Concentrated Equally Weighted Portfolios

Elegant, simple, and disciplined

One question we are often asked when meeting investors is: why do we run the Fund as a concentrated portfolio with equal target weights?

At first it doesn’t sound particularly sophisticated to split a portfolio into a number of equally-weighted positions; perhaps even a bit of a blunt tool. Shouldn’t the portfolio construction process be more complicated and dynamic than that? Aren’t fund managers meant to assess consistently the potential upside for each and every company they own, and dynamically adjust the weights in their portfolio accordingly? If managers aren’t changing their weights based on how share prices have moved then what are they spending their time doing? Don’t you want to see a portfolio that contains some large weights to the manager’s favourite companies – a portfolio with conviction?

What we are most interested in is how can we maximise the chance of generating good returns. If that means we end up using a method that looks relatively simple, then so be it.

The elegance and efficiency of an equally weighted portfolio approach are part of the attraction, but there are some very good reasons as to why one should construct a portfolio on an equal-weight basis.

Why concentrated?

First, it’s worth considering why we run the Fund as a concentrated portfolio (typically 35 companies) rather than a broadly diversified portfolio.

Going back to fundamentals, the reason we all create a portfolio of stocks rather than investing in a single company is the benefits of diversification. By adding additional stocks to a portfolio we reduce the potential loss to the portfolio caused by any single investment going sour due to a company-specific issue.

The explanations, calculations, charts and tables shown below are for illustrative purposes only.

In the examples given there is an assumption that starts with each position having an exact equal weight and that for the stocks that have not lost 100% of their value, the percentage losses are evenly distributed i.e. that if one stock loses all of its value, all other stocks in the portfolio have no movement in their prices, which we believe is an unlikely scenario.

The maximum potential percentage loses and other figures stated are calculated on the basis of these assumptions and are therefore purely for illustrative purposes.

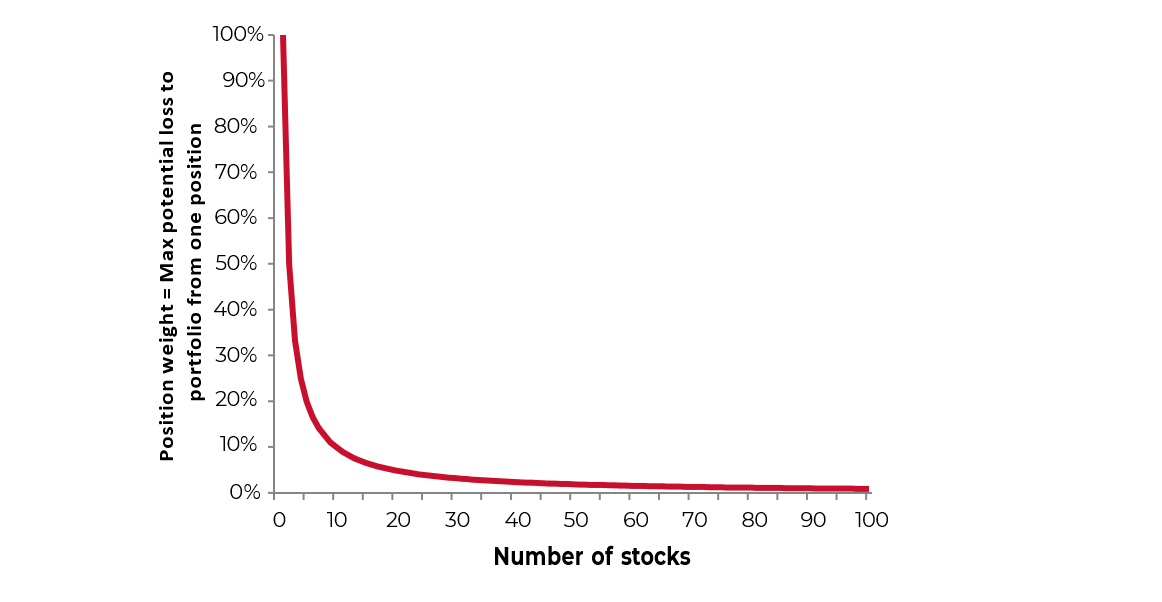

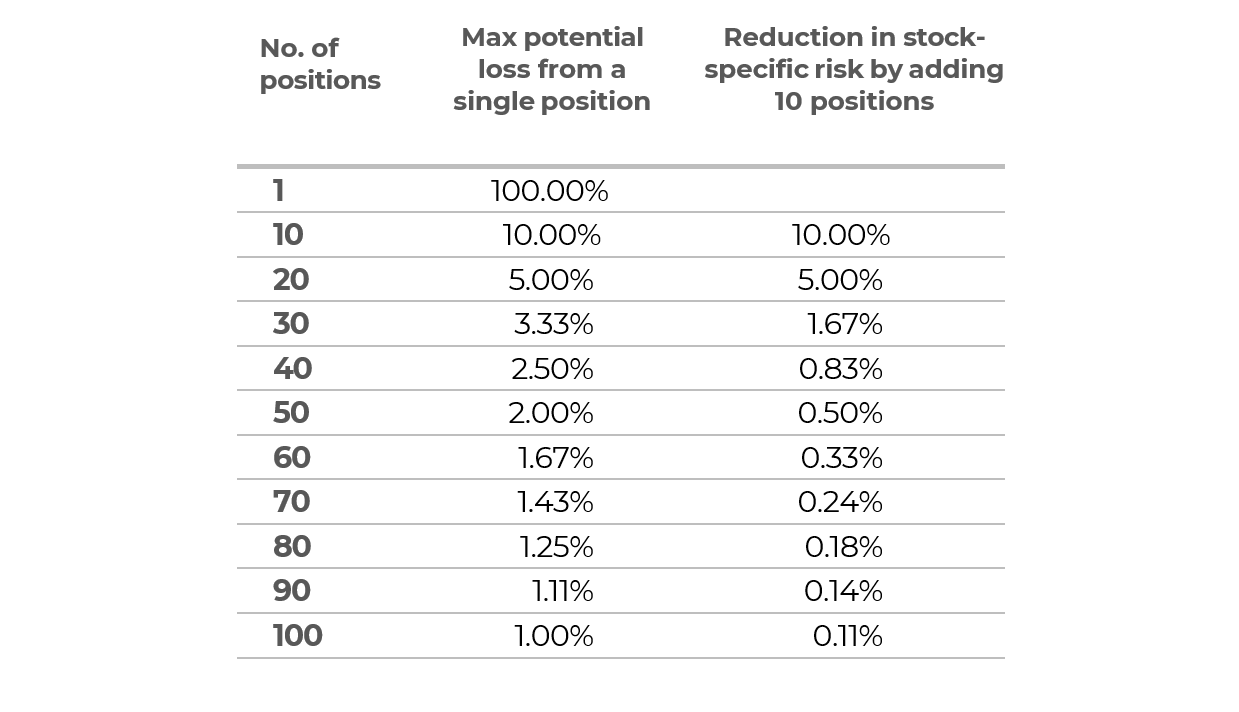

What’s interesting is how quickly you can reduce this stock-specific risk to a portfolio by increasing the number of equally weighted positions. The chart above shows this. When you have just one position in a portfolio the potential loss is obviously 100%, with five positions it’s 20%, with ten positions it’s 10%, and so on.

We think the sweet spot in terms of balancing the need for diversification to limit stock-specific risk and having sufficient weight in our positions so that any appreciation will have a meaningful impact on the portfolio is when you get to a level of 30 to 40 positions. At 30 positions your maximum potential loss to the portfolio from an individual position is 3.33%, while at 40 positions it is 2.5%.

Adding additional positions to a portfolio always has a diminishing effect on reducing stock specific risk, but beyond 40 positions the additional benefit is really quite small. At the same time, every additional stock we might consider including in a portfolio causes a very linear increase in the amount of time required to perform due diligence and on-going monitoring.

History shows that unexpected bankruptcies do happen, and even though we invest in companies that consistently earn high return on capital and are very unlikely to go bankrupt, we can’t ignore this risk. If the worst was to happen and one of our positions was to go bust then we feel that a loss of 2.5-3.33% to the portfolio – while obviously disappointing – would be by no means disastrous to the overall portfolio.

Why an Equally Weighted Approach?

When you consider the potential total return of a share you have bought, there are really two dimensions to this total return to consider. First is the scale of the total return (in terms of both size and whether it is positive or negative), and second is the timeframe over which the return is realised.

Do we think we can identify companies that are undervalued and likely to provide a positive total return?

Yes. In our investment process there are two stages to identifying companies we think can outperform. First, we have identified a group of companies that the market frequently underestimates regarding the persistence of their return on capital.

Our analysis of companies with long histories of consistently earning high returns on capital shows that they tend to outperform the rest of the market over a cycle. There will be periods throughout this cycle where they underperform, but over the longer term they outperform. This, then, is our starting point.

The second element is to identify the companies within this group that look particularly attractively valued relative to the broader group. Being confident in the likelihood of these companies continuing to earn high return on capital in the future means we can take a more contrarian view relative to the market, and add companies to the portfolio when they are unloved and offering attractive value.

We have developed a robust process for identifying these companies, and whilst we won’t get every decision right, we think we will do so more often than not.

How confident can you be in the scale of this potential total return?

There are clearly various ways you can come up with a target price for a company, be it through a simple or multi-stage discounted-cash-flow model, a multiple and a forecast earnings or cashflow number, dividend discount models etc. We are very cautious about the usefulness of coming up with a single target price and prefer to consider a range of valuations.

All these methods require some element of forecasting and all these methods are highly sensitive to a number of key assumptions. Often when you make small adjustments to inputs, such as the discount rate or long-term growth rate, you can see quite a wide swing in the warranted valuation of the company. Given these sensitivities, our confidence in any explicit upside prediction must be cautious.

Therefore, given we consider a range of potential valuations for each company, we cannot simply rank every company we own by its potential upside.

We also have to realise that there are many exogenous shocks that can occur over the period of holding the company. These are largely impossible to predict, but they can have a marked effect on the warranted valuation of the company.

Can you predict the timeframe over which this return will be realised correctly more times than incorrectly?

Can we come up with reasons why we think company X which we own might move closer to our range of target prices faster than company Y or Z or any other of our 35 positions? If we ranked all 35, how often would we get more than half correct?

Whilst it would be tempting to claim we could do this, the honest answer is we don’t think we can, nor do we think anyone can. There will be occasions when people get it right, but statistically this is more often luck than skill.

To summarise, when we considered these questions we come to the following conclusions:

| Do you think you can identify companies that are undervalued and likely to provide a positive total return? | Yes |

| How confident can you be in the scale of this potential total return? | Not very |

| Can you predict the timeframe over which this return will be realised correctly more times than incorrectly? | No |

When you consider the answers to these questions and consider how to construct a portfolio, you quite quickly come to the conclusion that using an equally weighted portfolio approach works to our strengths. We think we can identify companies that are undervalued and will likely provide a decent return, but we don’t have much certainty in the scale of this return, we know we won’t get them all right and some will lose us money, and we have no idea of the timescale over which this will occur.

So, let every good idea we come up with have an equal weight in the portfolio, and the market will decide when a more reasonable valuation will be reached.

If we did have misplaced confidence in a precise target price and in the timescale over which we thought this valuation anomaly would be realised, then you could see why you might weight your positions according to your conviction.

Advantages of using a concentrated, equally weighted portfolio approach

I) High active share

By having a concentrated portfolio with stock weights that are not influenced by the benchmark, by design we will always have a high active share. With 35 equally weighted positions, each position will be around 2.9% - a level higher than almost every stock in the MSCI World Index. Since we launched the Fund our active share has always been around or above 90%. a broadly diversified portfolio.

II) Rebalancing effect

Having an equally weighted portfolio approach removes some of the behavioural biases that all fund managers need to be aware of and control. Loss aversion is a key behavioural bias, but a broadly equally weighted portfolio creates a strict discipline to counteract this. To keep the broadly portfolio equally weighted, we have to rebalance it periodically. Clearly we don’t want to rebalance too frequently as this would create additional trading costs, which we want to keep to an absolute minimum, so we tend to rebalance every two to three months. This forces us to go against the market trend and corresponding media narrative and buy some more of the companies that have underperformed the portfolio as a whole and reduce our holding in companies that have outperformed.

If a company we hold has performed particularly poorly, then the rebalancing process forces us to decide whether we want to continue to own it – in which case we have to buy some more – or if something about our initial thesis for purchase has changed, and we must sell the entire position. What we can never do is have a long tail of small ‘legacy’ positions which we don’t have conviction in.

III) One in, one out

Often it can be easier to identify companies we would like to own in the portfolio than it is to find something we already own that we should be selling. By having a ‘one in, one out’ policy we are forced to consider which position in the portfolio we like the least. We can’t just add another position. This keeps the portfolio up-to-date with our best ideas.

IV) Limited stock-specific risk

Having a concentrated and equally weighted portfolio approach limits your stock-specific risk to a reasonable level. If you don’t have an equally weighted portfolio then your stock-specific risk is limited to the size of your largest position. It’s easy to think of large cap companies that might have made up a significant proportion of non-equally weighted portfolios, that didn’t turn out so well!

V) Conviction in every position

Some might argue that by taking an equal-weight approach the portfolio we are limiting the scale of conviction we can have in anyone company.

Is it higher conviction to have much higher weights in five companies and small weights in 30, or equal weights in all 35?

Our equal-weight portfolio construction approach allows us to have the same weight in the portfolio for a company that has a £1 billion market cap as for a company that has a £100 billion market cap. In our minds that demonstrates high conviction.

A portfolio of best ideas

In a concentrated portfolio we aren’t looking for generalisations, we are dealing with best ideas in individual stocks with specific mispricings, anomalies and opportunities. We are looking for the exceptions and outliers.

We are willing to back our convictions in a controlled and considered manner whilst at the same time ensuring we don't have overly concentrated exposure to specific sectors.

Risk: The Guinness Global Equity Income Fund and WS Guinness Global Equity Income Fund are equity funds. Investors should be willing and able to assume the risks of equity investing. The value of an investment and the income from it can fall as well as rise as a result of market and currency movement, and you may not get back the amount originally invested. Further details on the risk factors are included in the Funds’ documentation, available on our website (guinnessgi.com/literature).

The Funds are actively managed with the MSCI World Index used as a comparator benchmark only.

Disclaimer: This Insight may provide information about Fund portfolios, including recent activity and performance and may contains facts relating to equity markets and our own interpretation. Any investment decision should take account of the subjectivity of the comments contained in the report. This Insight is provided for information only and all the information contained in it is believed to be reliable but may be inaccurate or incomplete; any opinions stated are honestly held at the time of writing but are not guaranteed. The contents of this Insight should not therefore be relied upon. It should not be taken as a recommendation to make an investment in the Funds or to buy or sell individual securities, nor does it constitute an offer for sale.