Opportunities in Innovation

INNOVATION IS MORE THAN JUST TECHNICAL ADVANCES

Innovation can impact a company’s products, services or business model. Innovation can be dramatic where companies create new markets or disrupt incumbents. Or it can be more subtle where innovation leads to small but important advances that create a sustainable competitive advantage. Ultimately, innovative companies can experience faster profit growth and higher profit margins while their secular growth opportunities mean they can be less susceptible to the economic cycle.

Studies show that innovative companies exhibit...

So how do we identify innovative companies? We begin each year by reviewing our core set of innovation themes. We currently have 9 core innovation themes that, we believe, present exciting long-term investment opportunities (we shall take a closer look at why later).

These themes are derived from our ongoing research into growth trends and where we feel the growth is being driven by innovation rather than regulation. There will be numerous sub-themes associated with each theme and the sub-themes will be updated more frequently than the core themes. We subsequently search for companies that have exposure to these themes using a broad array of resources to build a universe of innovative companies.

- Management consulting firm Arthur D. Little has found that “Top quartile innovation performers obtain on average 13% points more profit from new products and services”. Additionally, it concluded that “…the top quartile innovators enjoy more than twice the proportion of new sales for new products/services (based on sales in the last three years), nearly twice the EBIT and a 30% shorter time-to-break-even than the rest. This is a good illustration of financial (or economic) benefits of excellent innovation performance.”

- In another report, Arthur D. Little found that “achieving innovation excellence can boost EBIT margin by four percentage points through both top line growth and bottom line improvements”.

- A University of British Columbia study has also compared innovation “leaders” and innovation “laggards”, finding that innovation is “strongly associated with firms’ expected returns.” In particular, they found that “more innovative firms have lower exposure to systematic risk.”

HOWEVER, NOT ALL INNOVATIVE COMPANIES ARE GOOD INVESTMENTS

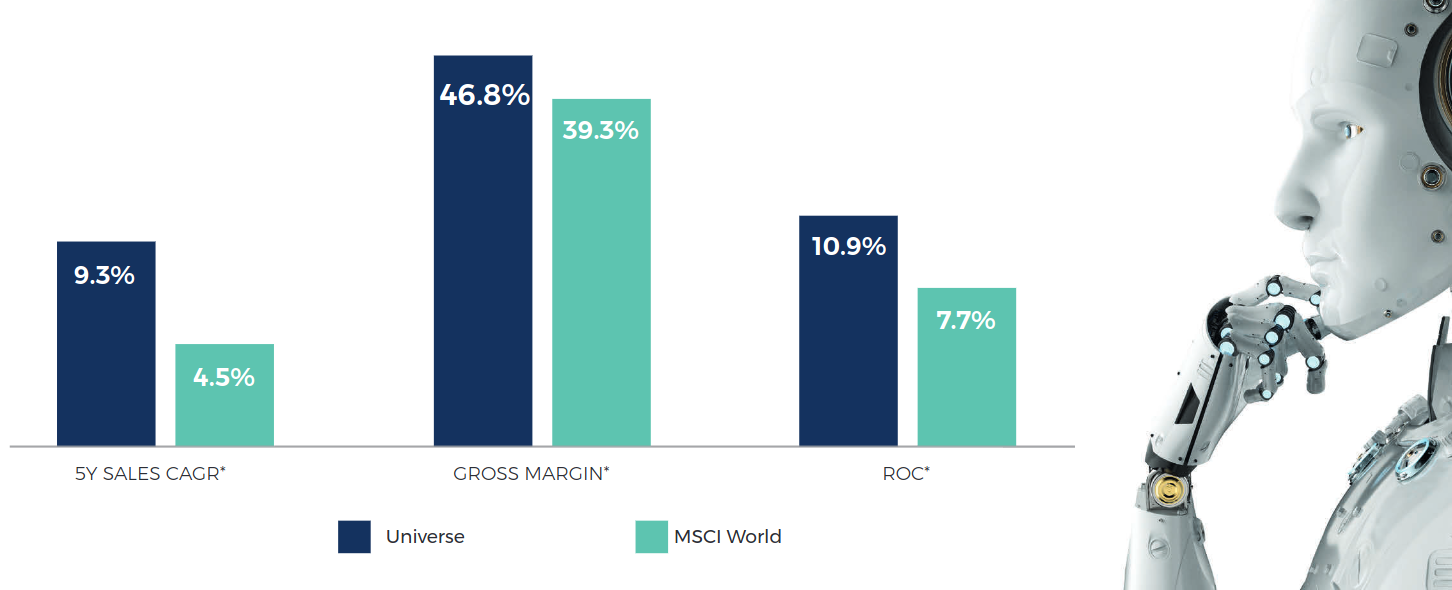

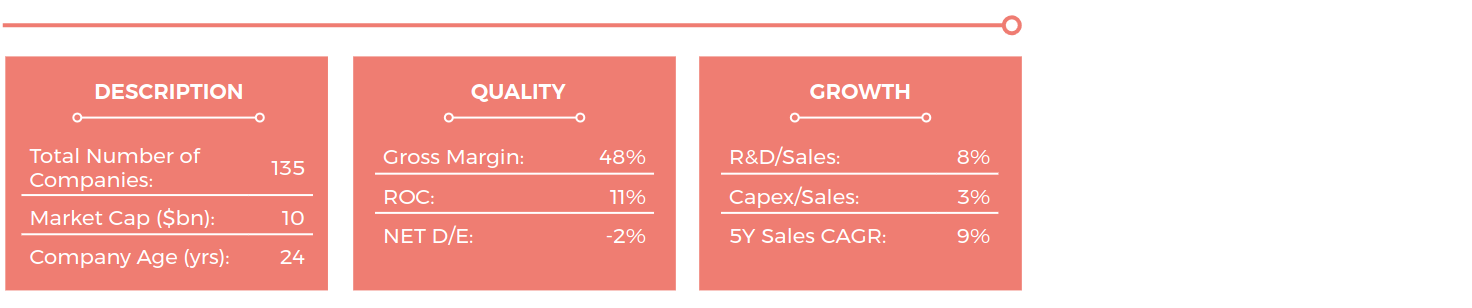

Quite often early stage businesses that have identified a niche in the market or are reinventing an existing product tend to require substantial external financing to reach critical mass and maintain growth rates – in some cases never transforming from a cash-burning business into a cash-generative one. However, it is not just early stage businesses that pose a risk: mature companies that may have once been labelled as innovative may see their competitive advantage erode as they themselves are disrupted. Consequently, these businesses wind up with deteriorating returns-on-capital. In order to avoid these companies we focus in on those with quality financial characteristics: namely, those creating economic value, possess robust balance sheets, and have profitable growth prospects. This leads us to our investible universe. Upon inspection, the benefi ts of investing in innovative businesses, outlined in the three academic studies referenced on the previous page, are evident in our investible universe below. The companies in our universe demonstrate faster historic sales growth, wider margins, and greater return-on-capital versus the median MSCI World constituent.

Global Innovators Universe Statistics vs MSCI World

In the following pages, we will take a closer look at our 9 innovation themes, giving colour to the rationale behind the investment prospect and categorising the themes based on certain characteristics. We examine the opportunity set, looking at the investment opportunities and example companies within each theme.

ADVANCED HEALTHCARE

ADVANCED HEALTHCARE

Sub Themes: BioTech, Genomics, Speciality Pharmaceuticals, MedTech

Global demand for healthcare continues to rise thanks to changing demographics, higher standards, economic growth, and innovation. In addition to the advances seen in drug discovery, disruptive technological advances in other sectors including retail, transportation and manufacturing seem set to carry over into healthcare; from robotic surgery to augmented reality headsets and artificial intelligence (AI) used in diagnosis, the healthcare of tomorrow will continue to evolve.

At the most disruptive end of the healthcare spectrum, biotechnology has made great advances, particularly in genomics, where the cost to sequence a whole human genome has fallen from $150mn in 2003 to $1k today – outpacing Moore’s Law. The possibility of replacing or editing the building blocks of human DNA - that translates into everything from eye colour to severe diseases such as Parkinson's - was once reserved to the realm of science fiction. While there will be many regulatory hurdles to overcome, and the ethics of gene editing will undoubtedly come into question, the necessary applications of curing or possibly eradicating mutations that would lead to disease in later life seem obvious.

In a continually evolving healthcare landscape, hospitals and medical practitioners are becoming more efficient in their work as medical technology becomes more prominent in daily routines: remote patient monitoring, video-calling check-ups and wearable sensors create an ecosystem of connected devices via which a patient’s health can be monitored. This is enabling greater access to healthcare, greater data collection, and the automation of symptom detection. Consequently, incremental innovations in healthcare, be they through drug discoveries or medical technologies, are creating a spectrum of opportunities from an investment perspective. These range from the disruptive end of genomics, offering high growth (albeit at considerable premiums), to the relatively more stable MedTech businesses, which benefit from high proportions of recurring revenues.

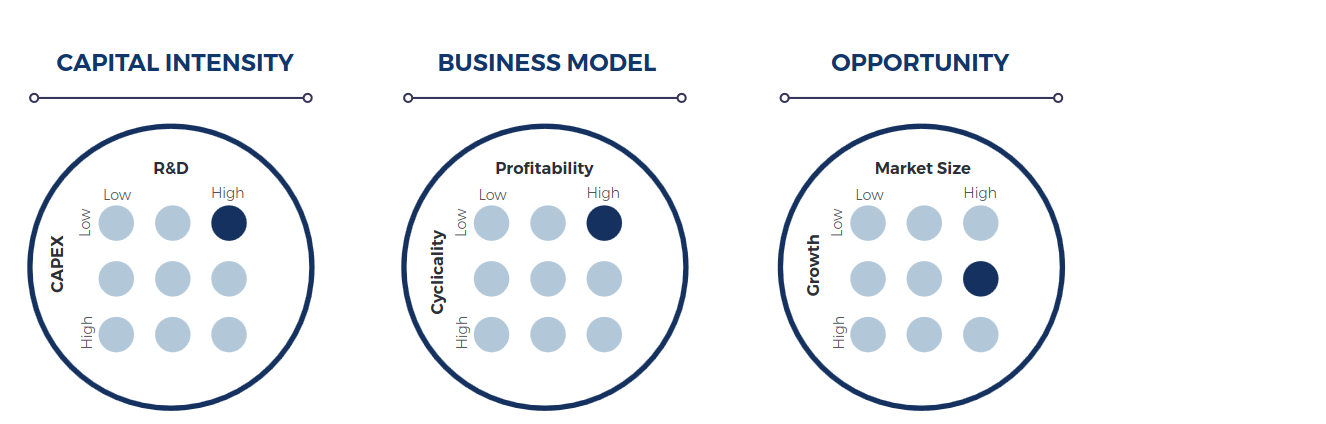

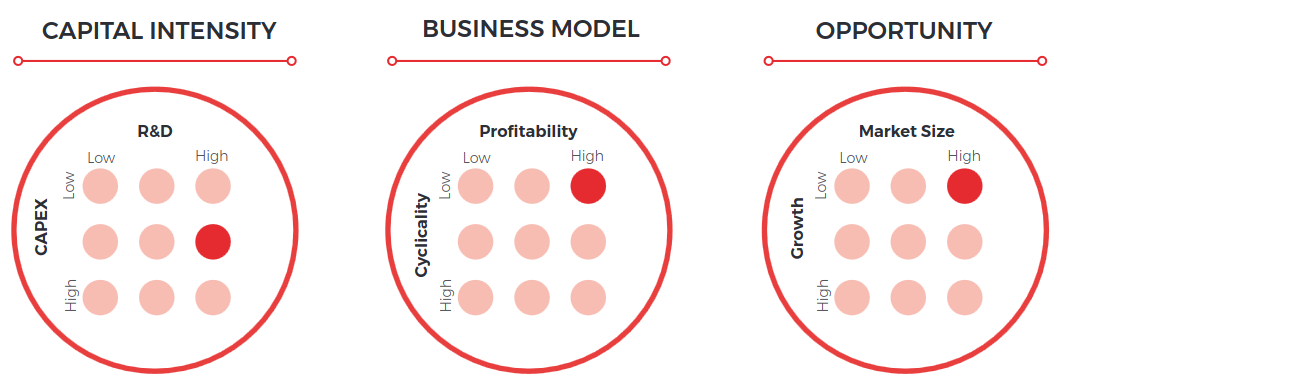

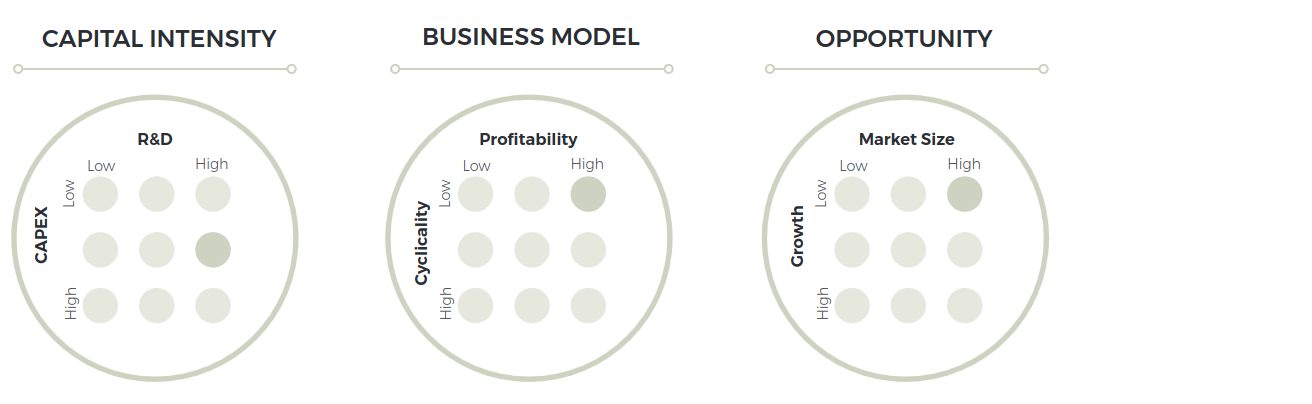

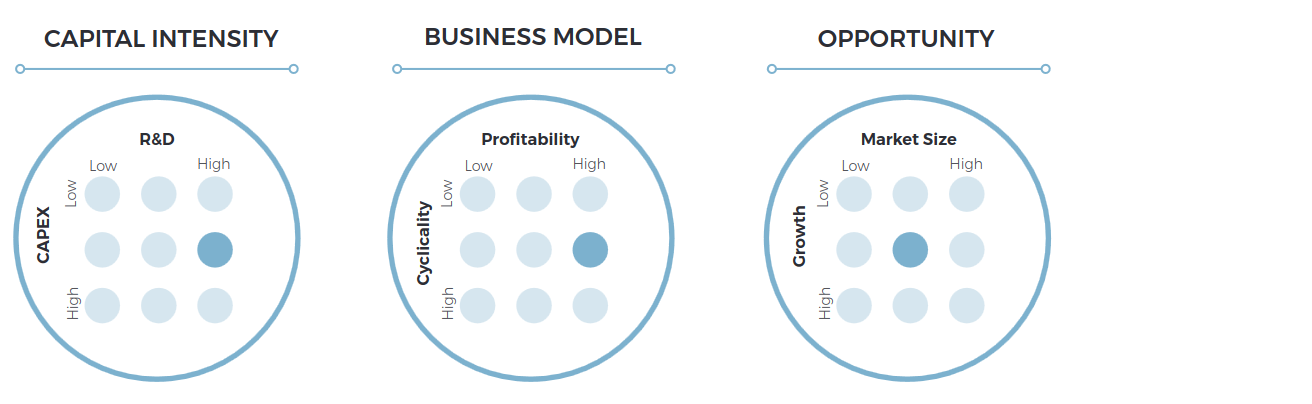

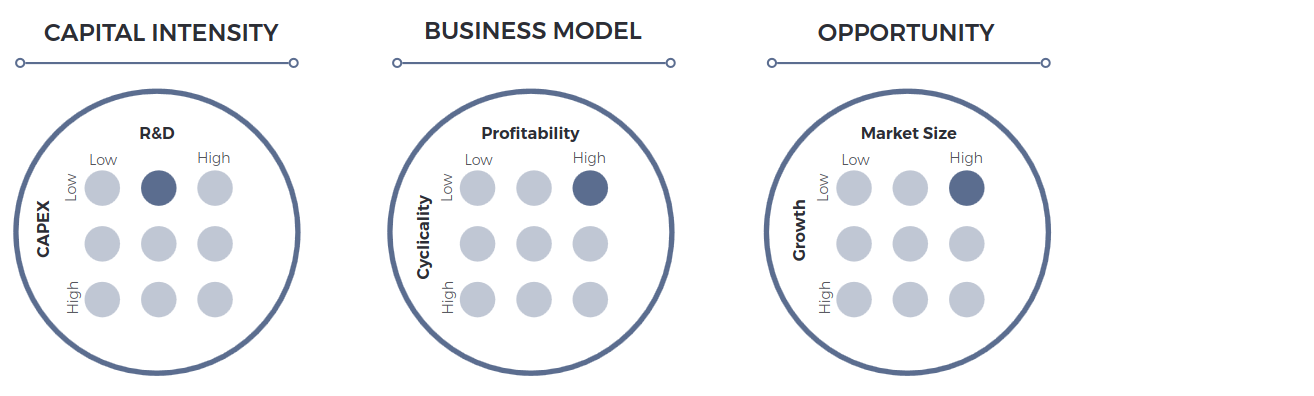

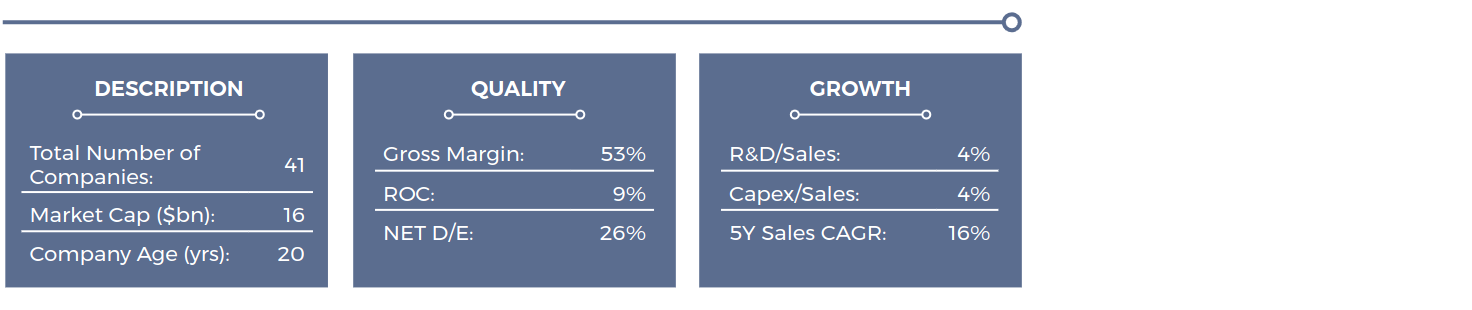

While the healthcare space requires laboratories to create medicines and vaccines, the overall requirement for fixed assets is low. The R&D requirement, however, is notoriously high for pharmaceuticals (Roche spent 21% of revenue on R&D in 2019); there are substantial research and regulatory hurdles to gain approvals and application processes can last several years. Although the MedTech space requires relatively lower amounts of R&D, we maintain a high rating for Advanced HealthCare’s R&D intensity.

Healthcare tends to be classified as a ‘defensive’ sector, showing relatively predictable earnings through varying periods due to the continuous demand for medical products and procedures. Although drug pricing pressures have brought some uncertainty to the pharmaceutical space, the MedTech space offers more stable recurring demand, leading to an overall low cyclicality rating. Despite the substantial upfront costs involved in bringing a drug to market, new innovative drugs can be highly profitable due to their patent exclusivity period (particularly in cutting edge biotech and genomics) driving our high profitability rating.

The growth potential for new innovative drugs (synthetic or biologic) and genetic editing is strong, meeting previously unmet medical needs and being an exclusive seller. Conversely, MedTech businesses offer more stable earnings as hospitals and practitioners slowly adopt these new technologies. Advanced healthcare is continually evolving with new discoveries and technologies emerging all the time. The advancements give way to ample runway, not least in Developed markets, but also in Emerging markets, driving our large market size rating.

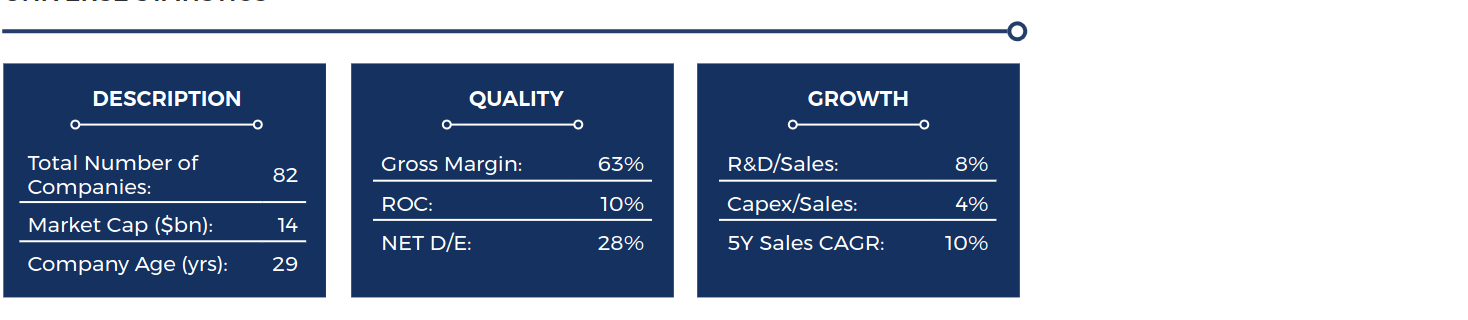

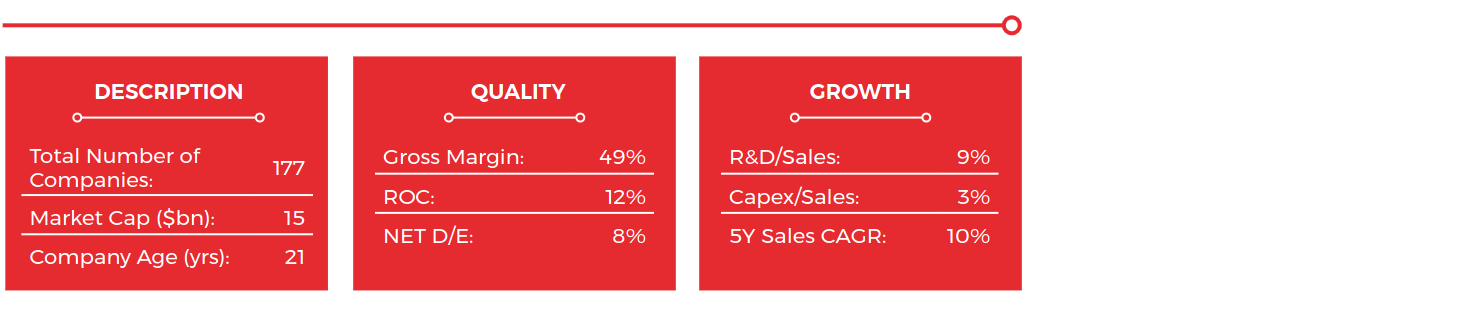

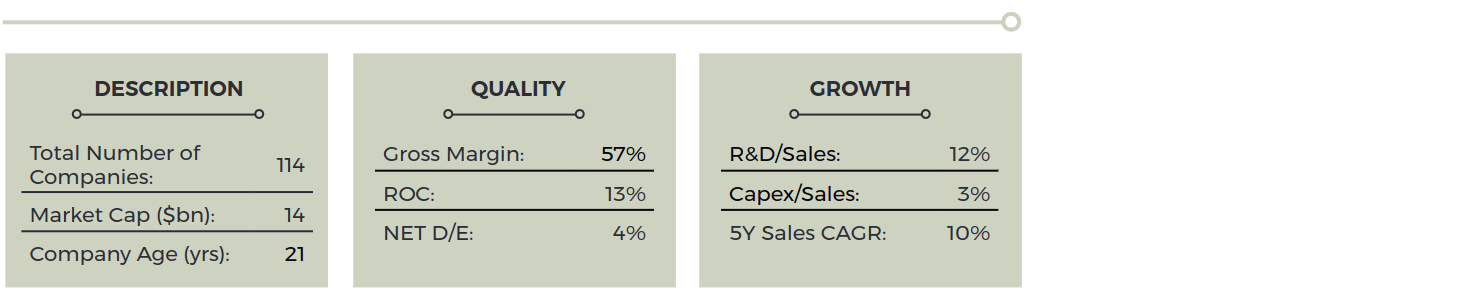

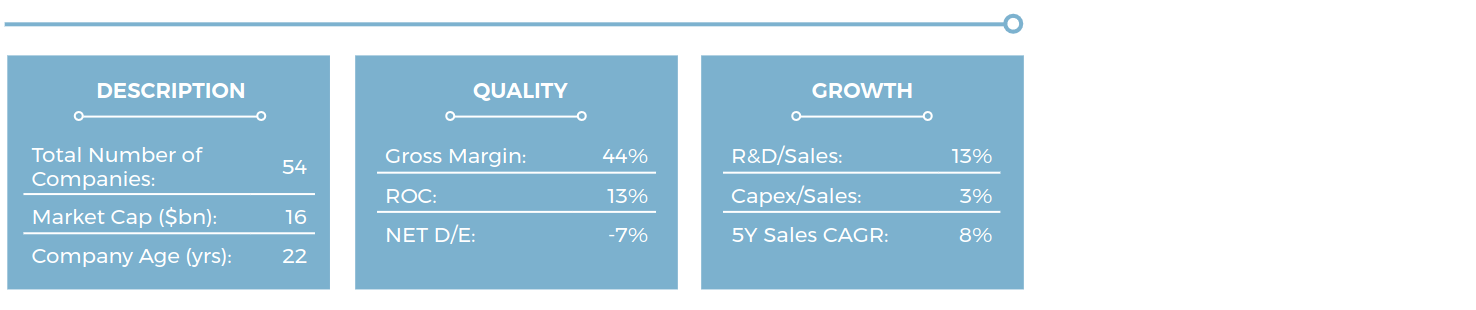

UNIVERSE STATISTICS

OPPORTUNITY SET

Traditional pharmaceutical companies, including incumbents Johnson & Johnson, Novartis, and Roche, benefit from large amounts of intellectual property (IP) and brand awareness creating wide economic moats. However, patent protection may only last as long as five years, creating looming patent cliffs after which competitors may produce their own cut-price versions. An alternative opportunity set comes from biotechnology companies. Unlike pharmaceutical medicine, which is manufactured from artificial sources, biopharmaceutical medicine uses living organisms to create solutions, and, although the investment costs are much higher, patents on approved biologic drugs can be as long as 12 years. This area is much sought after due to the higher growth potential and possibility of more sophisticated solutions, which has led to a variety of traditional pharmaceutical companies investing in this area: two of the largest acquisitions in 2019 were Bristol-Myers Squibb’s acquisition of Celgene and Danaher’s acquisition of General Electric’s biopharmaceutical business.

At the cutting edge of biotechnology, genomics offers opportunities in a less mature but higher-growth area of healthcare. While a large number of medicines do not address underlying causes, but instead serve to manage symptoms, genome sequencing has the potential to address this with a ‘one- time cure’. Although applications are currently limited to rare and incurable diseases, as the cost to sequence a genome continues to fall and gene therapy becomes more sophisticated, the applications will eventually expand and have the potential to be considered a ‘norm’ in modern healthcare. This area is currently led by Illumina, who predict they can reduce the genome sequencing cost down to $100 in the years to come.

While drug pricing pressures endure within the pharmaceuticals space, MedTech companies can offer some reprieve. These are the companies creating the technology that hospitals and practitioners use for applications including monitoring, diagnosis, and drug delivery systems. As a more tech- savvy generation comes through, patients are demanding quicker, cheaper, and simpler solutions. Companies such as Medtronic are creating more effective patient monitoring systems through the use of sensors; Intuitive Surgical performs robot-assisted surgery using its Da-Vinci robot; and Microsoft is partnering with healthcare companies to use AI for diagnosis, rehabilitation and better predictive analysis. The line between the healthcare and IT sector is becoming increasingly blurred; Apple continues to innovate in wearable devices such as its smart watches that can measure heart rates and perform ECGs. All this makes for an expanding opportunity set, with new players arising from unlikely sources.

ARTIFICIAL INTELLIGENCE & BIG DATA

ARTIFICIAL INTELLIGENCE & BIG DATA

Sub Themes: Machine Learning, Analytics, Autonomous Vehicles

As we move from an era of pre-defined logic – humans telling computers how to behave – to an era of computers learning how to act independently of humans, Artificial Intelligence (AI) is set to be revolutionary. Here, a machine and computer program seek to simulate human intelligence with the capability of altering its behaviour in response to input data. It will be able to learn, reason, discover meaning, perceive its environment, learn from experience, and interact. Furthermore, AI is set to take many forms – from voice and image recognition software, to language processors, smart robotics, chat bots and autonomous vehicles.

Whilst the idea of artificial intelligence is not new, the development of the technology has only truly become prominent in the last decade. IBM kick-started the advance in AI when its natural language software ‘Watson’ competed on the quiz show Jeopardy and won the $1mn jackpot. Recent improvements in AI technology have been driven by three factors: advances in computing power, particularly from semiconductors such as graphic processing units (GPUs); the explosion in data from increasingly connected devices used to ‘train’ algorithms (according to IBM, 90% of all data was created in the last two years [2017]); and cloud computing enabling the storage, aggregation and processing of data quicker and cheaper. The development of these adjacent technologies is enabling AI technology to become more effective at creating tangible economic benefits.

Businesses that are able to leverage this technology stand a better chance of developing sustainable competitive advantages. Here businesses can create more personalised consumer engagements that drive sales, improve productivity by utilising AI to gather new insights into predictive maintenance, quality control and task automation, and differentiate products by embedding AI capabilities. Indeed, these technologies are already being used all around us: Google and Netflix create personalised engagements through the use of AI to rank search queries and recommend new shows to watch (Netflix estimates 80% of content watched is a consequence of their recommendations, saving $1bn a year in customer retention), whilst other businesses are embedding personal assistants such as Amazon’s Alexa to differentiate their products from competitors and create smart devices. Whilst pure-play AI investment opportunities tend to be early stage and small in number, we find good opportunities arising from large IT companies such as Microsoft and their development projects, as well as companies embracing the technology in their current business models.

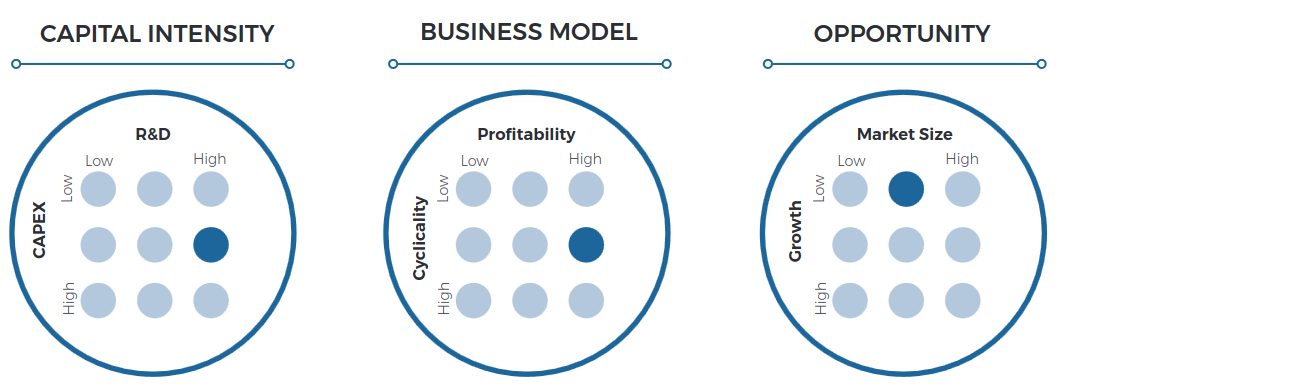

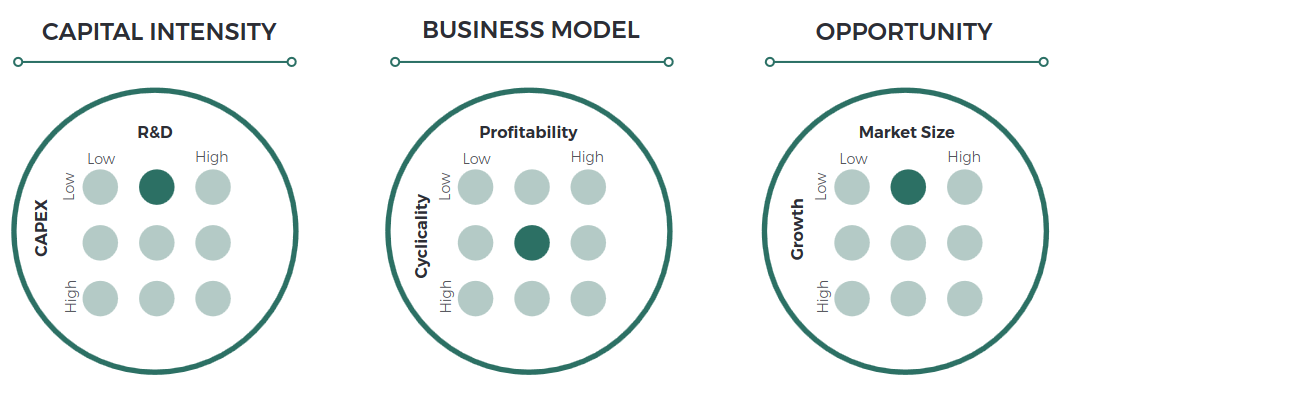

While the capex required to aggregate and compute data within data centres can be very large (Amazon Web Services [AWS] spent 37% of sales on capex in 2019), as well as more obvious capex needed in the manufacturing of autonomous vehicles – a specific use case of AI – the beneficiaries – those integrating AI into their products – tend to have more asset-light models. R&D, additionally, is a vital part of continuing to develop this relatively new technology and as such requires a high capital input.

Very few companies have the capability to develop cutting- edge AI technologies, usually confined to the largest players. Moreover, embedding AI capabilities, be it through enhanced analytics or voice assistants, can create a more premium product. For these reasons, companies exposed to AI tend to exhibit greater profitability. From a cyclicality perspective, although the application of autonomous vehicles tends to be more cyclical due to the general automotive market, AI capabilities reach far beyond this with the technology being embedded across industries – often in highly critical workflows. This leads us to a low cyclicality rating.

The applications for AI technology are not confined to any one industry, with vast potential to disrupt many kinds of business; from those involved in medical diagnosis, to autonomous vehicles and robotics. While the technology is still evolving, businesses developing the technology, as well as those utilising it, are experiencing high short-term growth (albeit from relatively low bases) and this looks to continue into the long-term (according to Tractica, annual global AI software revenue is forecast to grow from $10.1 billion in 2018 to $126.0 billion by 2025).

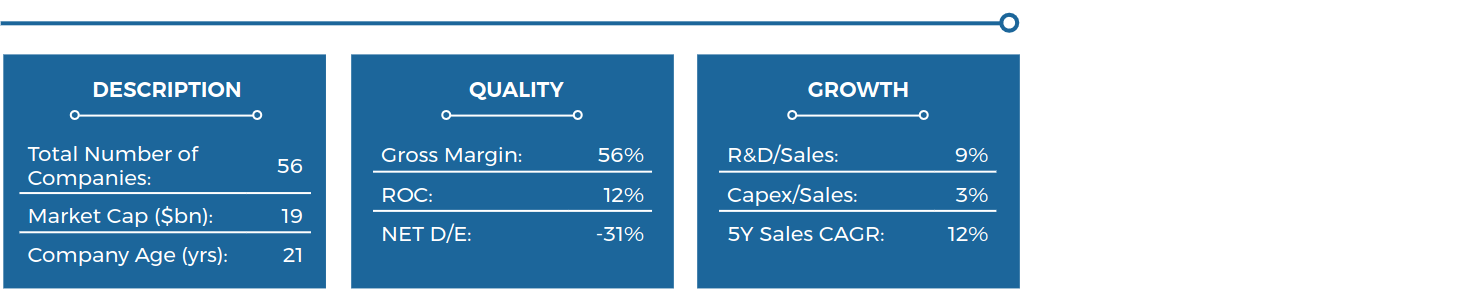

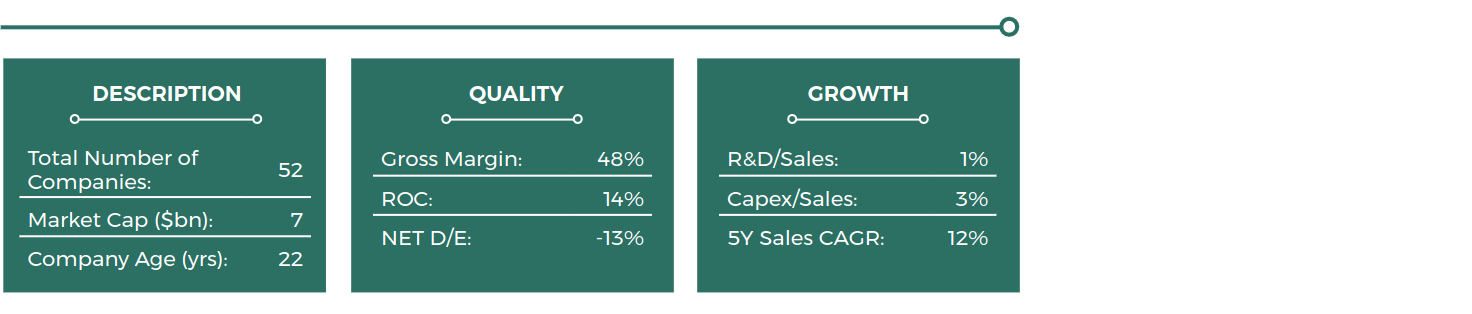

UNIVERSE STATISTICS

OPPORTUNITY SET

At the forefront of the AI revolution are the cutting-edge technology developers. This set of companies mainly consists of the large IT vendors such as Alphabet, Facebook and Microsoft, which have leveraged their expansive data sets and deep pockets to build out their own software and platforms which other businesses may now utilise. However, in order to develop these technologies, they have relied on developments in adjacent technologies, including semiconductors such as GPUs from Nvidia and AMD which are able to compute vast quantities of data simultaneously, better enabling AI algorithms to train and infer (in 2012, Google Brain used over 10 million images from YouTube video thumbnails to train its AI to identify a cat) and cloud computing businesses such as Amazon Web Services which provide the computational power to process this information.

Taking advantage of the new technologies are the beneficiaries. These are businesses that are integrating AI into their existing products and services to create more meaningful insights and engagements. Smart device manufacturers, for example, are integrating speech recognition software such as Amazon’s Alexa into their products. Additionally, software vendors including Adobe and Salesforce are leveraging AI on their data sets to create more intelligent tools to analyse current marketing strategies or to prioritise sales leads based on historic deals and likelihood of closure. This should create more sustainable competitive advantages over competitors, creating higher switching costs through enhanced capabilities.

In an application-specific use of AI, we find good opportunities in the autonomous vehicle (AV) space. Here, there are numerous companies ranging from the large IT software developers such as Alphabet with their Waymo project, to the developers of advanced driver-assistance systems (ADAS) such as Mobileye (owned by Intel) and Infineon, who produce power management semiconductor chips. While we remain a few years away from seeing the widespread use of AVs on the road – with the safety precautions requiring further scrutiny – we are very much on the path to fully autonomous vehicles with automated breaking, automated parking, lane departure warning and cruise control already integrated into most new vehicles.

CLEAN ENERGY & SUSTAINABILITY

CLEAN ENERGY & SUSTAINABILITY

Sub Themes: Electric Vehicles, Circular Economy, Resource Efficiency

As humans have evolved, technologies have advanced, and consumers have demanded better, faster, and more efficient products and services. And while we would not be where we are today without such periods as the industrial revolution – which enabled humans to transition from manual manufacturing to the industrial mass production of goods, often turning to fossil fuels to power the new machinery – the impact we have had on our world is becoming increasingly apparent. The emphasis today is on sustainability: that is, considering environmental impacts before undertaking projects, utilising clean energy sources, and becoming more efficient in the way that we use and subsequently dispose of products.

The push for sustainability is no longer only coming from small clusters of activists, but from governments and companies alike. The Sustainable Development Goals (SDGs), for example, signed by all 150 UN states, define 17 global goals to tackle by 2030 – an initiative many businesses and investment strategies are now aligning themselves with. The clean energy transition is a specific area upon which governments have been focusing: the pursuit of GDP growth, rising populations, and increasing emissions have led to rising temperatures and public concern over climate change. Governments are now responding in a concerted global effort to tackle emissions through numerous green initiatives aimed at making renewable energy sources more competitive against fossil fuels.

The pressure from governments, investors, and consumers is leading to a renewed focus on corporate sustainability: companies are being urged to source raw materials responsibly and pivot towards circular business models, to reduce their carbon footprints, and ultimately to produce products that are beneficial to the world, not detrimental. Businesses which champion sustainable business practices are set to enjoy first-mover advantages in new product categories, improved brand image, and higher consumer switching costs. Combining this with greater efficiency and lower input costs could ultimately lead to a material improvement in their bottom line, enabling these new age enterprises to be “doing well whilst doing good”. Laggards, on the other hand, could face government fines, shareholder revolts, and even consumer avoidance or boycotting. From the standpoint of a long-term investor, these opportunities may not be best placed for sustained growth.

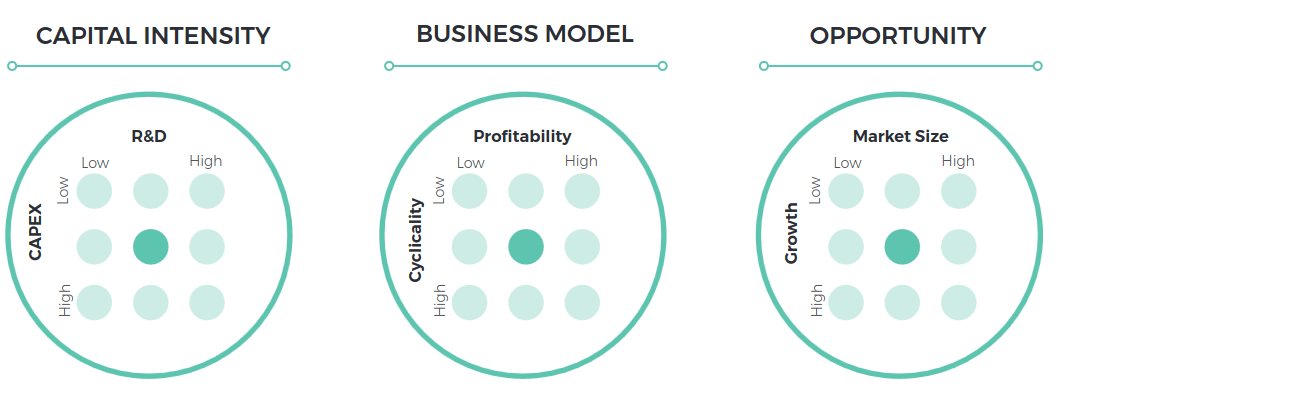

While the capex requirement to improve the efficiency of an existing workflow does not require substantial new equipment, the capex intensity in the production of electric vehicles (EVs) and renewable energy projects (large wind farms, for example) is comparatively large. Additionally, incremental R&D investments are further necessary to continue innovating in areas such as power efficiency and material science.

Although incorporating sustainability into a company can have upfront costs, a business may be more efficient going forward and benefit from improved competitive advantages arising from enhanced brand image and higher consumer switching costs. Additionally, clean energy, which has historically been dependent on subsidies, is now becoming competitively priced vs fossil fuels, leading to growing margins and more stable earnings. This leads to our medium cyclicality and profitability ratings.

Growth in these areas has historically been gradual and of a stop-start nature dependent on subsidies. However, alternative energy is now becoming profitable on a standalone basis vs traditional generation technology while the quality of earnings is also set to improve as installed bases build and related service revenue grows. Furthermore, green stimulus packages, cross-border agreements between countries, and increasing stakeholder pressure are enabling more sustainability- themed innovation to take precedent.

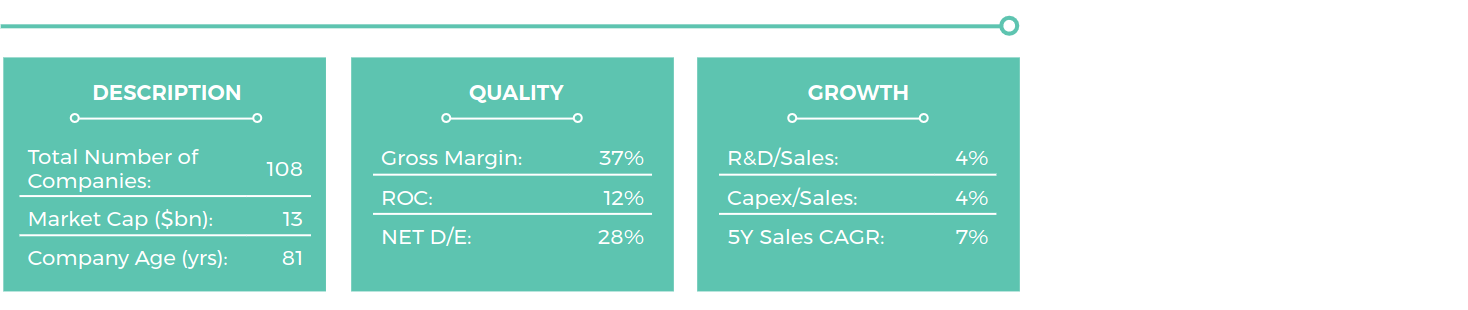

UNIVERSE STATISTICS

OPPORTUNITY SET

As the world transitions away from traditional fossil fuels, new investment opportunities are arising in the renewable energy space, through companies which harness the energy produced by solar (e.g. Canadian Solar and First Solar), wind (e.g. Vestas) and geothermal (e.g. Ormat) power sources. Historically, subsidies have played a crucial role in supporting the transition away from traditional carbon-based fuels. However, as these businesses have scaled, together with regional taxes on carbon, the cost to produce renewable energy has become increasingly competitive vs fossil fuels. Indeed, BP predict that by 2040, renewables will surpass coal as the primary source of global power, accounting for 30% of the sector.

With transportation contributing 24% of direct CO2 emissions from fuel combustion (International Energy Agency), the transition to clean energy has led to a drive towards electric vehicles (EVs). While Tesla may be the posterchild for EVs – and arguably rightly so due to its leadership in batteries – the transition is also creating opportunities elsewhere. Traditional car manufacturers are themselves transitioning to more electrified products, while EV-enabling manufacturers are exhibiting evolving demand. These include Aptiv, who are responsible for the electrified ‘nervous system’ of a vehicle, Infineon, who produce power management semiconductors, and ABB, who manufacture electric vehicle charging infrastructure. While new vehicle releases are currently geared more towards hybrids, the full electrification of vehicles may lie in the not-so-distant future, with governments pushing for ambitious goals: China, for example, reportedly has plans for 60% of all automobiles sold to run on electric motors by 2035.

With companies and shareholders alike pushing for sustainable product sourcing and waste reduction, management are gearing business models towards resource efficiency and circular economies. That is, maximising the supply of resources whilst minimising waste and using sustainable materials that can be reused, repaired, or recycled. Businesses such as Schneider Electric and Siemens create solutions to more efficiently manage power usage, Smurfit Kappa is a global leader in sustainable paper-based packaging, while retail businesses such as Nike are using recycled materials in their newest footwear and apparel (FY19 Nike Impact Report: 76% of Nike footwear and apparel include some recycled materials). While direct exposure to this sub-theme is limited, businesses employing this type of thinking point to more effective long-term capital allocators within management.

CLOUD COMPUTING

CLOUD COMPUTING

Sub Themes: Cyber Security, Networking, Software-as-a-Service

Cloud computing can be defined as the delivery of computing services – such as servers, storage, databases, networking, software, and analytics – over the internet (“the cloud”). The service, provided by cloud vendors including Amazon Web Services (AWS) and Microsoft Azure, gives companies access to faster, more flexible resources and economies of scale. Typically, companies such as SAP or Dropbox, which deliver their products to consumers using the cloud, pay cloud vendors including AWS only for the cloud resources they use – not dissimilar to your electricity bill. This helps to create lower fixed costs by eliminating expenditure incurred in setting up their own on-site data centres, while giving them the flexibility to increase usage as they scale. Cloud computing is enabling businesses across industries to deliver their products and services on-demand: from file storage and backups to video gaming, data analytics, and video conferencing.

As the use of the cloud has expanded, we have seen the increasing use of Subscriptions-as-a-Service (SaaS) business models. These new models charge consumers periodic fees for the right to use their product or service, as opposed to one (much larger) license payment. This enables companies to deliver automatic updates or the latest content as soon as they’re available, while receiving smoother payments throughout the year with higher retention rates (you’re more likely to keep paying your $8+ a month Netflix fee as opposed to repeating a larger one-off fee to get hold of the latest content). Adobe, for instance, has been transitioning consumers from perpetual licences to subscriptions for its various software packages, and has consequently seen recurring revenue grow to 89% of revenues in 2019, whilst operating margins have expanded from 18.4% in 2015 to 29.2% in 2019.

As consumers increasingly demand greater user experiences and as firms increasingly see the benefit in transferring their products and services to the cloud, the opportunity for long- term growth across the value-chain is set to be immense. The growth in data volume will require greater quantities of more sophisticated networking hardware and software in data centres to manage the flow of data, whilst the increasing propensity to store data in the cloud will increase the need for more robust cyber security systems. This gives rise to numerous investment opportunities across the cloud computing value chain, from your upstream data centre providers to end market SaaS business models.

There is a large capex requirement to build vast data centres capable of aggregating and computing enormous quantities of data (AWS spent $13bn on cloud capex in 2019 alone). However, the beneficiaries tend to have more asset- light models with no need to build on-site data centres. R&D, however, is key to continue developing this technology: from optimisation of data flow, to reducing the vast energy consumption and cooling systems required to operate the centres (Microsoft’s project Natick is testing the feasibility of subsea data centres powered by offshore renewable energy).

With few players able to afford the large upfront costs involved in designing and building vast data centres, the market is currently dominated by several vendors which are able to enjoy healthy margins (AWS operating margin 26% 2019 vs MSCI World 12%). Further, SaaS businesses are able to lower their long- term operating costs by utilising the cloud, thereby expanding their margins. Cloud computing poses vast opportunities across industries: not only is it being harnessed by the big players in gaming and video streaming, but also in mission- critical applications that enable data access and remote working, which ultimately enable a business to continue operating. This leads us to our low cyclicality rating.

As the world continues to produce ever increasing volumes of data, the need for greater aggregation, storage and computational power grows. Additionally, as a growing number of businesses move to cloud-based products and services, the need for this technology becomes vital across applications – from streaming content to a business’s operational software. Indeed, AWS has grown revenues at 35% CAGR over the last 5 years. These reasons point to a considerable market size together with significant growth rates.

UNIVERSE STATISTICS

OPPORTUNITY SET

The firms set to yield the greatest rewards are the cloud vendors. These are the companies with the substantial financial ability required to build new data centres capable of delivering content on-demand on a mass scale. The market is currently comprised of a handful of players including AWS, Microsoft Azure, Alibaba Cloud, and Google Cloud Platform (with AWS and Azure being the dominant players). These companies generate large economic moats as they benefit from economies of scale realised from providing cloud computing to an increasing number of businesses, while large upfront costs disincentivise any potential new entrants.

Another set of companies highly exposed to growth in cloud computing is a group that can be collectively described as the enablers. In order to set up and manage the vast quantities of data in the cloud, the cloud vendors must use highly sophisticated equipment: networking companies such as Cisco and Arista produce switches and routers along with optimisation software to manage the fl ow of data, while semiconductor companies design the ‘brains’ of the data centres – from central processing units (CPU) sold by Intel, to the more advanced so-called accelerator chips including field programmable gate arrays (FPGA) and graphic processing units (GPU) produced by Xilinx and Nvidia respectively.

Firms willing to transfer their products and services to the cloud-based equivalents can benefit from a more asset-light business model, higher recurring revenues, and subsequent opportunity for margin expansion. These beneficiaries are diverse and span varying industries, from Netflix (delivering your videos on-demand) to SAP (customer relationship management software) and Adobe (cloud-based creative software). Additionally, with the increased use of the cloud to store and transfer data, this is driving demand for more sophisticated cyber security software. With data privacy ever more at the forefront of consumers’ minds as a result of firms increasingly being targeted by cyber-attacks – the attack on Sony Pictures in 2014 being particularly memorable – firms such as Cisco and Fortinet are benefitting from the growing need for businesses to protect their consumers’ data.

INTERNET, MEDIA & ENTERTAINMENT

INTERNET, MEDIA & ENTERTAINMENT

Sub Themes: Social Media, Streaming, Gaming, eLearning

Ever since the World Wide Web was invented in 1989 by English scientist Tim Berners-Lee, the internet has been one of the main drivers behind many of the world’s advances, creating an ecosystem upon which information may be shared and people may connect. Recent advances in network connectivity, particularly in cloud computing, coupled with the desire of consumers to engage and connect with one another at ease, has led to an explosion of mediums through which you can now stream, share and surround yourself with like- minded people.

Social media platforms have allowed people to build networks and engage with millions of followers with just one tweet: according to Hootsuite’s Global Digital April 2020 report, there are 3.8bn active social media users, compared to a world population of 7.8bn – a 49% penetration rate. Platforms such as Facebook have allowed consumers to build their own online profiles based on likes and dislikes, which has enabled businesses to create more targeted engagement, leading to better conversions. By creating ecosystems around consumers’ profiles, these platforms have been able to monetise additional features: Tencent’s WeChat, for instance, is the leading example of a so-called ‘super-app’, with the platform’s 1.2bn monthly active users (MAU) being able to order food, pay utility bills, order a taxi and more – all directly through the app.

Indeed, advances in cloud computing, coupled with businesses’ need to connect to wider audiences and consumers’ desire for convenience, has led to an era of digital-first products and services. Netflix’s success comes from taking a stagnating DVD rental industry and pivoting it into a digitalised distribution platform, enabling consumers to stream content on- demand over the internet. This has led to an era of cord-cutting, with viewers preferring to cancel their multichannel television packages in favour of streaming content online, usually for less money and more convenience. Similar evolutions can be observed across other industries: educational services are making greater use of the internet to deliver classes, requiring fewer classrooms whilst giving access to wider audiences who may otherwise be unable to attend; within video gaming, consumers have shifted from physical purchases to online downloads, and now – led by Alphabet’s Stadia – to the early stages of cloud-based video game streaming. Moreover, gaming has seen further innovations to enhance user experiences through improved graphics via Nvidia’s graphic processing units (GPU), the advent of eSports and augmented & virtual reality experiences.

While the capex requirements for media streaming businesses and gaming producers are low, social media companies are required to spend larger amounts on data centres in order to manage vast quantities of data (capex/sales 2019: Netflix 1%, Activision 2%, Facebook 21%). This combination leads us to a medium capex rating. Moreover, R&D expenditure amongst social media, streaming and gaming companies is large as user experiences need to be continually improved through personalisation algorithms, streaming optimisation, and sophisticated graphics.

For streaming platforms such as Netflix, scale is everything. To achieve this, these businesses are having to spend substantial capital on content, which is leaving slim margins. However, offsetting these costs are healthy margins from social media and gaming businesses (operating margins 2019: Facebook 34%, Activision 25%) – hence our overall high profitability rating. In terms of cyclicality, the revenues derived from this theme tend to be fairly discretionary in nature, although streaming has gone some way to offset this with subscription business models aimed at recurring revenues.

Advances in cloud computing and connectivity are driving substantial growth rates in social media and streaming platforms, with further runways led by underpenetrated markets and the movement towards cord cutting (5Y sales CAGR 2019: Facebook 41%, Netflix 30%). Video gaming tends to be more modest in growth, with releases that are difficult to forecast and with lower switching costs amongst publishers. eSports, however, is placing video games in the mainstream, with an estimated 495mn viewers in 2020 (Newzoo).

UNIVERSE STATISTICS

OPPORTUNITY SET

While social media platforms – such as Google + and MSN – have come and gone, the overall number of platforms has grown in number, with varying types of content and use cases: from social networks and messaging platforms such as Facebook, WeChat and Twitter, to media sharing platforms like YouTube and Instagram, as well as more niche discussion forums and content curation networks. These platforms are able to leverage their network effects to create ecosystems upon which to monetise. While Facebook boasts the leading portfolio of platforms with Facebook, WhatsApp, Facebook Messenger, and Instagram – which currently experience 2.5bn, 2bn, 1.3bn and 1bn global MAU respectively – more comprehensive ‘super-apps’ have emerged primarily in Asia. Tencent’s WeChat, the most all- encompassing example, has 1.2bn MAU, each able to leverage multiple services from within the app, improving user experiences and creating additional revenue streams for the platform.

As cloud computing has advanced, the ability to stream your music, TV, video games or educational courses (eLearning) through any one of the numerous devices consumers now have at their disposal has been realised. These streaming companies, such as Spotify for Music, Netflix for video content, or Stadia for video games, are able to deliver their respective products and services via the internet – typically for a monthly subscription, leading to highly recurring revenues at lower costs. A trend we have seen in the last few years is the disaggregation of content: while Netflix was first to market the go-to service for all your video needs, content creators such as Disney (Disney+, ESPN+, Hulu) and Comcast (Peacock, NowTV) are now building out rival streaming services, taking back control of their own content in the hope of generating highly sought- after recurring revenues. This has created new investment opportunities from what were once pure-play cable TV providers.

While streaming video games over the internet offloads the actual running of the game onto data centre servers and enables playing time across devices, it is not the only innovation taking place within gaming: more advanced technologies are opening the world of gaming to new players and creating new immersive experiences through virtual and augmented reality headsets (Facebook’s Oculus) and advanced graphics (Nvidia’s GPUs). No longer do individuals purely enjoy gaming within the four walls of their bedrooms: the advent of eSports creates organised video game competitions played in front of live audiences and streamed to millions worldwide. Not only is this creating new demand for game creators such as Activision and Tencent, but also for streaming services such as Alphabet’s YouTube and Amazon’s Twitch, on whose platforms millions can watch. The League of Legends World eSports Championship in 2019, for example, boasted 100mn viewers – the same number of viewers as the American Football Super Bowl drew in that same year.

MOBILE TECHNOLOGY & INTERNET OF THINGS

MOBILE TECHNOLOGY & INTERNET OF THINGS

Sub Themes: Smartphones, Wearables, Smart Devices, 5G

As the world has evolved, so too have our mobile phones. You only have to go back to the 1970s when Motorola launched the first mass-produced – albeit rather unwieldy – handheld device, which did the job of providing two-way communication. Since then, mobile phones have evolved in leaps and bounds, with mobile computing serving as a more accurate term to describe the vastly improved functionality. Indeed, while the size of mobile phones has shrunk considerably, the applications they house have expanded and merged what used to be distinct operations into one all-encompassing device: from messaging and internet access, to music and TV streaming, photography, and maps. The rise of the mobile phone has led to the expansion of other mobile devices from tablets to laptops, although the differentiation between these devices is becoming less apparent as their size and functionalities converge.

As sensors and mobile technology have advanced – and with the next generation of consumer demanding increasingly cloud-based applications – the evolution of ‘smart devices’ has come to fruition. What was once a fridge is no longer ‘just’ a fridge, but now a smart fridge; what was once a watch is no longer ‘just’ a watch, but now a smart watch – all connected, all talking to each other. These new ecosystems of devices and sensors – now collectively referred to as the Internet of Things (IoT) – give users the ability to track, monitor and control devices remotely, creating high switching costs for consumers considering alternative brands. The technology responsible for facilitating such transformation in mobile technology and connected devices? Wireless networking. While 4G has led the most recent wave of evolution, 5G is poised to be a huge leap forward, offering speeds significantly faster than the current 4G technology and vastly better coverage which will enable newer technologies that simply were not possible on older iterations. Autonomous vehicles, for example, will require constant connectivity and low latencies in order to manage the continuous flow of data from sensors and be able to react accordingly.

While the proliferation of smart devices and mobile technology raises concerns over privacy and security as the volume of data capture increases exponentially, these technologies are set to disrupt and transform all industries: from healthcare – with the ability to remotely track vitals and instantly connect to practitioners – to ecommerce – with the ability to search, shop and buy items on any mobile device. The ability for businesses to capture more data should better enable them to gain more holistic insights into consumer behaviours and thereby deliver more personalised experiences, translating into better conversions.

The capex requirement for mobile technology and IoT devices is moderate, with lots of enablers creating differing components. However, the utility businesses enabling 5G connectivity require much more. This, however, is offset by more modest requirements from 5G enablers such as Cisco and Keysight (Verizon spent 14% of sales on capex in 2019 vs Cisco 2% and Keysight 3%). The R&D requirement, nevertheless, remains high across these technologies, particularly from semiconductor manufacturers (Xilinx 24% R&D/Sales in 2019 & Broadcom 21%).

Although mobile technology can be thought of as discretionary products, 5G provides a more stable cycle, with countries continuing their spend in a push to lead this new technology. In terms of profitability, mobile technology has tended towards more premium products with more sophisticated functionality (Apple operating margin 25% 2019). Similarly, the semiconductor and networking businesses exposed to 5G are able to yield expansive margins by way of their increasingly complex products (Xilinx operating margin 31% and Cisco 27%).

The market opportunity for 5G applications is significant with new technologies relying on its fruition (autonomous vehicles, IoT and better internet access globally to name a few). Mobile technology, however, is more evolutionary than revolutionary, with updates on the latest versions arriving regularly. Nonetheless, increasingly connected smart devices should provide ample growth opportunity across applications.

UNIVERSE STATISTICS

OPPORTUNITY SET

While Motorola and Nokia may have initiated the mobile phone revolution some 40 years ago, the largest manufacturers of smartphones today include Apple, Samsung, and a handful of Chinese manufactures. These companies are continually pushing the boundaries of what it means to be a smartphone, with better cameras, foldable screens, and facial recognition. However, the manufacturing of a smartphone consists of much more than just the branding. While the iPhone may have been designed by Apple, the majority of its components come from adjacent players: from AAC Technologies – who provide the acoustics and haptics – to Broadcom – who supply the modem chips – to Foxconn – who bring everything together to create a finished product. These enablers are typically exposed to high levels of customer concentration risk but can provide an alternative exposure to the mobile technology evolution.

Although the smart device opportunity set is more in its infancy, it does provide a glimpse into the future of tech, as it becomes more compact and integrated into traditional objects. For example, Acuity Brands, the largest luminaires company in North America, is using its lights as a base for new technology, integrating sensors capable of measuring CO2 levels, to tracking the movement of customers within a shop. The majority of investment opportunities, however, come from larger businesses which are building out their portfolio of smart devices either through acquisition or internal transformation of their existing products. For instance, Amazon acquired Ring – a smart doorbell – and Google bought Nest – a smart thermostat – to expand their ecosystems of devices, all connected to their respective smart speakers, Echo and Google Home. In the wearable segment, Apple leads the way with its smart watch – a product which goes beyond fitness tracking to provide mobile computing on your wrist. However, this segment remains a relatively small portion of their overall business today.

As the 5G revolution begins, nations are championing their own national businesses in a bid to be the leader in the next wave of connectivity. While traditional telecoms are the obvious group set to benefit with the likes of Nokia and Ericsson building out their 5G networks in the US, our opportunity set focuses on the more asset-light enablers. With the increased demand for physical telecoms comes the increased need for components from providers of switches such as Cisco, semiconductor producers such as Xilinx, and design, testing, and measurement solutions from Keysight. These 5G enablers provide a different pool of investment opportunities in which to gain exposure.

NEXT GEN CONSUMER

NEXT GEN CONSUMER

Sub Themes: Ecommerce, Everything-as-a-Service, Healthy Living

With each new generation comes a new wave of opportunities and challenges for consumer-orientated companies. The so-called ‘Gen Z’ consumer – those born between 1996 and 2010 (although definitions differ) – were brought up as America’s first generation of true ‘digital- natives’, demanding simpler, cheaper, and more sustainable products at their fingertips. With Gen Z set to make up the largest proportion of the US consumer population, companies must adapt and innovate to offer on-trend products and services, and ultimately stay relevant.

The newest set of consumers is poised to be the most diverse, forward-thinking generation who care less about brand loyalty and more about convenience. Retail is one of the main areas where this changing consumer is bringing about the most disruption. Companies such as Inditex (Zara’s parent company) are investing in supply chains closer to stores and more automated manufacturing in order to deliver ‘fast fashion’ (i.e. shorter time intervals between design and sale) to keep up with changing trends. Not to mention the threat of ecommerce: consumers want to be able to search, review and purchase goods on whatever device they happen to be using, with easy checkouts and fast delivery. This is an area where the ecommerce giants Amazon and ASOS have thrived at the expense of the traditional brick-and- mortar retailers.

Technology is perhaps the biggest differentiating factor between generations. The next generation of consumer – born mobile phone in-hand – demands convenience and speed at their fingertips. This has led to the digitalisation of many products and services – ‘there’s an app for that’ – and a new wave of business models termed ‘Everything-as-a-Service’ (XaaS). These businesses do not sell the product itself but charge for usage – a flexible model penetrating industries from accommodation with Airbnb to ride- hailing with Uber.

Finally, while technology may be driving many of the inter-generational transformations, consumers are also becoming increasingly health- conscience. From consumers targeting more active lifestyles which has led to athleisure wear becoming everyday norms, to more sustainable and healthy diets giving way to more niche plant- based products.

The R&D expenditure required for these ‘digital-first’ companies is high, particularly within many XaaS businesses which are relatively young in their life cycle (Uber 34% R&D/ Sales in 2019), whereas the R&D required for healthy living products such as apparel or nutrition is relatively lower. The overall capex requirement for the theme, however, is low, owing to the high proportion of software- related products that this theme incorporates.

The structural changes from the previous generation underpin a relatively stable outlook for many of these businesses – i.e. the shift to healthy living and digital–first businesses. However, these products are often discretionary, leading us to a modest cyclicality rating. Moreover, healthy living and ecommerce businesses tend to command expansive margins through their premium products and personalised shopping experiences. Conversely, the high reinvestment costs for XaaS businesses often leads to much leaner margins.

Consumers’ demand for digital products is driving high growth rates amongst pure- play businesses, as well as those transforming their online presences (Nike now derives ~20% of revenues from digital sales). Additionally, the move towards sustainable products has seen a dramatic increase in meat-free alternatives and healthy foods, as well as athleisure apparel products (according to a 2019 Mintel report, sales of meat-free foods in the UK have grown 40% from £582 million in 2014 to an estimated £816 million in 2019).

UNIVERSE STATISTICS

OPPORTUNITY SET

The shift to ecommerce and away from traditional brick-and-mortar stores offers good opportunity for investment, not only from the online-only businesses such as Amazon and ASOS, which offer faster growth and asset-light models, but also from traditional retailers who are investing in their online presence. Take Nike, whose recent strategy has been digital-first, focusing more on direct- to-consumer sales through their online channels. The shift to digital should reduce these companies’ fixed costs (mainly rent) thereby reducing their operating leverage, whilst bringing about more personalised shopping experiences through their online portals.

In the Everything-as-a-Service opportunity set, we find a diverse range of businesses that are not confined to any one industry: from taxis with Uber and Lyft, to music streaming with Spotify. These businesses tend not to meet our quality universe criteria, being earlier in their lifecycle and burning through significant amounts of cash in order to reach critical mass and maintain their high growth profiles. However, they are worth monitoring as these companies transition from constant re-investing cash-burners to more stable cash-generative businesses. Moreover, traditional businesses are also transitioning their products into pay-per- use services: Dell offers a PC-as-a-Service model which enables businesses to pay a predictable per-seat subscription for end-to-end solutions from computing hardware and software to maintenance and data recovery; while Rolls Royce rents its jet engines through its TotalCare program, charging on a ‘per-flying hour’ basis, and uses data from the connected sensors to provide proactive maintenance.

With the next generation of consumers being increasingly health conscious, this has created new opportunities for companies who can offer healthy-living lifestyle products and services. Athleisure clothing brands such as Nike, Lululemon and Adidas are in demand, partly as populations become increasingly active, but also as consumers view the clothing as a fashionable alternative to everyday wear. Aside from having a more active lifestyle, consumers are also more food and drink conscious, which has paved the way for a spectrum of dietary styles – from vegetarianism to veganism, and everything in between. A subsequent shortage in supply of these types of products has left a void into which new innovative products are emerging, including plant-based alternatives such as Beyond Meat (although too early stage for our investible universe), as well as Danone with its portfolio of products from nutritional supplements to soy- based alternatives.

PAYMENTS & FINTECH

PAYMENTS & FINTECH

Sub Themes: Digital Wallets, Blockchain, Payment Infrastructure

As the twenty-first century rolls on, you may be forgiven for believing that cash is essentially obsolete in the modern world. In developed economies, businesses are increasingly offering a variety of payment methods – cash, card and contactless (via card, phone, watch, or even contactless rings). Yet when we look at a developed economy such as Europe, cash still represents 79% of all point of sale (POS) transaction volumes (World Payments Report 2019, Capgemini), with even higher proportions in emerging economies. Moreover, non- cash transactions pose their own unique set of challenges: inconsistent methods of invoicing in Business-to-Business (B2B) transactions, complex cross-border systems, fears over data privacy, and underwhelming user experiences all leave plenty of room for innovation in this space.

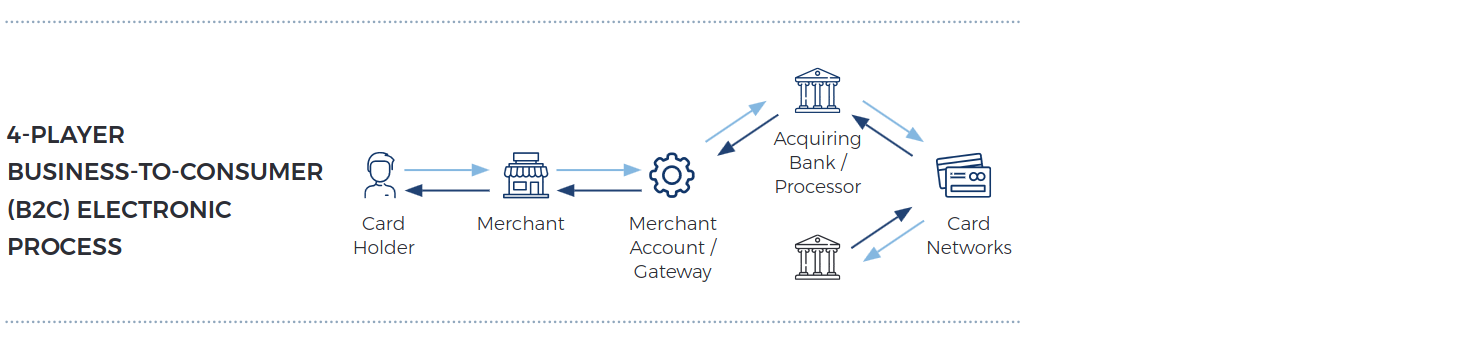

While the current payment space is filled with incumbents whose systems have been batched together over time, newer innovative players are making their way into the market, disintermediating the slow, expensive services that lack data insights. The 4-player business-to- consumer (B2C) electronic payment process, for instance, through which data traditionally travels each time a consumer makes an electronic purchase, relies on a payment gateway/POS system, issuer bank, merchant bank, and a card network – all usually different, all taking a fee. This causes issues for corporations who have to use differing providers across multiple channels and geographies, whilst posing the challenge of consolidating data into a single platform. This, however, is being tackled by Dutch payment company Adyen, who employ a single platform across geographies – one which covers more of the payment life cycle and offers improved analytics. Elsewhere, cryptocurrencies are showing promising applications within B2B and cross-border transactions, whilst digital wallets such as Apple Pay and PayPal are facilitating more secure payments alongside better user experiences.

Payments and FinTech is a broad space with appealing characteristics and growth driven by a number of structural changes: the move away from cash, which is increasing the pure volume of non-cash payments; the growth in e-commerce transactions, which is shifting payments away from stores and onto online portals; and the proliferation of mobile technology, which makes everything conveniently available at your fingertips. These businesses are highly scalable, with low incremental costs leading to highly persistent returns on capital. Furthermore, they tend to benefit from network effects – that is, the more consumers on the network, the more attractive the network becomes to additional consumers and merchants.

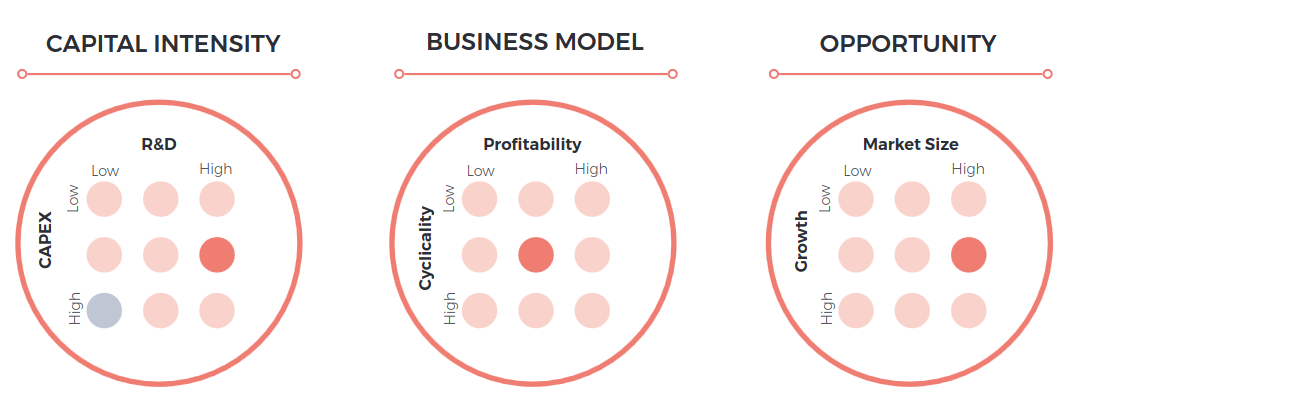

Payment companies, in general, tend to require very little incremental capital input to generate an extra $1 of revenue, owing to their asset-light business models. Although more established players such as Visa do not report any R&D expenditure, FinTech businesses including PayPal and Square spend large amounts on innovation (R&D/Sales 12% and 14% in 2019 respectively). This drives our medium R&D rating.

With their low capital intensity and often oligopolistic markets, these businesses tend to enjoy healthy margins (Visa 65%, Fiserv 22% operating margins in 2019 respectively). Although B2C revenues are directly tied to consumer spending, payment companies’ revenues tend to be highly stable due to the large volumes of recurring essential spending as well as the ongoing structural changes taking place within the space.

Payments and FinTech’s large market size and growth derives from the global transition away from cash, the rise in ecommerce, and the proliferation of mobile devices – all of which present significant room for further market penetration and long runways. According to Capgemini’s World Payments Report 2019, global non-cash transaction volume will record a CAGR of 14% during 2017-2022, driven primarily by emerging economies.

UNIVERSE STATISTICS

OPPORTUNITY SET

The payments infrastructure space offers a mix of larger incumbents who should benefit from the shift to non-cash payments, as well as smaller disruptive businesses who are eager to change the model, trading on elevated multiples but in return for high growth potential. Established businesses benefit from efficient scale and network effects which create oligopolistic markets that are difficult to penetrate: within the card network space, Visa and Mastercard dominate western markets, while FIS, Fiserv and Jack Henry control the majority of the core processing market in the US, each demonstrating significant client retention rates.

However, new FinTech businesses are driving innovation across the value chain: Adyen have streamlined the 4-player business-to-consumer process by offering a single platform with better insights, whilst Square offers wireless payment hardware and processing software that enables improved analytics at affordable rates – particularly benefiting small businesses, which previously could not accept card transactions.

Digital wallet usage has been on the rise, particularly in China where, according to eMarketer, 81% of smartphone users in 2019 made use of proximity mobile payments. This technology takes two forms: a pass- through digital wallet such as Apple Pay, Google Pay or Alibaba’s Alipay, which remove the need to carry a physical wallet by storing your card details, whilst adding an additional layer of security through tokenisation; and a staged digital wallet such as PayPal, which serves as a digital storage of capital, with consumers required to fund their accounts before purchases. While there may be few pure-play opportunities, smartphone operating systems such as Apple iOS and Android, as well as third- party apps such as Tencent’s WeChat, have benefited from integrating digital wallets into their ecosystems, leading to higher consumer switching costs.

ROBOTICS & AUTOMATION

ROBOTICS & AUTOMATION

Sub Themes: Robots, Sensors, Logistics, 3D Printing

As we move into what is now commonly being referred to as ‘Industry 4.0’ or the ‘4th Industrial Revolution’ – centred around the automation of factories and connected robotics – much has been made of the possible implications for future employment, with many harbouring the ‘in 10 years time, robots will be doing my job’ mindset. According to the International Federation of Robotics (IFR), however, the increased use of robots and automation is set to complement and augment labour activities, not necessarily replace them, by enabling humans to focus on higher- skilled tasks, while robots automate lower-cognitive activities.

Robotics can be broadly categorised into two segments: industrial robots – those large robotic arms that spring to mind in a car manufacturing plant; to service robots, such as delivery drones and household robot vacuums. Indeed, the use of robotics and automation is not confined to the traditional, labour- intensive industries, but rather has potential applications extending to further afield end-markets. Amazon’s acquisition of Kiva Robotics, for example, which may have been passed over as an insignificant investment for the conglomerate, gave Amazon access to the technology that enables robots to now automate their warehouses and fulfilment centres, physically fetching items to be shipped and organising the warehouses based on the popularity of items. The potential applications of robotics and automation equally extend to the medical field, where robotic assisted surgery is becoming more prominent, led by Intuitive Surgical’s Da-Vinci device.

From an investment perspective, companies which are able to embrace automation give themselves the best opportunity of remaining competitive. Whilst labour costs have been on the rise, the cost of a robot has simultaneously been on the decline. Together with a robot’s ability to reduce the number of errors and defects, companies may benefit from improved productivity, a reduction in operating leverage and the subsequent expansion of margins. Perhaps more cyclical than other themes by a function of end-markets they currently serve (primarily automotive and electronics), however, over the long-term, the trend towards automation seems logical.

While a physical robotic arm is primarily used in heavy industries such as the automotive industry – which implies a higher capex requirement initially to create an installed base – the ongoing costs are largely servicing costs. Additionally, R&D remains important, particularly on the software side (Cognex spent 16% of sales on R&D in 2019 owing to their leadership in machine vision software), and while more modest, the general robotics R&D is required to continue expanding their use-cases and further bring down costs.

Robotics and Automation’s medium cyclicality rating is primarily a function of the markets it currently serves (automotive accounts for 30% and electronics 25% of total installed base, IFR 2018). The installation of these technologies requires large upfront costs which may mean businesses defer integration in less profitable periods. Having said this, once a robot is installed, recurring service revenues can be highly profitable for robot vendors (the average life of an industrial robot is greater than 10 years). Additionally, those businesses utilising automation can benefit from increased productivity leading to margin expansion.

The opportunity for industrial automation across industries remains large, from automotive and electronics to food and safety. This in addition to the faster growing service robot market including logistics and medical. Indeed, the use of robotics remains highly underpenetrated at present, with on average only 99 industrial robots per 10,000 employees in the manufacturing industry globally (IFR, 2018). While growth remains modest due to the large upfront costs, the number of industrial and service robots are expected to grow by 12% CAGR and ~40% CAGR to 2022 respectively (IFR, 2018).

UNIVERSE STATISTICS

OPPORTUNITY SET

The area of Robotics and Automation involves a multitude of players, the most prominent of which being the industrial robot manufacturers themselves. This market is comprised of 4 main players: ABB, Fanuc, Kuka and Yaskawa, best characterised by the different coloured robotic arms they each manufacture. While these incumbents may have started off manufacturing arms for the automotive industry, their equipment is slowly transitioning to alternative industries such as electronics, chemicals and food & beverage. These businesses benefit from high switching costs associated with the large installed base they currently possess.

While the robotic arm is perhaps the feature piece, this only represents one portion of robotics and automation. From sensors to software and electricals, the enablers consist of companies that provide components to make robots function effectively. Machine vision plays a key role in enabling these robots to ‘see’, by employing one or more cameras to capture and process images, identifying defects in components, and providing location information that guides a robot. Key players here include Cognex and Keyence. Additional contributors include the electricals that enable the machine to function from companies such as Schneider Electric, or simulation and control units from Siemens that control the systems. However, automation is broader than merely robotics. New opportunities are arising from companies such as Zebra Technologies and Honeywell, who use Radio Frequency Identification (RFID) to track the flow of goods in real time, in addition to Amazon and Walmart, who are showing promising signs in their pursuit of using drones for parcel delivery.

The final set of investment opportunities looks at the companies embracing robotics and automation to enhance their productivity and consumer experiences – the beneficiaries. Although the automotive industry was the first to incorporate these technologies into their manufacturing process, today, businesses across industries are looking for ways to integrate automation: within robotic surgery, Intuitive lead the market with their Da-Vinci robot; L’Oreal use 3D printing to speed up packaging prototyping; Amazon’s new checkout- less grocery stores, Amazon Go, uses RFID technology to track the movement of goods; and Adidas are automating parts of their supply chain by using auto cutting, computerised stitching and robotic adhesive spray systems. While this group yields few ‘pure-play’ opportunities, the area is more about efficient long-term capital allocators than a specific product or service.

Disclaimer: This Insight may provide information about Fund portfolios, including recent activity and performance and may contains facts relating to equity markets and our own interpretation. Any investment decision should take account of the subjectivity of the comments contained in the report. This Insight is provided for information only and all the information contained in it is believed to be reliable but may be inaccurate or incomplete; any opinions stated are honestly held at the time of writing but are not guaranteed. The contents of this Insight should not therefore be relied upon. It should not be taken as a recommendation to make an investment in the Funds or to buy or sell individual securities, nor does it constitute an offer for sale.