors across industries – particularly at the leading edge. The firm has been a pioneer in driving innovation at advanced nodes and is heavily investing in both fabs and R&D to maintain this reputation and drive the growth of the future. As one of three companies that can produce chips at the 3nm node (and the only pure-play foundry) and a market share of 59% (54% in Q1 2022), the firm is firmly positioned at the forefront of technological progress and will no doubt benefit from increasing demand across the semiconductor product spectrum. |

| Integrated Device Manufacturers |  | Infineon has positioned itself in some of the fastest growing areas of semiconductor markets, in particular within Automotive and Green Energy Transition. The firm has a leading position in Power Discrete and Modules, taking market share from 17-18% to 20% since 2016 and within the auto’s power semiconductor segment, the firm has three times the share of its nearest competitor (>30%). This is also a firm which is investing heavily in innovation; it is regarded as the technological leader in silicon carbide (SiC) and is now investing heavily in capacity (via a €5bn plant in Malaysia). The firm’s SiC-based chips offer higher performance within EVs and renewable energy products, in a segment of the market which is expected to undergo rapid market growth (c.30% annual growth from 2022-2028), with Infineon’s superior technology (trench technology vs planar, used by STM) expecting to drive market share gains from 20% to 30% over this period. |

| Semiconductor Equipment Manufacturers |    | We have discussed in detail the significant capex requirements for the future growth of the semiconductor industry – all supported by long-term secular growth themes (Artificial Intelligence, Cloud Computing, Energy Transition, Electric Vehicles and autonomous driving, etc) alongside the significant government subsidies on offer across regions to drive onshoring. Demand for new fabrication plants, both for technological advancement as well as capacity build-out, have resulted in significant capex commitments by firms such as TSMC, Intel, Samsung, Infineon and Texas Instruments. Together, these offer a significant tailwind for Semiconductor Equipment Manufacturers such as Applied Materials, KLA and Lam Research. Each is a market leader in some market vertical (KLA in Process Control, Lam in Etch and Applied Materials in Deposition and Epitaxy), offering significant exposure to these capacity build-outs. The ‘growth’ on offer for Semi Equipment Manufacturers is likely to be less cyclical and more consistent than the wider market, with multi-year factory build-outs allowing consistent demand – even if the underlying semiconductor market periodically weakens. |

Growth opportunity: We have already discussed the strong, underlying secular trends and growth within the industry, resulting in the expected c.7-10% annual industry growth between 2023-2030 – some of the key drivers being increasing semiconductor content per unit/device, the shift towards electric vehicles and autonomous driving solutions (and more intelligent solutions in general), big data and artificial intelligence driving growth in datacentre demand, alongside rising demand for electronic devices in general and new technologies (Internet of Things (IoT), edge computing, 5G etc). We have also discussed the significant capex requirements needed to achieve this.

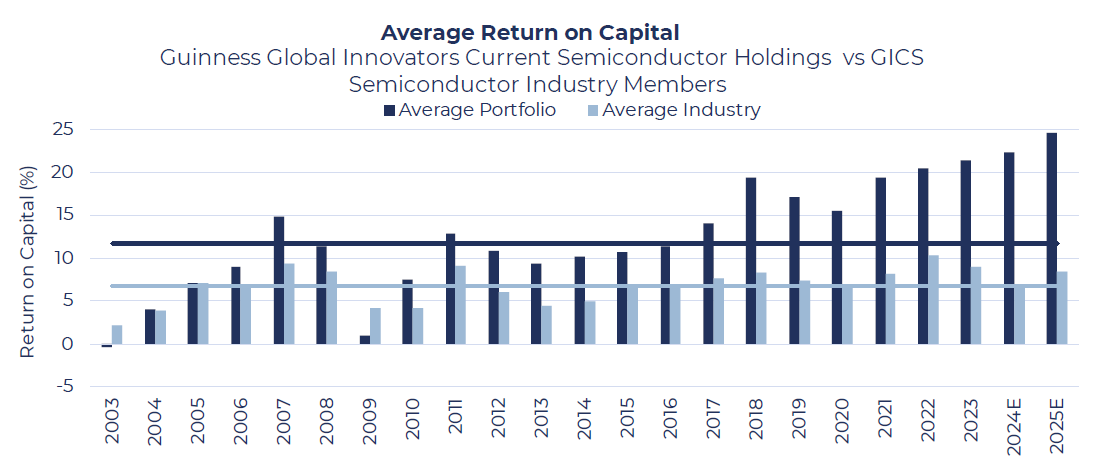

Quality: We place significant emphasis on the ‘quality’ of a firm. We believe that quality helps to mitigate against downside risks that a firm may be subject to. This is especially important in the semiconductor industry, which has grown hugely historically but has been highly cyclical. We have attempted to identify high-quality names within the industry using analysis of financial metrics such as return on capital, balance sheet strength, margin profile, and with a more qualitative perspective. Our portfolio holdings demonstrate a superior return on capital to the broader semiconductor market as seen over a 20- year history. While the market has seen declines since 2022, expected to continue next year, our average holding has shown continued growth over the same period. Over the past five years, our average holding has delivered a return on capital of 18.9% vs the average semiconductor industry member of 8.4%.

Source: Guinness Global Investors, Credit Suisse, February 2024. Data for 2024 onwards is estimated.

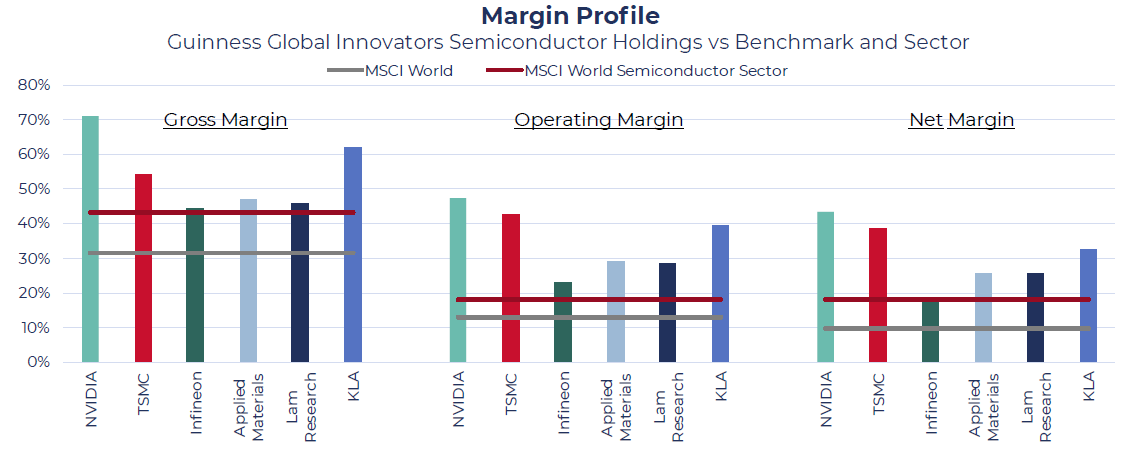

Fund semiconductor holdings also offer a far superior margin to the MSCI World benchmark, and better than the MSCI World Semiconductor sector.

Source: Guinness Global Investors, MSCI, Bloomberg, company reports, February 2024

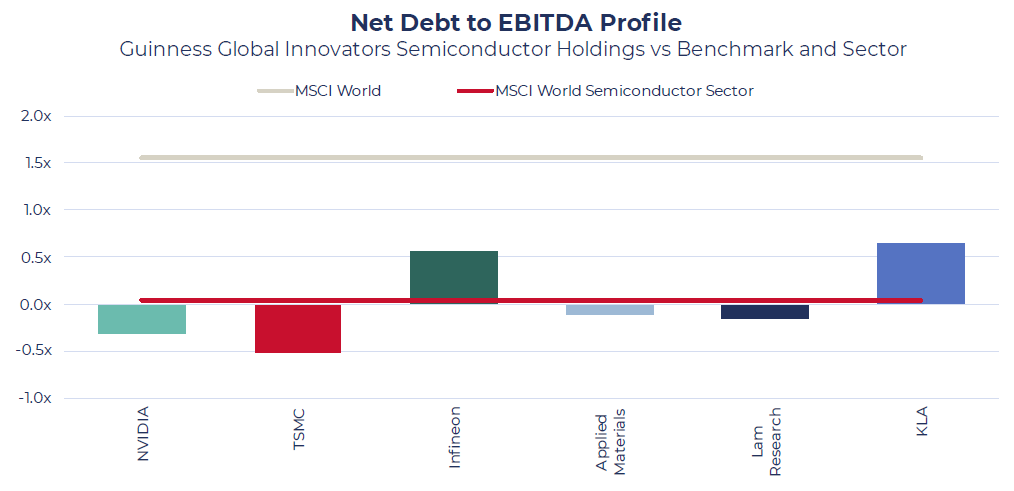

Our companies also exhibit greater balance sheet strength than the benchmark, with an average Net Debt to EBITDA (Earnings before Interest, Taxes, Depreciation, and Amortization) of 0x (the maximum being 0.6x), in-line with the MSCI World Semiconductor sector (likely skewed by Nvidia’s large weighting) but materially below the MSCI World benchmark 1.6x.

Source: Guinness Global Investors, MSCI, Bloomberg, company reports, February 2024

We also note the competitive advantages these businesses enjoy:

- High capex requirements create high barriers to entry. Whilst a high capex spend impacts the bottom line of the firm, it also acts as a high barrier to entry for new entrants, which are unable to fund the high up-front costs.

- Specialisation creates economies of scale, another barrier to entry that reduces competition. Many of our portfolio companies compete in highly specialised areas, such as Infineon in power chips. Semiconductor design and manufacturing require deep expertise, and focusing on a specific type of chip allows a company to concentrate its effort and resources on mastering the intricacies of that particular technology, but also create density in demand and thus economies of scale.

- High-IP industry. Our portfolio companies have been operational for over 20 years, generating significant intellectual property during that period. New entrants in any vertical would need to invest heavily to develop similar economies of learning.

- Global presence. Whilst trade war risks are relevant to companies with Chinese exposure, they are mitigated by a diversified revenue stream. Having diversification across our semiconductor holdings with respect to both region (e.g. Infineon is European-based, TSMC is based in Taiwan), and place in the value chain (e.g. trailing edge firms such as Infineon are facing less scrutiny than leading edge firms such as Nvidia with respect to trade risks) helps reduce the overall portfolio risk.

- Long-term secular growth trends, more stable returns. We believe these will drive more consistent demand over the medium term, leading to lower cyclicality within the industry overall, and our holdings in particular.

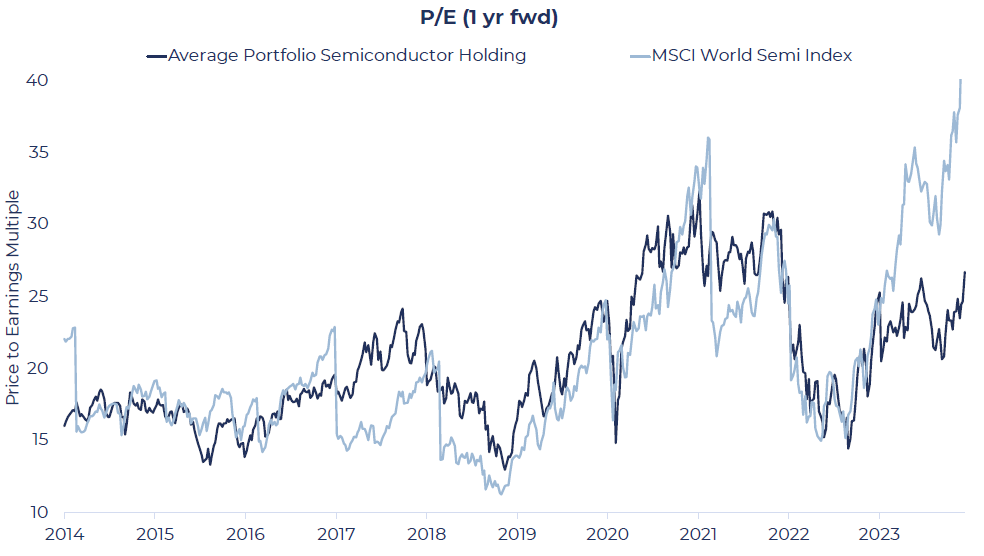

Valuation

Despite their superior characteristics, our holdings have, on average, typically been in line with the MSCI World Semiconductor Index valuation on a price/earnings (P/E) basis.

Source: Guinness Global Investors, MSCI, Bloomberg, to 31.01 .2014 to 31.01.2024. A simulation based on the historic data for the Fund's current holdings. The Fund was launched on 31.10.14. Calculations assume an equally weighted portfolio.

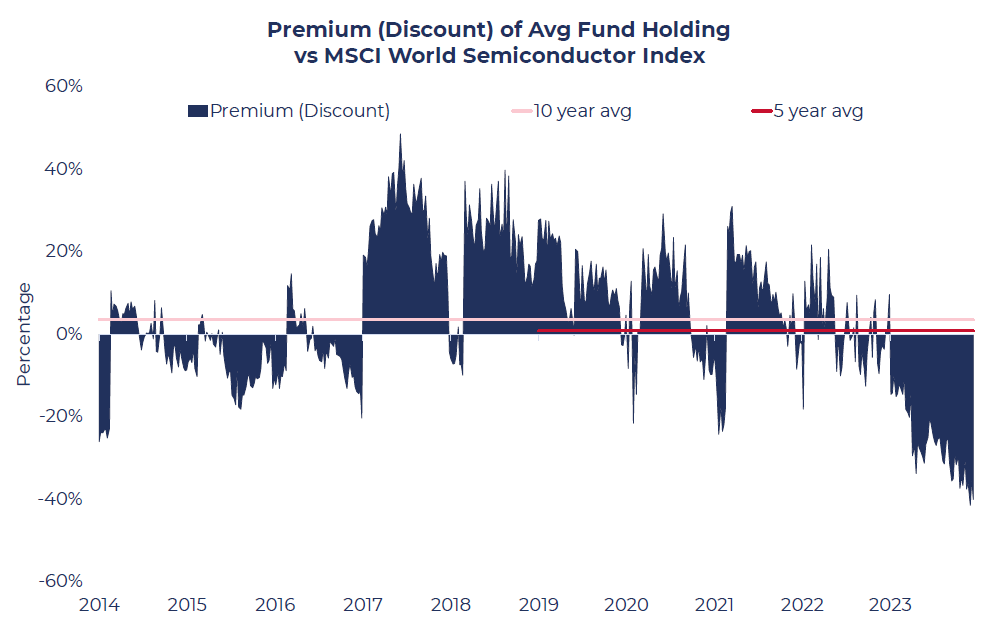

However, recently a significant discount has emerged.

Source: Guinness Global Investors, MSCI, Bloomberg, to 31.01.2014 to 31.01.2024. A simulation based on the historic data for the Fund's current holdings. The Fund was launched on 31.10.14. Calculations assume an equally weighted portfolio.

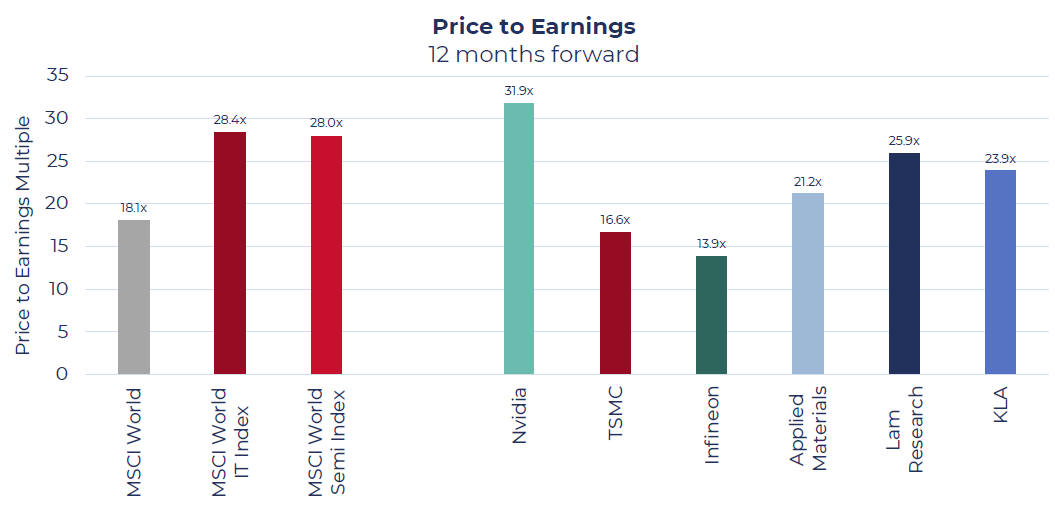

With the exception of Nvidia, all of our holdings are at a discount to the MSCI World Information Technology Index and the MSCI World Semiconductor Index today.

Source: Guinness Global Investors, MSCI, Bloomberg, as of 31.01.2024

We therefore continue to see good opportunities for the fund holdings in the semiconductor sector and believe they continue to have good pathways for future growth, and potential outperformance.

Risk: The Guinness Global Innovators Fund and WS Guinness Global Innovators Fund are equity funds. Investors should be willing and able to assume the risks of equity investing. The value of an investment can fall as well as rise as a result of market and currency movement; you may not get back the amount originally invested. The Funds are actively managed with the MSCI World Index used as a comparator benchmark only. The Fund invests in global equities. The companies invested in will have, in the manager's opinion, innovation at the core of their business.

The brochure, which can be accessed via the article links above and below, contains important information about the Fund and further details on the risk factors are included in the Funds’ documentation, available on our website (guinnessgi.com/literature)

Disclaimer: This Insight may provide information about Fund portfolios, including recent activity and performance and may contains facts relating to equity markets and our own interpretation. Any investment decision should take account of the subjectivity of the comments contained in the report. This Insight is provided for information only and all the information contained in it is believed to be reliable but may be inaccurate or incomplete; any opinions stated are honestly held at the time of writing but are not guaranteed. The contents of this Insight should not therefore be relied upon. It should not be taken as a recommendation to make an investment in the Funds or to buy or sell individual securities, nor does it constitute an offer for sale.